|

|

|

|

|||||

|

|

|

Casual restaurant chain Brinker International (NYSE:EAT) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 6.9% year on year to $1.45 billion. The company’s full-year revenue guidance of $5.80 billion at the midpoint came in 0.7% above analysts’ estimates. Its non-GAAP profit of $2.87 per share was 9.2% above analysts’ consensus estimates.

Is now the time to buy Brinker International? Find out by accessing our full research report, it’s free.

"Chili's delivered another strong quarter with industry-leading growth of +9%, rolling the industry-leading growth from last year for a 2-year comp sales growth of +43%," said Kevin Hochman, President & CEO of Brinker International.

Founded by Norman Brinker in Dallas, Brinker International (NYSE:EAT) is a casual restaurant chain that operates the Chili’s, Maggiano’s Little Italy, and It’s Just Wings banners.

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $5.69 billion in revenue over the past 12 months, Brinker International is one of the larger restaurant chains in the industry and benefits from a well-known brand that influences consumer purchasing decisions.

As you can see below, Brinker International’s sales grew at a decent 9.3% compounded annual growth rate over the last six years despite not opening many new restaurants, implying that growth was driven by higher sales at existing, established dining locations.

This quarter, Brinker International reported year-on-year revenue growth of 6.9%, and its $1.45 billion of revenue exceeded Wall Street’s estimates by 2.9%.

Looking ahead, sell-side analysts expect revenue to grow 3.1% over the next 12 months, a deceleration versus the last six years. This projection doesn't excite us and implies its menu offerings will face some demand challenges.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

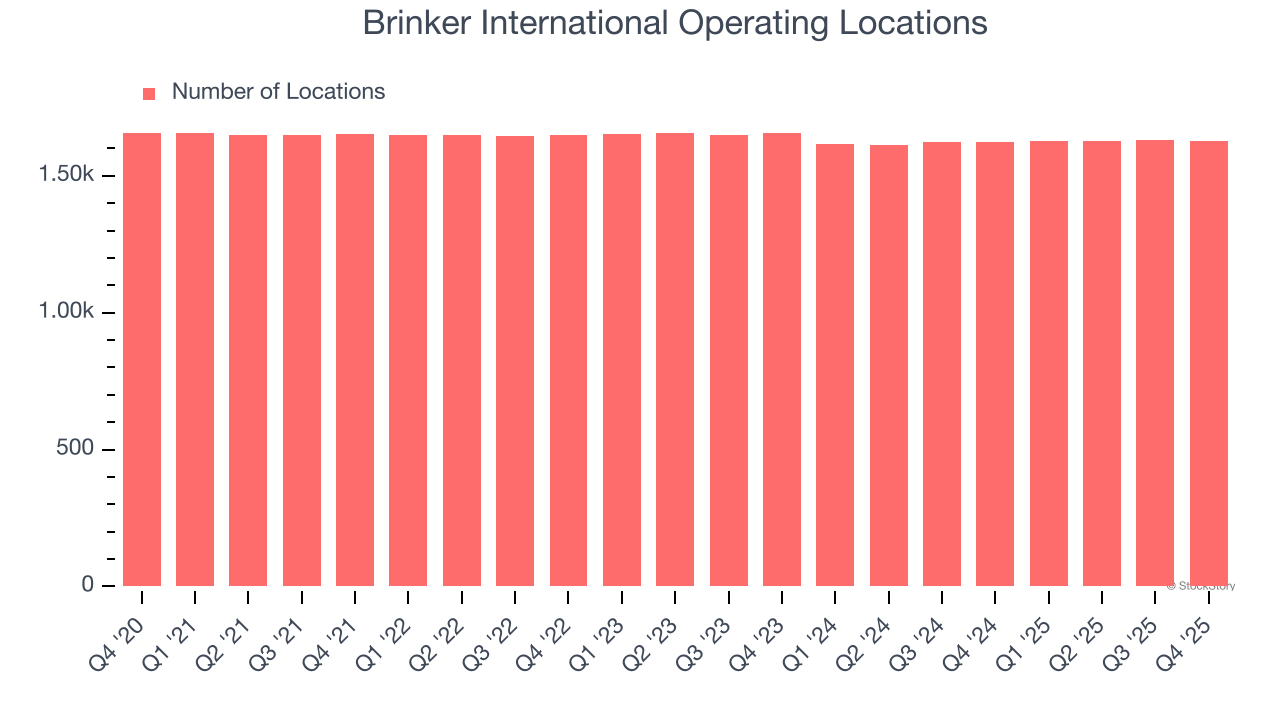

A restaurant chain’s total number of dining locations influences how much it can sell and how quickly revenue can grow.

Brinker International listed 1,627 locations in the latest quarter and has kept its restaurant count flat over the last two years while other restaurant businesses have opted for growth.

When a chain doesn’t open many new restaurants, it usually means there’s stable demand for its meals and it’s focused on improving operational efficiency to increase profitability.

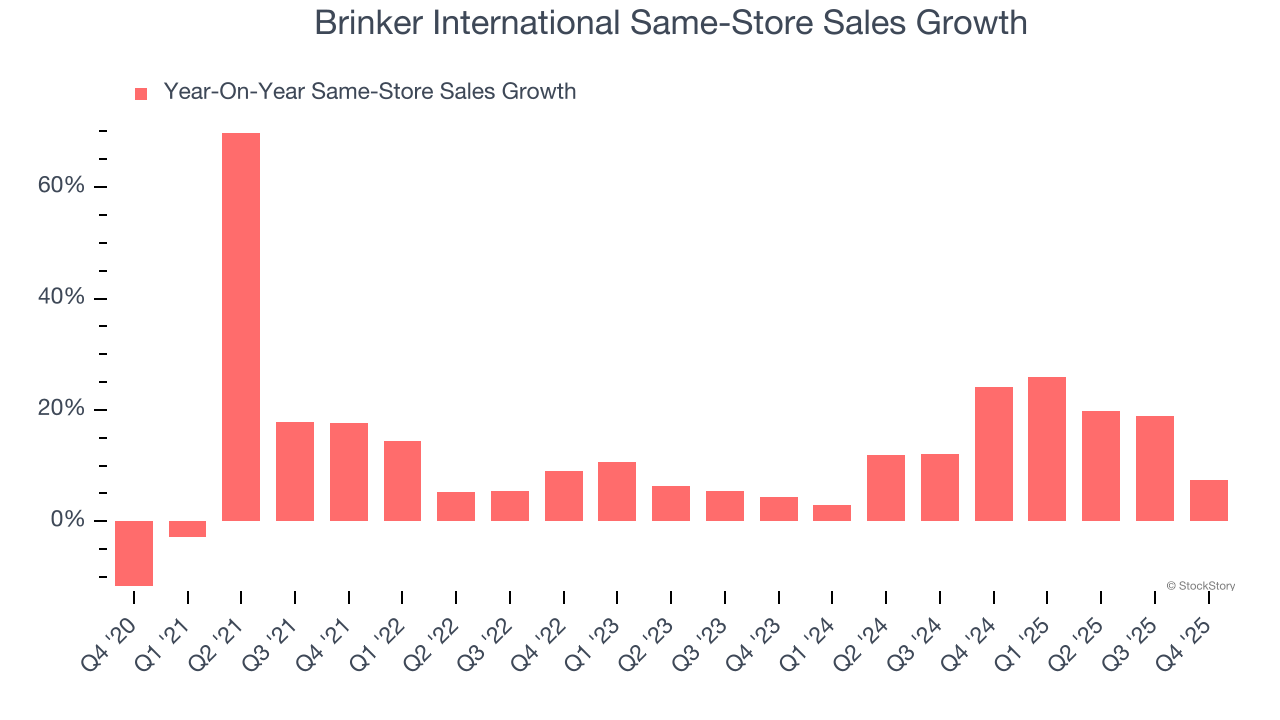

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales is an industry measure of whether revenue is growing at those existing restaurants and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Brinker International has been one of the most successful restaurant chains over the last two years thanks to skyrocketing demand within its existing dining locations. On average, the company has posted exceptional year-on-year same-store sales growth of 15.4%. Given its flat restaurant base over the same period, this performance stems from a mixture of higher prices and increased foot traffic at existing locations.

In the latest quarter, Brinker International’s same-store sales rose 7.5% year on year. This was a meaningful deceleration from its historical levels. We’ll be watching closely to see if Brinker International can reaccelerate growth.

This was a 'beat and raise' quarter. We were impressed by how significantly Brinker International blew past analysts’ same-store sales expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. The company capped things off by raising full-year guidance. Zooming out, we think this was a very solid print. The stock traded up 7.7% to $169.43 immediately following the results.

Sure, Brinker International had a solid quarter, but if we look at the bigger picture, is this stock a buy? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-17 | |

| Jul-14 | |

| Jul-10 | |

| Jul-10 | |

| Jul-01 | |

| Jun-18 | |

| Jun-02 | |

| May-27 | |

| May-18 | |

| May-11 | |

| May-01 | |

| Apr-30 | |

| Apr-30 | |

| Apr-29 | |

| Apr-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite