|

|

|

|

|||||

|

|

|

Lockheed Martin LMT is slated to report fourth-quarter 2025 results on Jan. 29, 2026, before market open.

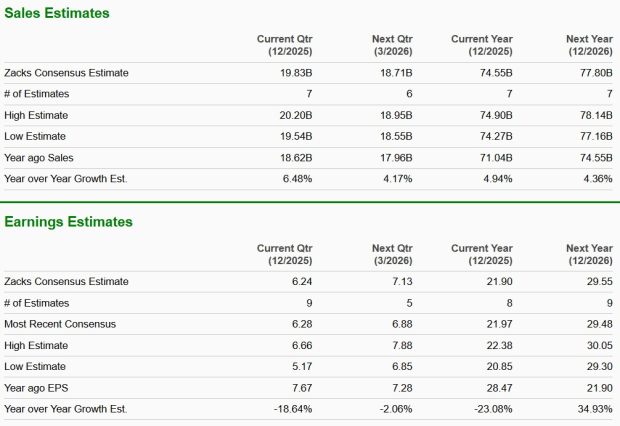

The Zacks Consensus Estimate for revenues is pegged at $19.83 billion, indicating an improvement of 6.5% from the year-ago quarter’s reported figure. The consensus mark for the bottom line is pegged at $6.24 per share, implying a decline of 18.6% from the prior-year quarter’s reported figure.

LMT’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 13.29%.

Our proven model does not conclusively predict an earnings beat for LMT this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat, which is not the case here. You can uncover the best stocks before they are reported with our Earnings ESP Filter.

LMT has an Earnings ESP of -9.36% and a Zacks Rank of 3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Some stocks in the same industry that have the combination of factors indicating an earnings beat are Draganfly DPRO and Intuitive Machines LUNR. DPRO and LUNR have an Earnings ESP of +13.33% and +221.62%, respectively. Both Draganfly and Intuitive Machines carry a Zacks Rank of 2 at present.

Higher sales volume from increased production contracts for the F-35 jet program is likely to have bolstered the Aeronautics segment’s top line.

A higher sales volume, resulting from the production ramp-up of tactical and strike missile programs, is likely to have benefited LMT’s Missiles and Fire Control segment’s quarterly sales performance.

The production ramp-up of the CH-53K helicopter program within the Sikorsky unit is likely to have bolstered the Rotary and Mission Systems segment’s sales.

Higher sales volume from strategic and missile defense programs, particularly the Next Generation Interceptor, is likely to have bolstered the Space segment’s top line.

The Zacks Consensus Estimate for the fourth quarter’s total backlog is pinned at $185.66 billion, indicating year-over-year growth of 5.5%.

Higher tariff-related costs are likely to have offset some of the benefits from increased sales volume and improved operational performance across LMT’s four business segments, weighing on overall earnings.

Moreover, charges related to a handful of Lockheed Martin’s classified programs, as well as lingering losses arising from its two helicopter programs- Canadian Maritime Helicopter Program (CMHP) and Turkish Utility Helicopter Program (TUHP), along with charges related to uncertain tax positions, are expected to have hurt its quarterly bottom-line performance.

LMT’s shares have exhibited an upward trend, gaining a notable percentage over the past six months. Specifically, the stock soared 41.6% in the time frame, outperforming the Zacks aerospace-defense industry’s growth of 8.6%. It has also outpaced the broader Zacks Aerospace sector’s return of 10.9% as well as the S&P 500’s gain of 11.8%.

Other industry players, such as Draganfly and Intuitive Machines, have also delivered solid performance over the past six months. The shares have gained 85.6% and 72.7%, respectively.

In terms of valuation, LMT’s forward 12-month price-to-sales (P/S) is 1.76X, a discount to its industry’s average of 2.72X. This suggests that investors will be paying a lower price than the company's expected sales growth compared with its industry’s P/S ratio.

However, its industry peers are currently trading at a premium compared with LMT. While the forward 12-month price/earnings multiple for DPRO is 3.00, the same for LUNR is 7.68.

LMT is well-positioned for long-term growth, supported by steady demand for its core defense programs and a strong order backlog that provides good revenue visibility. The company continues to win contracts across key platforms such as the F 35 fighter jet, missile defense systems, helicopters and precision strike weapons. Growth across multiple business segments, rising international demand and a supportive U.S. defense spending environment strengthen Lockheed Martin’s long-term revenue outlook and support stable cash flow generation.

However, geopolitical factors, including sanctions and potential supply-chain disruptions, add uncertainty. While Lockheed Martin’s diversified portfolio and strong customer relationships help reduce these risks, effective execution and cost control will be key to maintaining earnings performance going forward.

Lockheed Martin appears well-positioned ahead of its fourth-quarter earnings, supported by steady demand across its core defense programs and continued activity in key platforms such as the F 35, missile defense systems, helicopters and space programs. While revenues are likely to have benefited from higher production and program execution, earnings are expected to have faced pressure from higher costs and ongoing program-related charges. Investors who already own the stock can continue to hold it, given the company’s solid long-term outlook, while those looking to initiate a position may prefer to wait for a more favorable entry point after the earnings announcement.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite