|

|

|

|

|||||

|

|

|

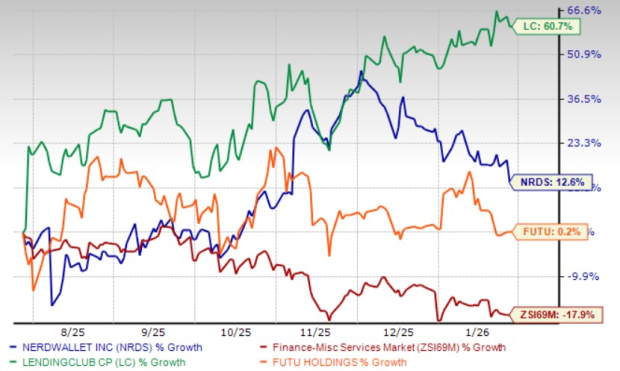

NerdWallet Inc. NRDS shares gained 12.6% in the past six months against the industry’s decline of 17.9%. Its peers FUTU Holdings FUTU and LendingClub LC have also outperformed the industry. FUTU Holdings rallied 0.2% while LendingClub rose 60.7% in the same time frame.

Price Performance

Given NRDS’s impressive rally, investors might wonder if the opportunity to add this stock to their portfolio has passed. To answer this, let us delve deeper and analyze factors at play.

NerdWallet is actively reducing its historical reliance on organic Google traffic by expanding into performance marketing, artificial intelligence (AI)-driven discovery and deeper financial services. Over the past year, the company has invested in paid marketing capabilities to acquire high-intent users more predictably and with attractive unit economics. Management noted that in third-quarter 2025, these efforts helped offset organic search pressure, particularly within Credit Cards and small and medium sized business (SMB) products.

At the same time, NerdWallet is beginning to benefit from AI-driven referral channels, including traffic originating from large language models (LLMs). Management highlighted that NerdWallet is now the most cited source among peers in LLM responses. While this traffic remains modest in volume, early data indicates meaningfully higher conversion rates than traditional organic search, positioning AI referrals as a potentially high-return on investment (ROI) acquisition channel over time.

Beyond traffic acquisition, NerdWallet is diversifying monetization by moving deeper into financial services through vertical integration. Acquisitions such as Next Door Lending in mortgages and earlier SMB integrations allow the company to participate further down the funnel, where monetization is significantly higher. Early results from the mortgage brokerage model show roughly 2X revenue per lead versus the traditional marketplace, reinforcing the earnings leverage of this strategy and supporting a more durable, diversified revenue mix.

NerdWallet has reached a clear inflection point in profitability, demonstrating sustained earnings power alongside disciplined growth. In third-quarter 2025, the company reported net income of $26.3 million, reflecting a meaningful shift from prior periods of investment-led losses to consistent bottom-line profitability. This improvement was supported by strong operating leverage, as revenue growth increasingly translated into earnings rather than incremental cost growth.

Adjusted EBITDA continued to scale meaningfully to $53.6 million in the third quarter of 2025, representing a 25% margin and 44% year-over-year growth. Non-GAAP operating income rose even faster, increasing 81% to $41.3 million, with margins expanding to 19%. These gains were driven by improved marketing efficiency, lower R&D and G&A expenses as a percentage of revenues, and the benefits of automation and AI-driven operational tools.

Management’s raised 2025 guidance for operating income and EBITDA further reinforces confidence that NerdWallet’s margin expansion and cash flow generation are structural rather than cyclical. NerdWallet expects its 2025 adjusted EBITDA to be $141-$45 million, up from the earlier stated $106-$116 million. In 2024, adjusted EBITDA was $108 million.

NerdWallet exited the third quarter of 2025 with a strong and flexible balance sheet, positioning the company to both withstand macro volatility and continue investing in long-term growth. As of the quarter-end, NerdWallet held $120.6 million in cash and cash equivalents, providing ample liquidity to fund operations, strategic initiatives and opportunistic capital returns without reliance on external financing.

In addition to its cash balance, the company maintains access to an undrawn $125-million revolving credit facility, further enhancing financial flexibility. This unused revolver provides downside protection in the event of macro disruption while preserving optionality for acquisitions, accelerated share repurchases, or incremental investment in high-return growth initiatives such as AI, performance marketing and vertical integration.

NerdWallet has also demonstrated disciplined capital return through share repurchases. In third-quarter 2025, the company repurchased $19 million of its common stock, bringing total repurchases to a meaningful level while still maintaining balance sheet strength. As of Sept. 30, 2025, $55.8 million remained available under the existing authorization, signaling management’s confidence in the company’s intrinsic value and cash flow durability.

Importantly, these repurchases were executed alongside continued investment in the business, underscoring NerdWallet’s ability to generate excess capital while pursuing growth.

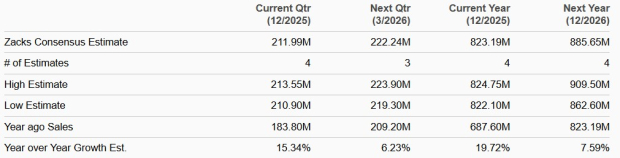

The Zacks Consensus Estimate for NerdWallet’s 2025 and 2026 earnings implies year-over-year rallies of 720% and 49.6%, respectively. The earnings estimate for both year remained unchanged over the past month.

Estimate Revision Trend

Image Source: Zacks Investment Research

The consensus estimate for 2025 and 2026 sales implies year-over-year rallies of 19.7% and 7.6%, respectively.

Sales Estimates

From a valuation standpoint, NRDS appears inexpensive relative to the industry. It is currently trading at a discount with a forward 12-month price-to-earnings (P/E) of 12.94X, well below the industry average of 21.48X. Further, FUTU Holdings is trading at a 12-month forward P/E of 14.74X, while LendingClub is trading at 19.19X.

P/E F12M

While NerdWallet has made meaningful progress in diversifying its revenue streams, improving profitability and strengthening its balance sheet, much of this positive momentum is increasingly reflected in the stock’s recent performance. The shares have rallied solidly over the past six months, and although valuation remains reasonable versus peers, near-term upside may be more measured as investors await further confirmation of sustained growth across newer channels.

Given the balance between improving fundamentals and recent price appreciation, maintaining a Hold stance appears prudent at this stage. Investors already owning the stock can benefit from NerdWallet’s continued execution and cash generation, while prospective investors may prefer to wait for a more attractive entry point or additional evidence of durable growth from AI-driven traffic and vertical integration initiatives.

At present. NRDS carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Jul-27 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-13 | |

| Jul-07 | |

| Jul-02 | |

| Jul-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite