|

|

|

|

|||||

|

|

|

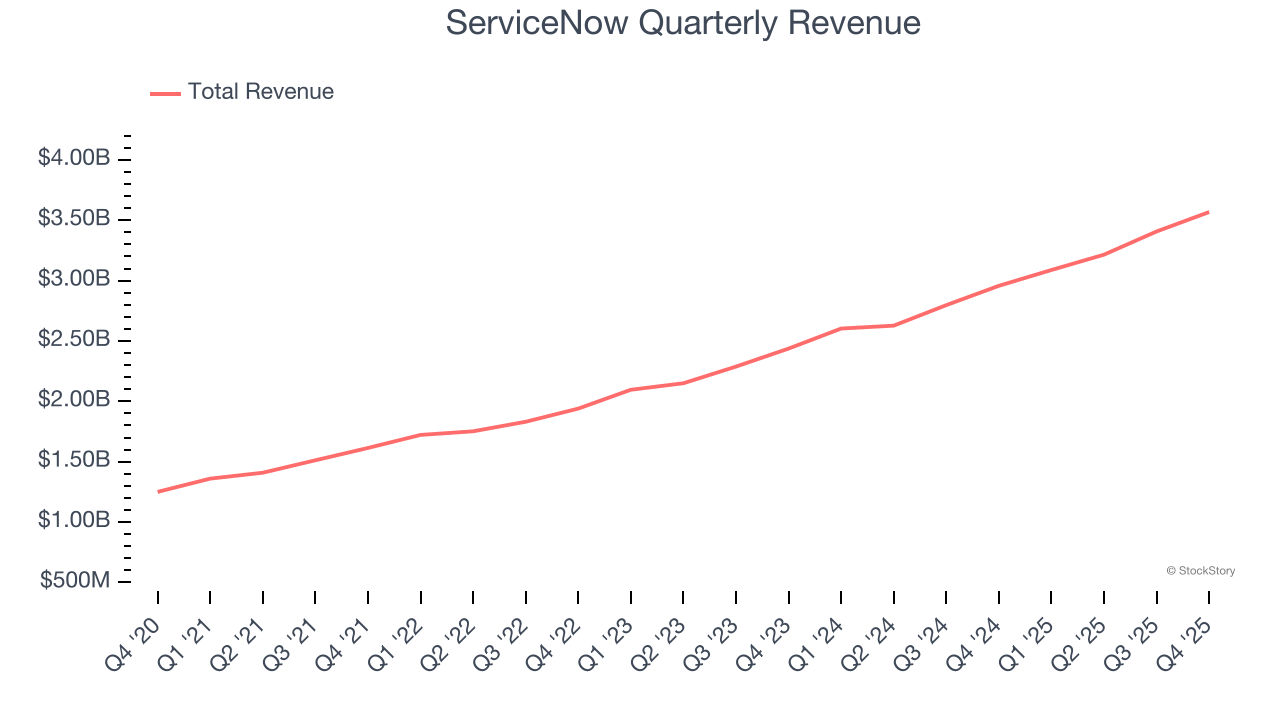

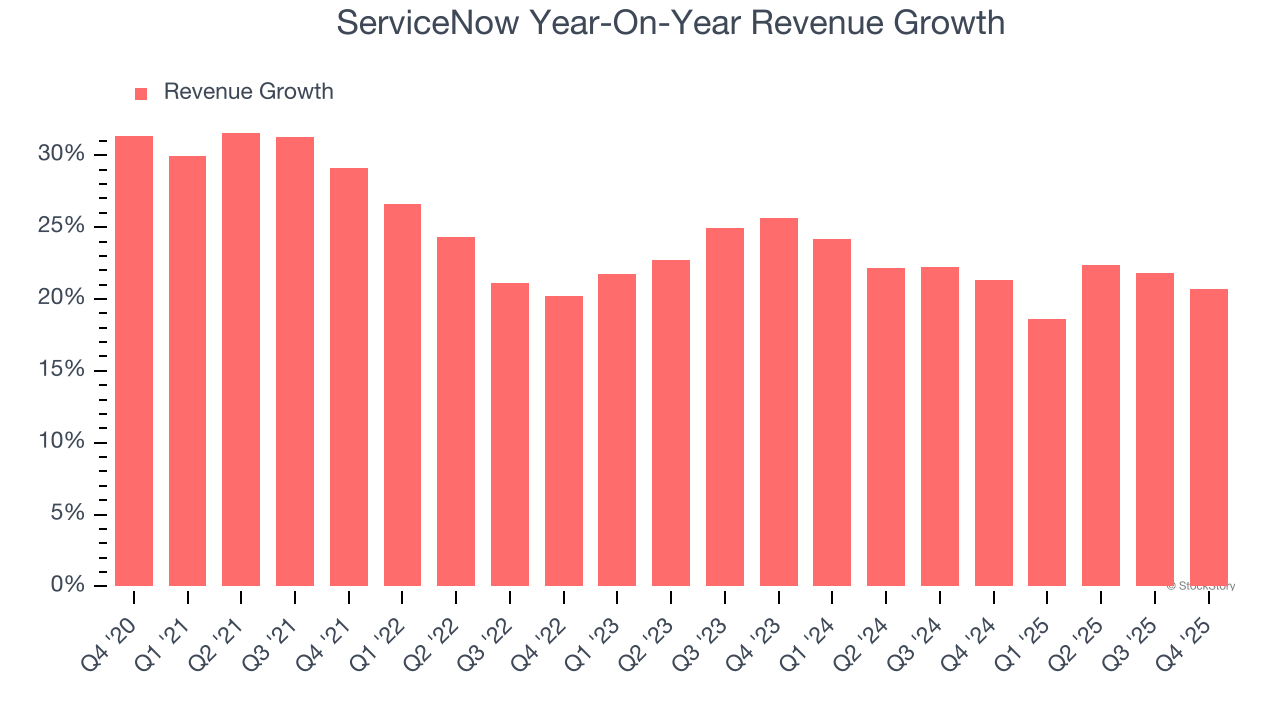

Enterprise workflow automation company ServiceNow (NYSE:NOW) reported revenue ahead of Wall Streets expectations in Q4 CY2025, with sales up 20.7% year on year to $3.57 billion. Its non-GAAP profit of $0.92 per share was 3.9% above analysts’ consensus estimates.

Is now the time to buy ServiceNow? Find out by accessing our full research report, it’s free.

Built on a single code base that processes over 4 billion workflow transactions daily, ServiceNow (NYSE:NOW) provides a cloud-based platform that helps organizations automate and digitize workflows across departments, from IT and HR to customer service and security.

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, ServiceNow’s 24.1% annualized revenue growth over the last five years was solid. Its growth surpassed the average software company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. ServiceNow’s annualized revenue growth of 21.7% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, ServiceNow reported robust year-on-year revenue growth of 20.7%, and its $3.57 billion of revenue topped Wall Street estimates by 1%.

Looking ahead, sell-side analysts expect revenue to grow 18.2% over the next 12 months, a deceleration versus the last two years. We still think its growth trajectory is attractive given its scale and indicates the market is baking in success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

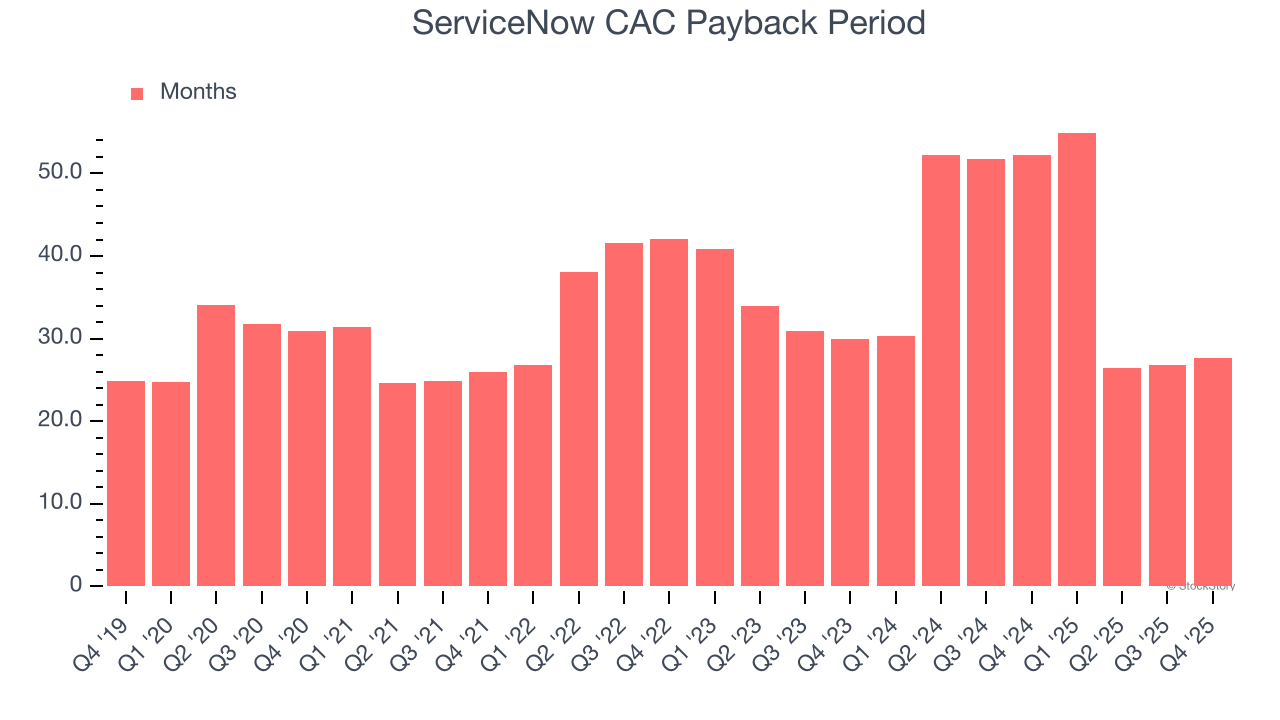

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

ServiceNow is very efficient at acquiring new customers, and its CAC payback period checked in at 27.6 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation due to its scale. These dynamics give ServiceNow more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

Current RPO (remaining performance obligations) was just in line with expectations, and ServiceNow only narrowly topped analysts’ revenue expectations this quarter. While adjusted operating profit in the quarter beat and subscription revenue guidance was slightly ahead, the overall results were not convincingly ahead of Wall Street's estimates enough to ease fears that AI may be a net negative for the company. The stock traded down 5.4% to $123.05 immediately following the results.

The latest quarter from ServiceNow’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 | |

| Mar-30 | |

| Mar-30 | |

| Mar-28 | |

| Mar-26 | |

| Mar-26 | |

| Mar-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite