|

|

|

|

|||||

|

|

|

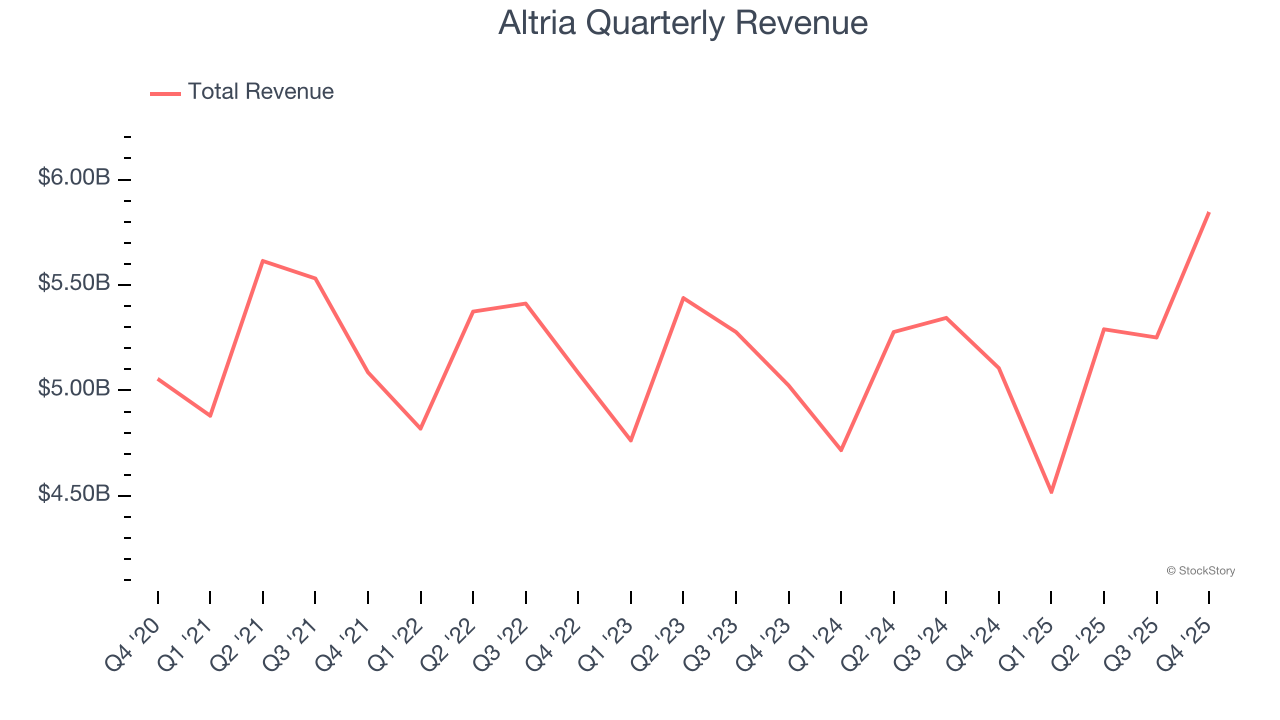

Tobacco company Altria (NYSE:MO) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 14.5% year on year to $5.85 billion. Its non-GAAP profit of $1.30 per share was 1.3% below analysts’ consensus estimates.

Is now the time to buy Altria? Find out by accessing our full research report, it’s free.

“2025 was a year of continued momentum for Altria, marked by strong financial performance, strategic progress across our smoke-free portfolio, new relationships in support of our long-term growth goals and significant cash returns to shareholders,” said Billy Gifford, Altria’s Chief Executive Officer.

Best known for its Marlboro brand of cigarettes, Altria (NYSE:MO) offers tobacco and nicotine products.

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $20.91 billion in revenue over the past 12 months, Altria is one of the most widely recognized consumer staples companies. Its influence over consumers gives it negotiating leverage with distributors, enabling it to pick and choose where it sells its products (a luxury many don’t have). However, its scale is a double-edged sword because there are only so many big store chains to sell into, making it harder to find incremental growth. To expand meaningfully, Altria likely needs to tweak its prices, innovate with new products, or enter new markets.

As you can see below, Altria struggled to increase demand as its $20.91 billion of sales for the trailing 12 months was close to its revenue three years ago. This shows demand was soft, a poor baseline for our analysis.

This quarter, Altria reported year-on-year revenue growth of 14.5%, and its $5.85 billion of revenue exceeded Wall Street’s estimates by 16.6%.

Looking ahead, sell-side analysts expect revenue to decline by 3.6% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and suggests its products will face some demand challenges. At least the company is tracking well in other measures of financial health.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

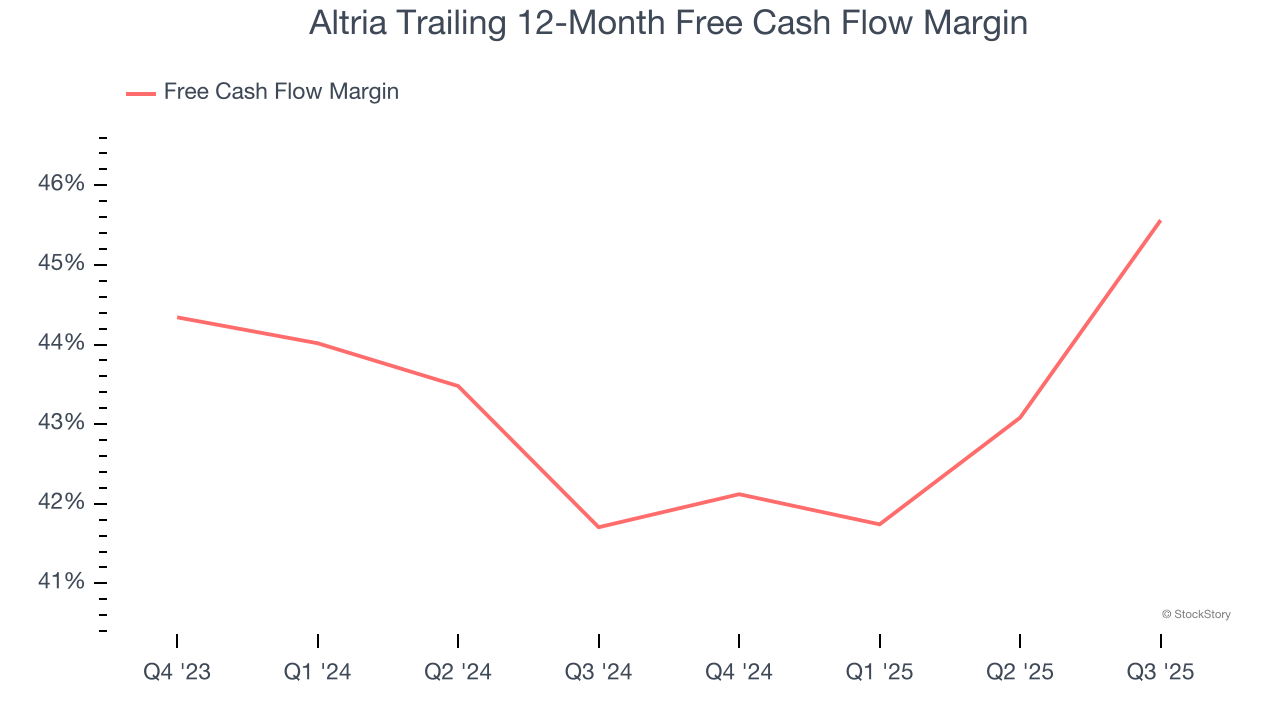

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Altria has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer staples sector, averaging an eye-popping 40.9% over the last two years.

We were impressed by how significantly Altria blew past analysts’ revenue expectations this quarter. We were also glad its gross margin outperformed Wall Street’s estimates. On the other hand, its EPS slightly missed. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 2.5% to $61.53 immediately after reporting.

Is Altria an attractive investment opportunity right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-14 | |

| Jul-10 | |

| Jul-09 | |

| Jul-02 | |

| Jun-30 | |

| Jun-24 | |

| Jun-01 | |

| May-28 | |

| May-21 | |

| May-19 | |

| May-18 | |

| May-14 | |

| May-14 | |

| May-06 | |

| May-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite