|

|

|

|

|||||

|

|

|

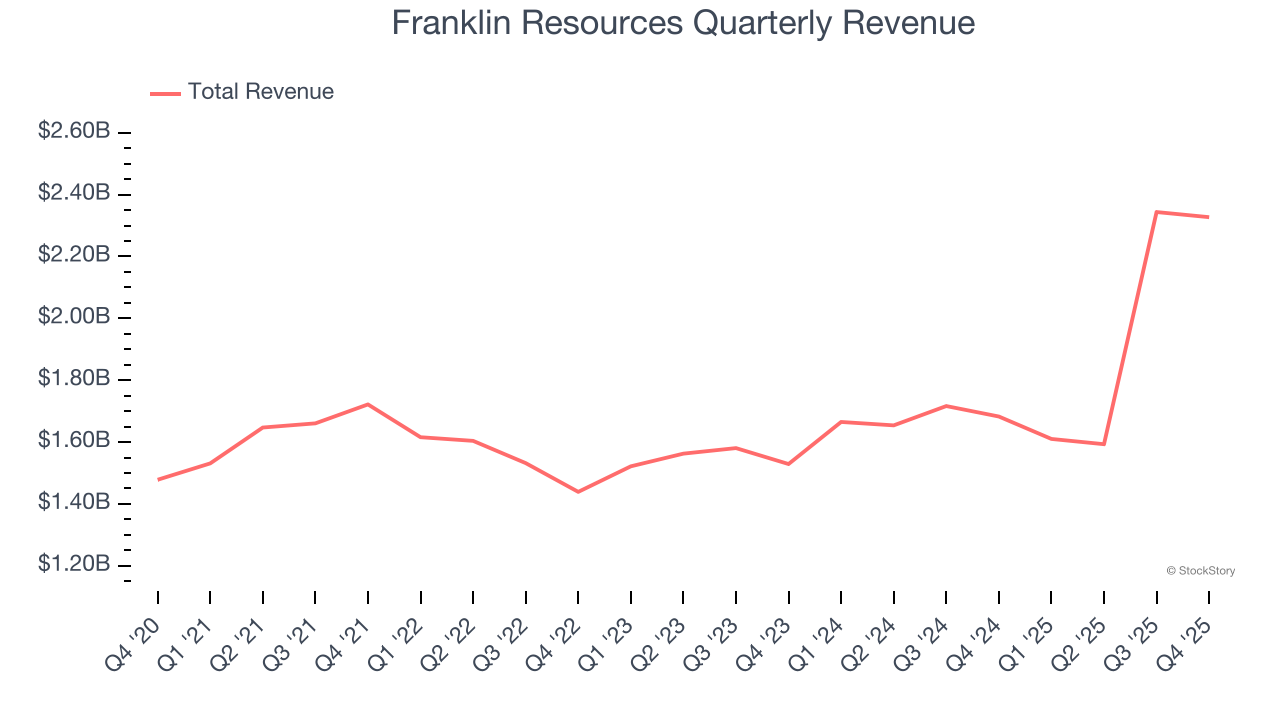

Global investment management firm Franklin Resources (NYSE:BEN) announced better-than-expected revenue in Q4 CY2025, with sales up 38.3% year on year to $2.33 billion. Its non-GAAP profit of $0.70 per share was 27.5% above analysts’ consensus estimates.

Is now the time to buy Franklin Resources? Find out by accessing our full research report, it’s free.

“Our first fiscal quarter continued the momentum we built last year with strong client activity across Franklin Templeton’s diversified global platform, with positive net flows in both public and private markets,” said Jenny Johnson, Chief Executive Officer of Franklin Resources, Inc.

Operating under the widely recognized Franklin Templeton brand since 1947, Franklin Resources (NYSE:BEN) is a global investment management organization that offers financial services and solutions to individuals, institutions, and wealth advisors worldwide.

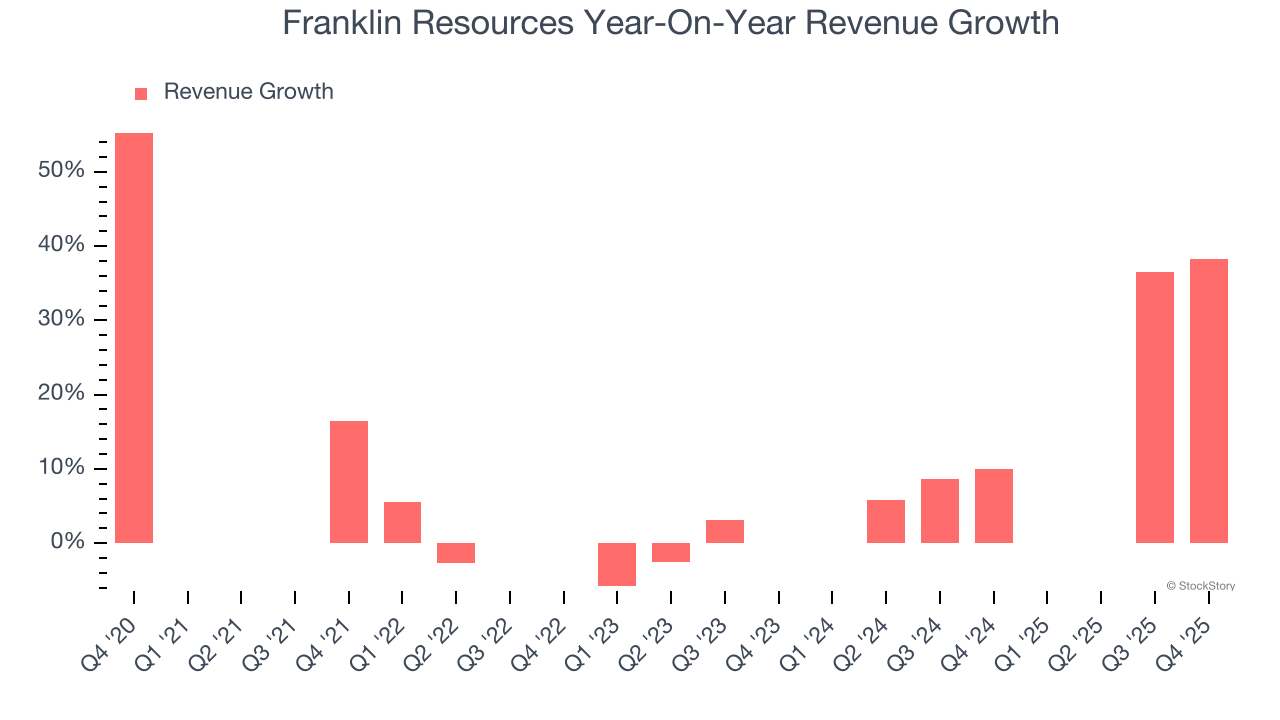

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Franklin Resources’s revenue grew at a solid 12.3% compounded annual growth rate over the last five years. Its growth beat the average financials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Franklin Resources’s annualized revenue growth of 12.7% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

This quarter, Franklin Resources reported wonderful year-on-year revenue growth of 38.3%, and its $2.33 billion of revenue exceeded Wall Street’s estimates by 11.5%.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

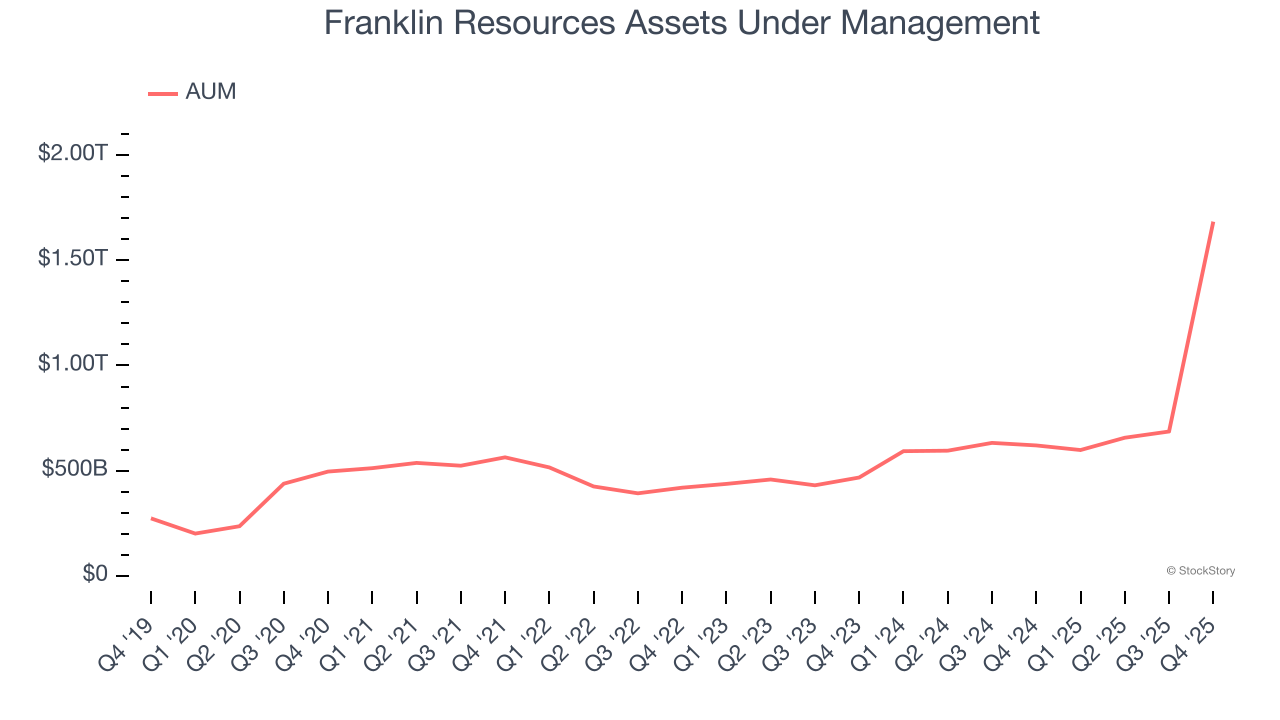

Assets Under Management (AUM) represents the total value of investments that a financial institution manages for its clients. These assets generate steady income through management fees, creating predictable revenue streams that remain stable so long as clients remain invested with the firm.

Franklin Resources’s AUM has grown at an annual rate of 21.5% over the last five years, better than the broader financials industry and faster than its total revenue. When analyzing Franklin Resources’s AUM over the last two years, we can see that growth accelerated to 42.2% annually. Fundraising or short-term investment performance were net contributors for the company over this shorter period since assets grew faster than total revenue. Just remember that while assets are relevant to watch, we don't place too much emphasis on them because they ebb and flow with the market.

Franklin Resources’s AUM punched in at $1.68 trillion this quarter, beating analysts’ expectations by 141%. This print was 172% higher than the same quarter last year.

It was good to see Franklin Resources beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 1.6% to $26.31 immediately after reporting.

Franklin Resources put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-08 | |

| Jul-06 | |

| Jul-06 | |

| Jul-01 | |

| Jul-01 | |

| Jun-23 | |

| Jun-19 | |

| Jun-19 | |

| Jun-18 | |

| Jun-17 | |

| Jun-17 | |

| Jun-09 | |

| Jun-04 | |

| Jun-04 | |

| Jun-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite