|

|

|

|

|||||

|

|

|

A key player in the broader AI frenzy, Palantir PLTR, delivered its 2025 Q4 results this week, kicking off a mighty busy earnings docket overall. Shares have been red-hot over the past year overall, gaining nearly 90% on the back of red-hot demand. Though shares have cooled off a bit in recent months, the results delivered paint a rosy picture in both the near and long-term picture for the stock.

Palantir again continued to fire on all cylinders throughout the period, with overall sales of $1.4 billion flying 70% year-over-year. U.S. results were notably strong, underpinned by both commercial and government strength. Specifically, U.S. sales totaled $1.1 billion, growing 93% year-over-year and an even more impressive 28% sequentially.

Further, Palantir closed 180 deals of at least $1 million, 84 deals worth at least $5 million, and 61 deals worth at least $10 million. It closed more than $4.2 billion of total contract value (TCV) overall, up more than 130% from the year-ago period.

And its consumer base keeps snowballing, with customer count surging 34% from the year-ago period. The results also wrapped up its broader FY25, with annual sales of $4.5 billion up 56% from FY25. The top-line growth here is incredible, a theme we’ve become accustomed to from the company over the last several years.

Below is a chart illustrating Palantir’s annual sales, with the acceleration evident since 2023.

Importantly, guidance for its FY26 alludes to more top-line growth acceleration, with forecasted FY26 sales of $7.2 billion reflecting a 61% jump from its FY25. Alex Karp, CEO, remained notably bullish and proud of the results, stating –

“Palantir is alone in choosing to exclusively focus on scaling the operational leverage made possible by the rapid advancements of AI models, a trend that we first called ‘commodity cognition’ well before others started repeating it.”

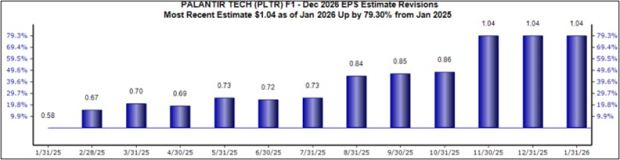

Concerning earnings, analysts have been bullish on the company’s broader FY26 EPS outlook for some time now, with the current $1.04 Zacks Consensus EPS estimate up nearly 80% just over the last year. The latest set of results helps underpin the bright EPS outlook in a big way, with the demand picture undoubtedly remaining bright.

Shares have seen a strong move following the initial earnings release, reflective of investors’ appetites for continued AI exposure. While 2026 will likely be filled with many companies considered to be AI ‘losers’, Palantir’s visible demand picture helps insulate it nicely.

Bottom Line

Palantir PLTR again crushed it in its latest quarterly release, with snowballing demand again leading to huge growth while also painting a rosy picture for its FY26.

The stock remains one of the best AI plays out there for those seeking exposure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 | |

| Jul-13 | |

| Jul-12 | |

| Jul-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite