|

|

|

|

|||||

|

|

|

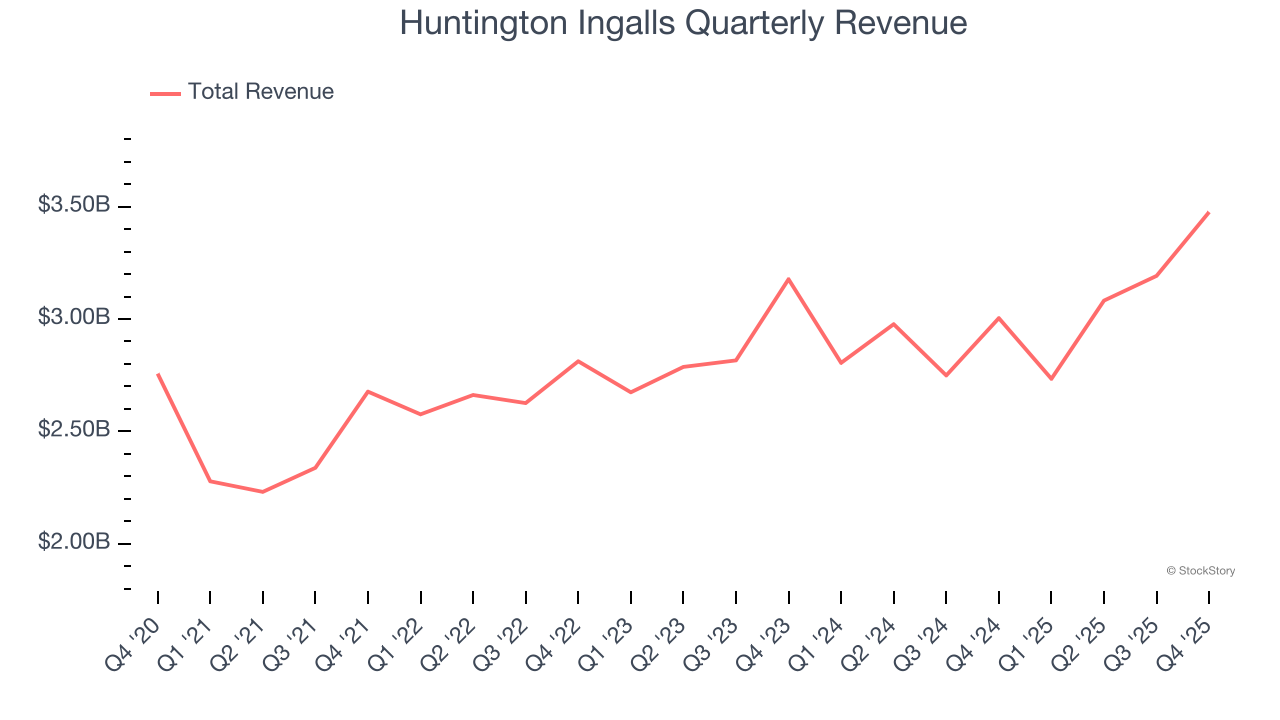

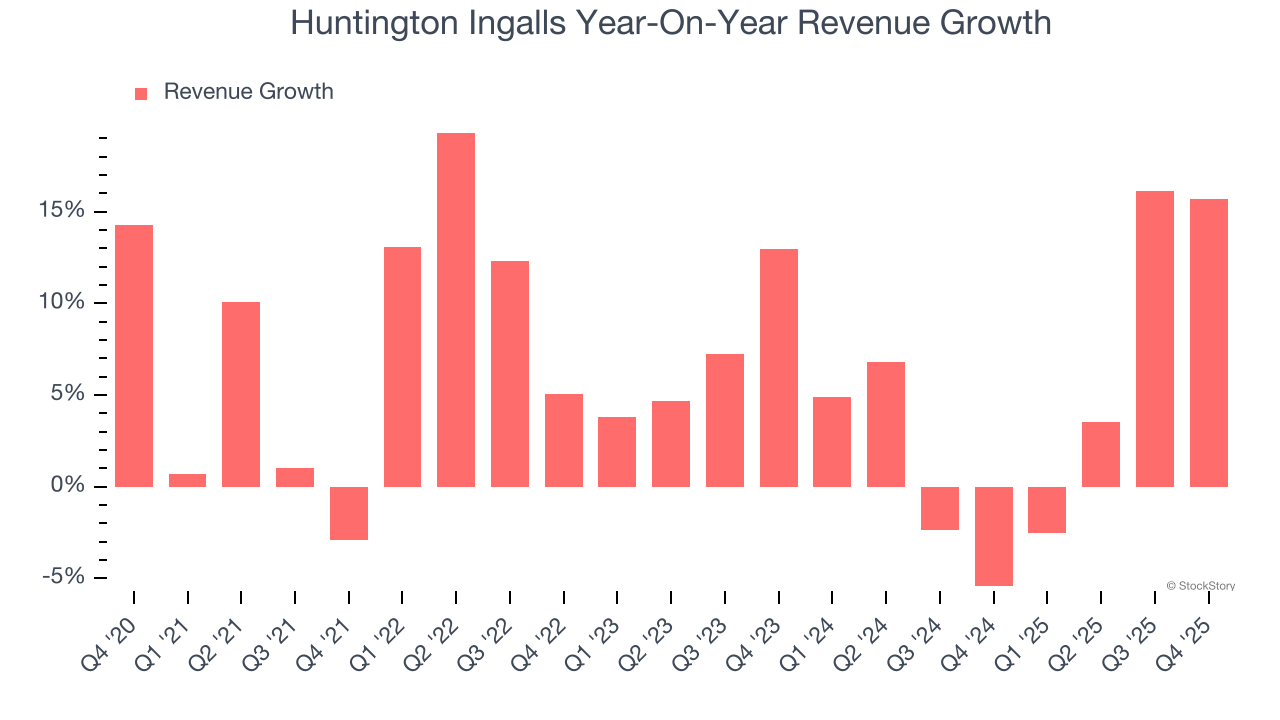

Aerospace and defense company Huntington Ingalls (NYSE:HII) announced better-than-expected revenue in Q4 CY2025, with sales up 15.7% year on year to $3.48 billion. Its GAAP profit of $4.04 per share was 3.7% above analysts’ consensus estimates.

Is now the time to buy Huntington Ingalls? Find out by accessing our full research report, it’s free.

Chris Kastner, HII’s president and CEO, said, “We made solid progress on our operational initiatives in 2025 and enter 2026 with strong momentum. With more than 40 ships at Ingalls and Newport News in active construction or modernization, our focus in 2026 is clear: We must build on this momentum, and continue to increase our shipbuilding throughput. The U.S. Navy and all of our defense customers need our ships and technologies now more than ever and we are committed to delivering for our customer and the nation.”

Building Nimitz-class aircraft carriers used in active service, Huntington Ingalls (NYSE:HII) develops marine vessels and their mission systems and maintenance services.

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Huntington Ingalls grew its sales at a tepid 5.9% compounded annual growth rate. This fell short of our benchmark for the industrials sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Huntington Ingalls’s recent performance shows its demand has slowed as its annualized revenue growth of 4.4% over the last two years was below its five-year trend.

This quarter, Huntington Ingalls reported year-on-year revenue growth of 15.7%, and its $3.48 billion of revenue exceeded Wall Street’s estimates by 12.7%.

Looking ahead, sell-side analysts expect revenue to grow 1.9% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will face some demand challenges.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

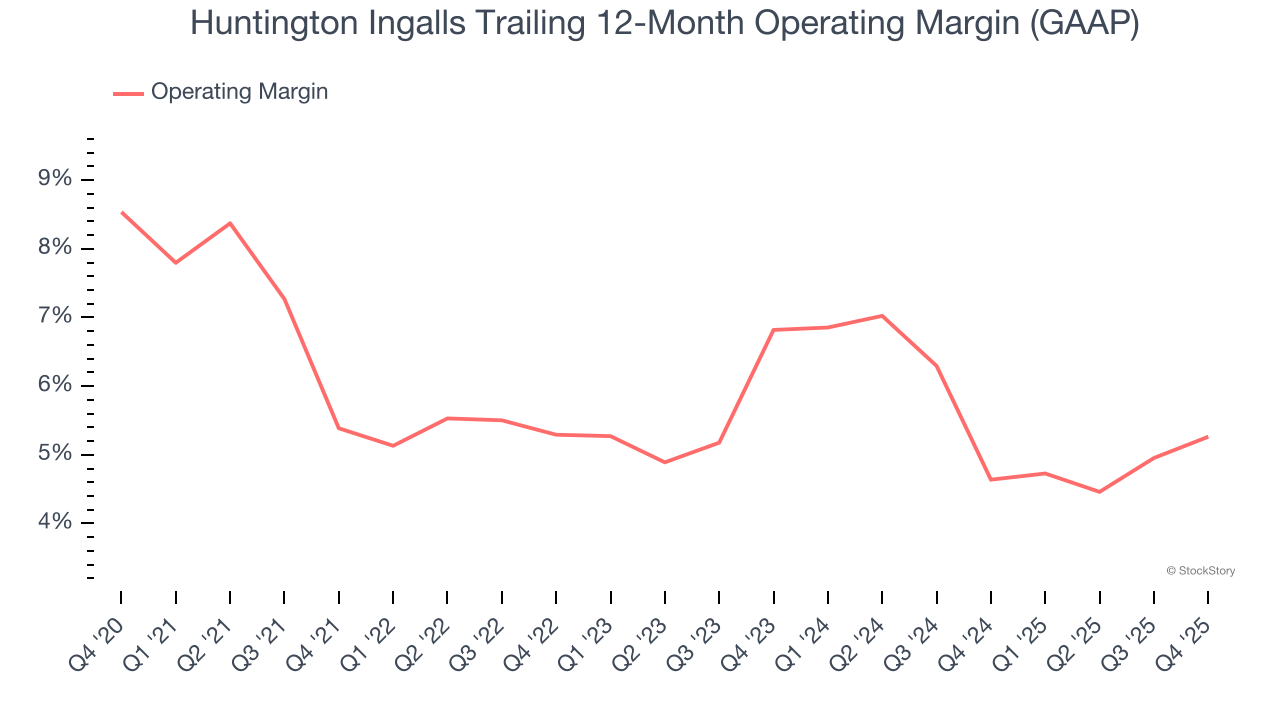

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Huntington Ingalls’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 5.5% over the last five years. This profitability was paltry for an industrials business and caused by its suboptimal cost structure.

Looking at the trend in its profitability, Huntington Ingalls’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Huntington Ingalls generated an operating margin profit margin of 4.9%, up 1.3 percentage points year on year. This increase was a welcome development and shows it was more efficient.

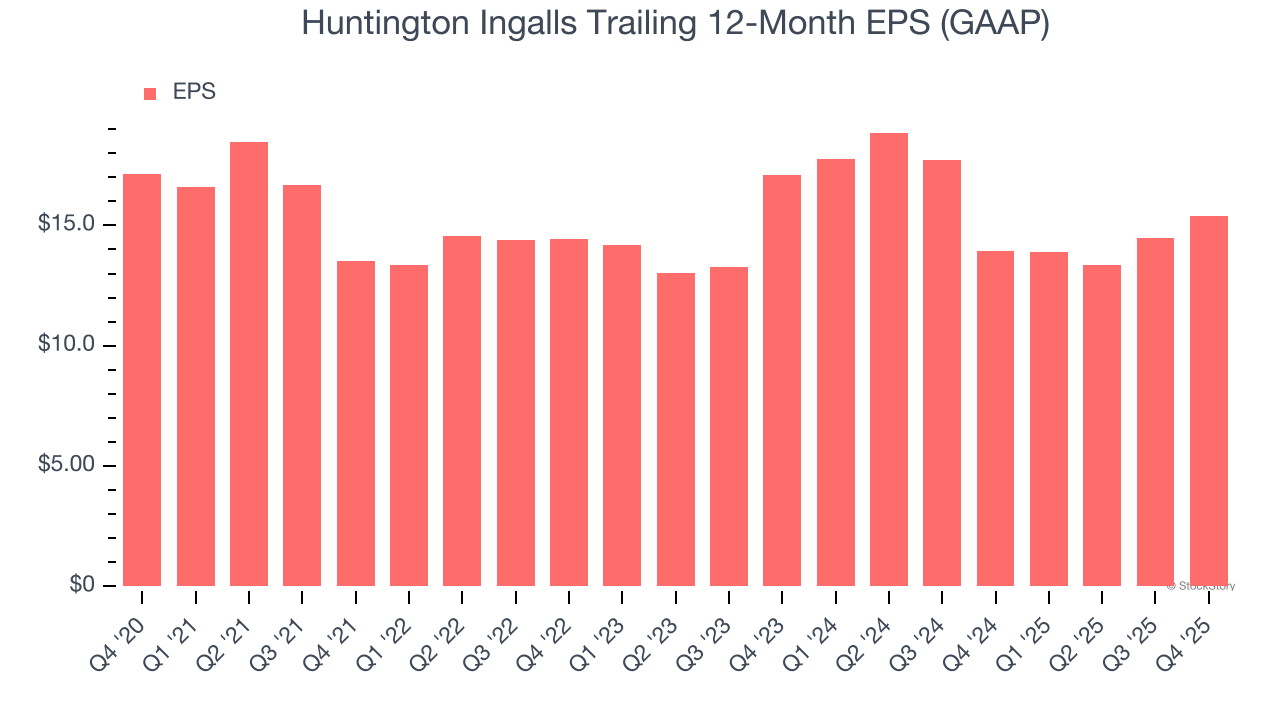

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Huntington Ingalls, its EPS declined by 2.1% annually over the last five years while its revenue grew by 5.9%. However, its operating margin didn’t change during this time, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Huntington Ingalls, its two-year annual EPS declines of 5.2% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Huntington Ingalls reported EPS of $4.04, up from $3.15 in the same quarter last year. This print beat analysts’ estimates by 3.7%. Over the next 12 months, Wall Street expects Huntington Ingalls’s full-year EPS of $15.37 to grow 16%.

We were impressed by how significantly Huntington Ingalls blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The market seemed to be hoping for more, and the stock traded down 10.7% to $368.93 immediately following the results.

Is Huntington Ingalls an attractive investment opportunity at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| Aug-06 | |

| Aug-04 | |

| Aug-03 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite