|

|

|

|

|||||

|

|

|

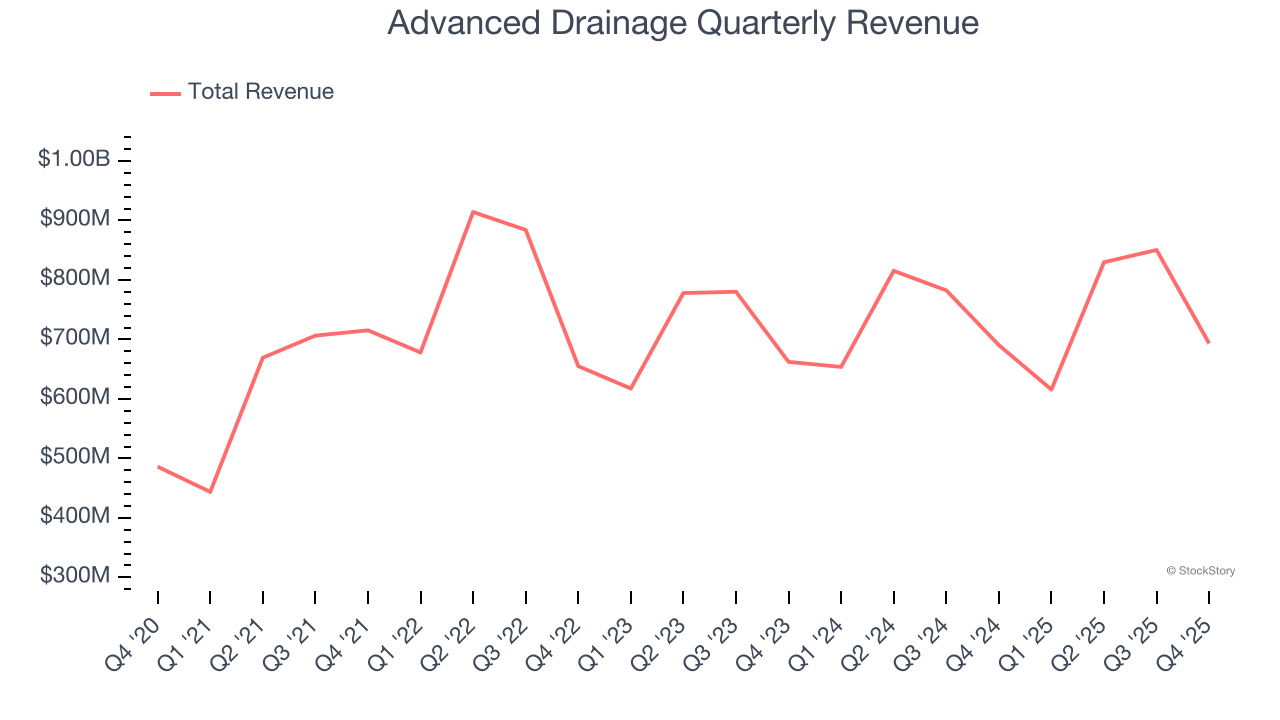

Water management company Advanced Drainage Systems (NYSE:WMS) announced better-than-expected revenue in Q4 CY2025, but sales were flat year on year at $693.4 million. The company’s full-year revenue guidance of $3.02 billion at the midpoint came in 1% above analysts’ estimates. Its non-GAAP profit of $1.27 per share was 14.7% above analysts’ consensus estimates.

Is now the time to buy Advanced Drainage? Find out by accessing our full research report, it’s free.

Scott Barbour, President and Chief Executive Officer of ADS commented, "We delivered our third consecutive strong quarter in a demand environment that is both challenging and mixed by geography. The Infiltrator business and Allied products portfolio grew significantly above-market as we continue to introduce new products, distribution and customer programs. Notably, profitability increased across all facets of the business, including pipe, Allied products and the Infiltrator business. We continue to strategically shift our portfolio mix towards higher margin products, which strengthens the resiliency of our business. This mix shift, in conjunction with favorable price/cost dynamics, resulted in an Adjusted EBITDA margin of 30.2% for the quarter. "

Originally started as a farm water drainage company, Advanced Drainage Systems (NYSE:WMS) provides clean water management solutions to communities across America.

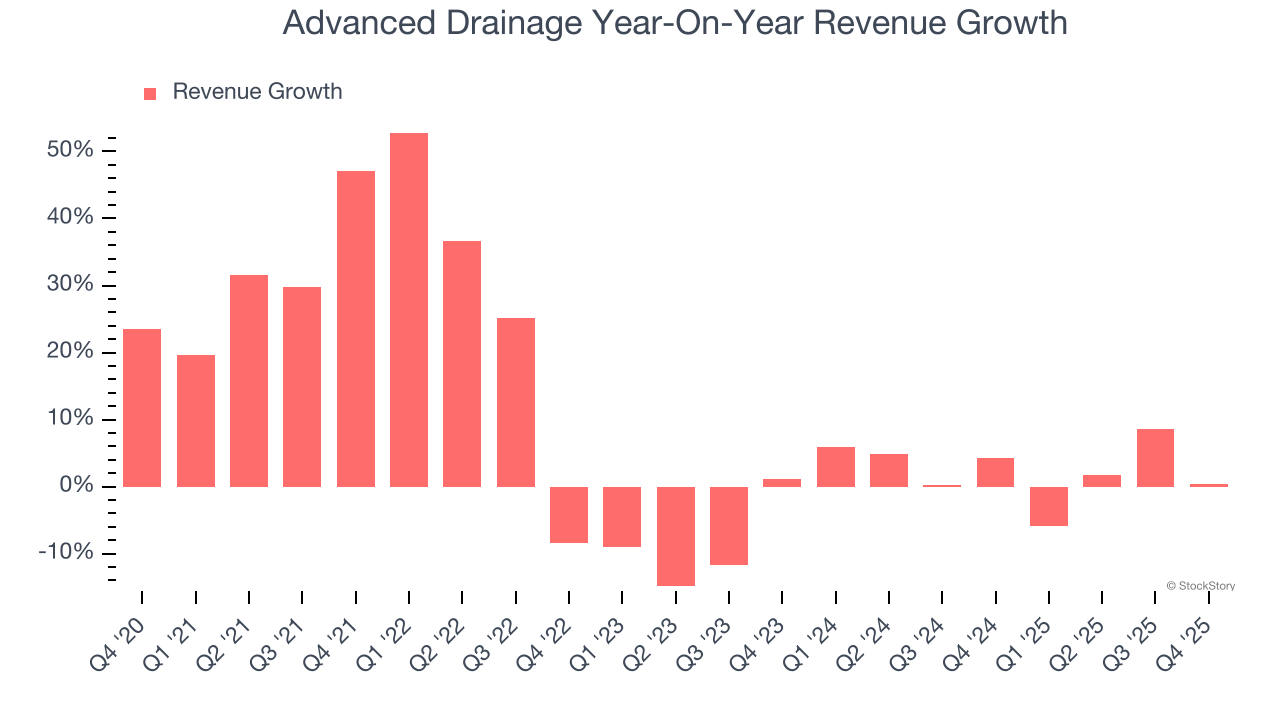

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, Advanced Drainage’s 9.4% annualized revenue growth over the last five years was solid. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Advanced Drainage’s recent performance shows its demand has slowed as its annualized revenue growth of 2.6% over the last two years was below its five-year trend.

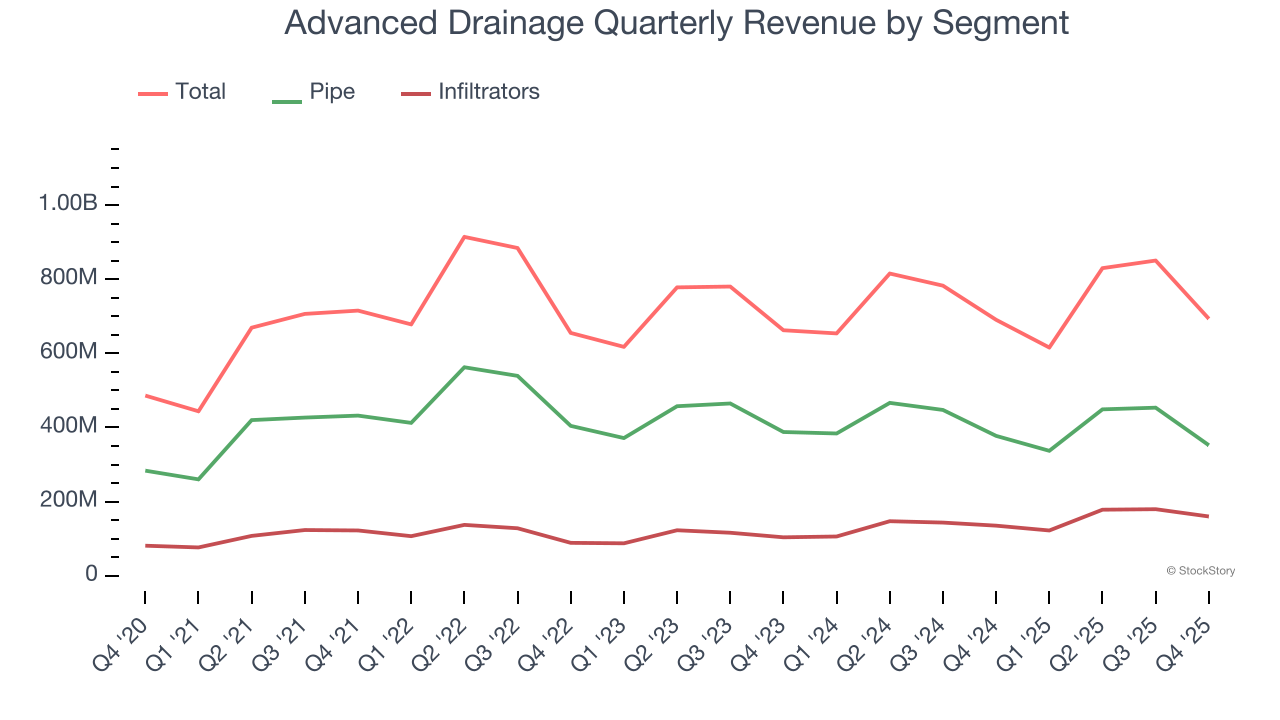

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Pipe and Infiltrators, which are 50.8% and 23.1% of revenue. Over the last two years, Advanced Drainage’s Pipe revenue (thermoplastic corrugated pipes) averaged 2.8% year-on-year declines. On the other hand, its Infiltrators revenue (wastewater treatment systems) averaged 21.8% growth.

This quarter, Advanced Drainage’s $693.4 million of revenue was flat year on year but beat Wall Street’s estimates by 1.1%.

Looking ahead, sell-side analysts expect revenue to grow 3.4% over the next 12 months, similar to its two-year rate. This projection is underwhelming and implies its newer products and services will not lead to better top-line performance yet. At least the company is tracking well in other measures of financial health.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

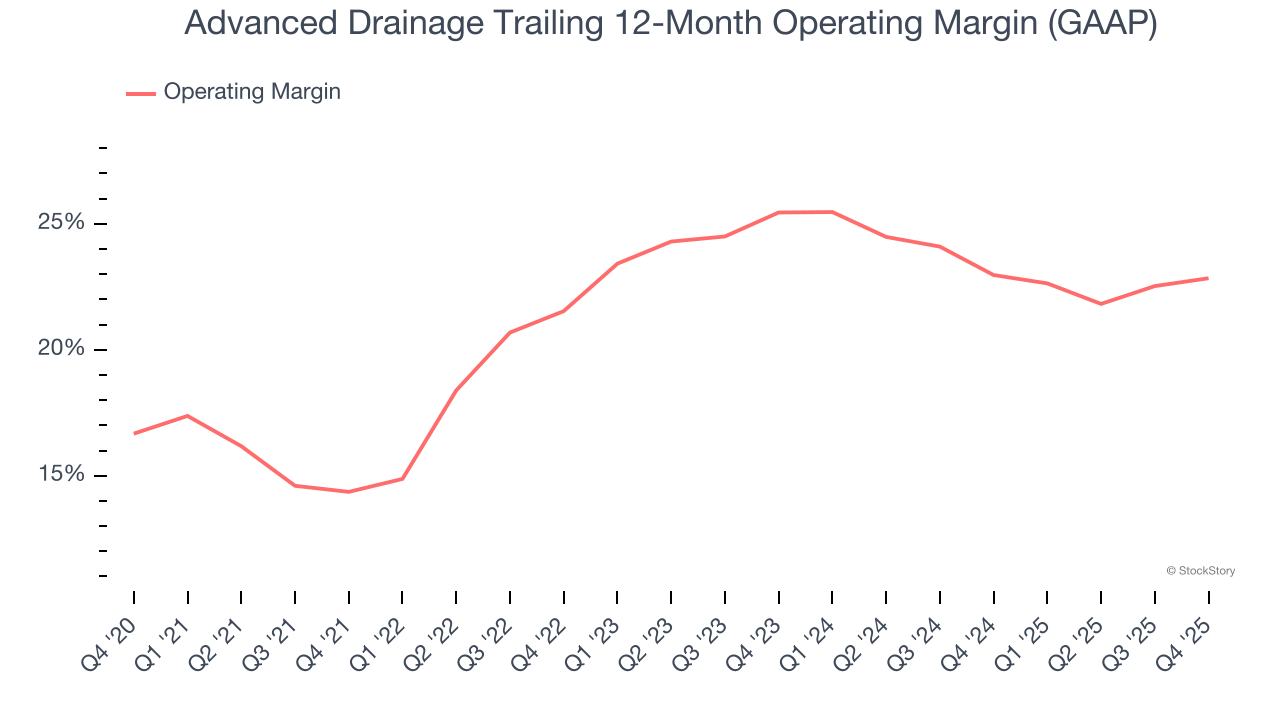

Advanced Drainage has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 21.6%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Advanced Drainage’s operating margin rose by 8.5 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, Advanced Drainage generated an operating margin profit margin of 19.7%, up 1.4 percentage points year on year. Since its gross margin expanded more than its operating margin, we can infer that leverage on its cost of sales was the primary driver behind the recently higher efficiency.

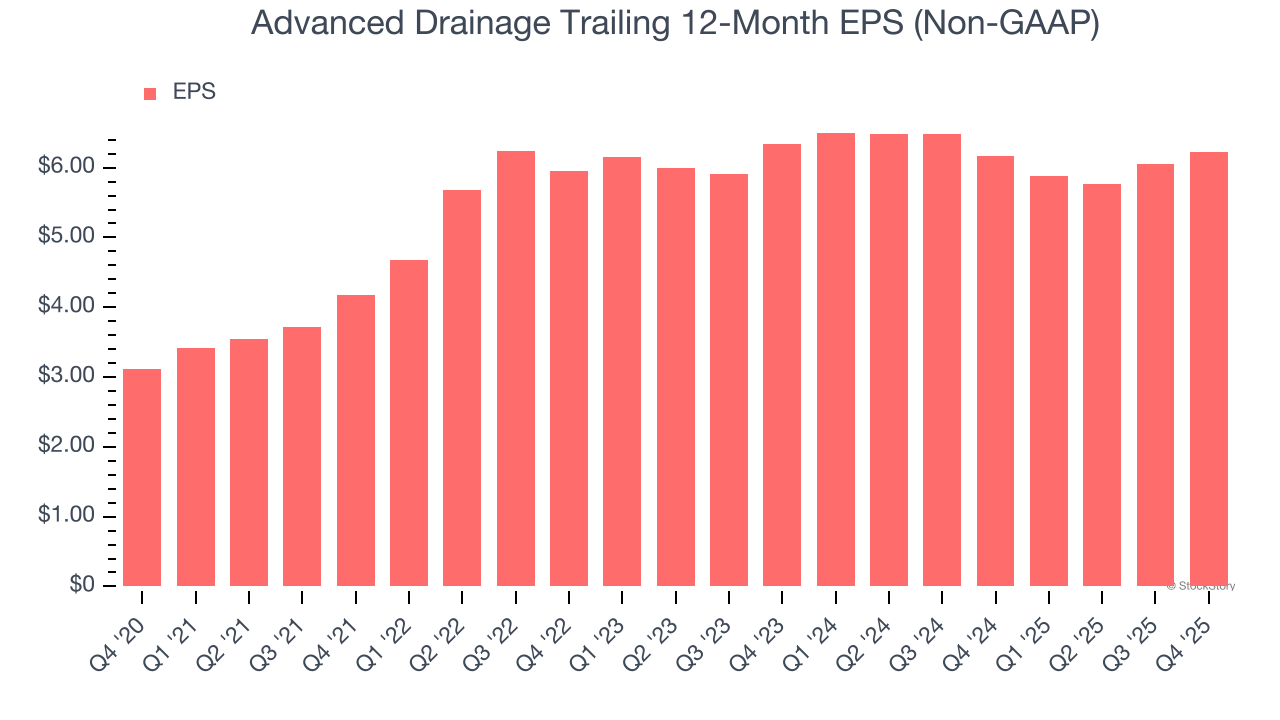

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Advanced Drainage’s EPS grew at a spectacular 14.9% compounded annual growth rate over the last five years, higher than its 9.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into Advanced Drainage’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Advanced Drainage’s operating margin expanded by 8.5 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Advanced Drainage, EPS didn’t budge over the last two years, a regression from its five-year trend. Given the merits in other parts of its business, we’re hopeful it can revert to earnings growth in the coming years.

In Q4, Advanced Drainage reported adjusted EPS of $1.27, up from $1.09 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Advanced Drainage’s full-year EPS of $6.23 to stay about the same.

We were impressed by how significantly Advanced Drainage blew past analysts’ Infiltrators revenue expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. On the other hand, its Pipe revenue missed. Overall, we still think this was a solid quarter with some key areas of upside. The stock remained flat at $160.28 immediately after reporting.

Advanced Drainage put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-16 | |

| Jul-09 | |

| Jun-18 | |

| Jun-11 | |

| May-21 | |

| May-21 | |

| May-21 | |

| May-21 | |

| May-21 | |

| May-21 | |

| Apr-21 | |

| Mar-06 | |

| Mar-05 | |

| Mar-04 | |

| Mar-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite