|

|

|

|

|||||

|

|

|

Pfizer’s PFE fourth-quarter results were strong as it beat estimates for both earnings and sales. Total revenues declined 3% on an operational basis due to a 40% decline in revenues from its COVID-19 products, Comirnaty and Paxlovid. Earnings rose 5% year over year. Pfizer reaffirmed its outlook for 2026, which it had announced in December.

Along with the earnings results, Pfizer announced positive top-line data from a phase IIb VESPER-3 study evaluating monthly maintenance dosing of its ultra-long acting investigational next-generation injectable GLP-1 receptor agonist (RA) called PF-08653944 (PF’3944) in adults with obesity or overweight without type II diabetes. PF’3944 was added to Pfizer’s obesity portfolio with the November 2025 acquisition of obesity drugmaker, Metsera. In the study, PF’3944 delivered robust weight loss with no plateau observed at week 28 while also maintaining competitive tolerability when switching to a 4-fold equivalent monthly dose.

Despite the better-than-expected quarterly results and the positive data from the obesity study, Pfizer’s shares did not show any significant gain in the week post earnings release, confusing investors on how to perceive the quarterly performance.

However, a single quarter’s results are not so important for long-term investors, and the focus should rather be on the company’s strong fundamentals to make an investment decision. Let’s understand the company’s strengths and weaknesses to better analyze how to play Pfizer stock in the post-earnings scenario.

Pfizer is one of the largest and most successful drugmakers in the field of oncology. Its position in oncology was strengthened with the acquisition of Seagen in 2023.

Oncology sales comprise around 27% of its total revenues. Its oncology revenues grew 8% in 2025, driven by drugs like Xtandi, Lorbrena, the Braftovi-Mektovi combination and Padcev. Pfizer has ventured into the oncology biosimilars space and markets six biosimilars for cancer. Its oncology biosimilars contributed $1.3 billion in sales in 2025, rising 26% year over year. Pfizer also advanced its oncology clinical pipeline with several candidates entering late-stage development. By 2030, it expects to have eight or more blockbuster oncology medicines in its portfolio.

Pfizer’s dependence on its COVID business has now reduced. Pfizer’s non-COVID operational revenues are improving, driven by its key in-line products like Vyndaqel, Padcev and Eliquis, new launches and newly acquired products like Nurtec and those from Seagen. Revenues from Pfizer’s non-COVID products rose 6% operationally in 2025. Pfizer's recently launched and acquired products delivered $10.2 billion in revenues in 2025 while growing approximately 14% operationally year over year. In 2026, Pfizer expects its recently launched and acquired products to record continued double-digit growth.

Pfizer is also trying to rebuild its pipeline through acquisitions. Seagen, Metsera and Biohaven are the most significant strategic acquisitions in recent years. In 2025, Pfizer invested around $9 billion in M&A deals, including the acquisition of Metsera and the licensing deal with 3SBio. The November 2025 acquisition of obesity drugmaker, Metsera, has brought Pfizer back into the lucrative obesity space after it scrapped the development of danuglipron, a weight-loss pill, early in 2025. The acquisition has added Metsera’s four novel clinical-stage incretin and amylin programs, which are expected to generate billions of dollars in peak sales.

Pfizer plans to start 20 pivotal studies in 2026, which include 10 pivotal studies for the ultra-long-acting obesity candidates added from the Metsera acquisition and four for PF-08634404, the dual PD-1/VEGF inhibitor in-licensed from Chinese biotech 3SBio in 2025.

Pfizer expects its recently launched and acquired products and a strong pipeline to help revive top-line growth toward the end of the decade.

Pfizer announced its financial guidance for 2026 in December 2025, which fell short of expectations. The company maintained the guidance along with the fourth-quarter results.

Pfizer expects total revenues for 2026 to be between $59.5 billion and $62.5 billion. The range represents a decline from 2025 revenues of $62.6 billion due to lower revenues from COVID products, Comirnaty and Paxlovid, and loss of revenues from the upcoming patent cliff.

In 2026, Pfizer expects adjusted earnings per share in the range of $2.80-$3.00, which represents a decline from the 2025 EPS of $3.22 due to the dilutive impact of 3SBio and Metsera deals, lower COVID revenues and higher taxes.

With the end of the pandemic, sales of Pfizer’s COVID products, Comirnaty and Paxlovid, came down to around $11 billion in 2024 and $6.7 billion in 2025 from $56.7 billion in 2022. Sales of Comirnaty declined in 2025 due to a narrow recommendation for COVID vaccines in the United States, while Paxlovid experienced reduced demand from lower infection rates.

In 2026, Pfizer expects its COVID revenues to be around $5 billion, representing a decline from 2025 COVID sales of around $6.7 billion as COVID infection rates are expected to continue to decline.

Pfizer expects a significant negative impact on revenues from the loss of exclusivity (“LOE”) in the 2026-2030 period as several of its key products, including Eliquis, Vyndaqel, Ibrance, Xeljanz and Xtandi, face patent expirations. The LOE cliff is expected to hurt sales by approximately $1.5 billion in 2026.

Unfavorable impact from the Medicare Part D redesign under the Inflation Reduction Act (IRA) hurt Pfizer’s revenues in 2025. Higher-priced drugs, including Eliquis, Vyndaqel, Ibrance, Xtandi and Xeljanz, are most affected by the IRA. The negative impact is expected to continue in 2026.

Pfizer’s stock has risen 5.2% in the past year compared with an increase of 18.0% for the industry. The stock has also underperformed the sector and the S&P 500, as seen in the chart below.

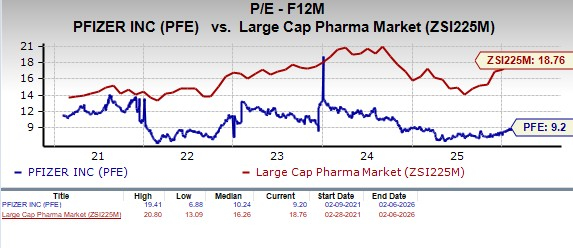

From a valuation standpoint, Pfizer appears attractive relative to the industry and is trading below its five-year mean. Going by the price/earnings ratio, Pfizer’s shares currently trade at 9.20 forward earnings, significantly lower than 18.76 for the industry as well as the stock’s five-year mean of 10.24. The stock is also much cheaper than other large drugmakers like AbbVie ABBV, Novo Nordisk, Eli Lilly LLY, AstraZeneca AZN, J&J and others.

Image Source: Zacks Investment Research

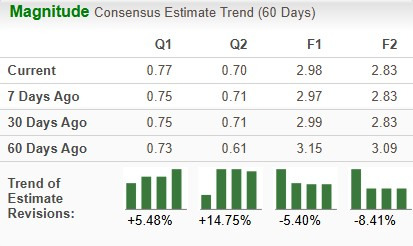

The Zacks Consensus Estimate for 2026 earnings has declined from $2.99 to $2.98 per share over the past 30 days.

Pfizer stock has taken a beating for the past three years as its revenues have declined substantially due to lower sales of its COVID products. In addition, Pfizer faces some other challenges, like U.S. Medicare Part D headwinds and the upcoming LOE cliff in the 2026-2030 period.

The company’s lukewarm guidance has built a negative sentiment around the stock. The declining estimates for 2026 also reflect analysts’ pessimistic outlook for the stock. It remains to be seen if Pfizer’s key drugs like Vyndaqel and Padcev, and its recently launched and acquired products, help the company offset its LOEs over the next several years.

It might be a good idea for short-term investors to avoid this Zacks Rank #5 (Strong Sell) stock for now. However, long-term investors may continue to hold the stock in their portfolio as Pfizer rebuilds its pipeline in oncology and obesity, which it believes can drive growth in 2028 and beyond.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 32 min | |

| 47 min | |

| 57 min | |

| 59 min | |

| 1 hour | |

| 1 hour | |

| 1 hour |

Novo Nordisk Files Deceptive Advertising Lawsuit Against Rival Eli Lilly

LLY

The Wall Street Journal

|

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 9 hours | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite