|

|

|

|

|||||

|

|

|

Applied Materials AMAT is scheduled to report first-quarter fiscal 2026 results on Feb. 12.

For the fiscal first quarter, AMAT expects revenues to be $6.85 billion (+/- $500 million). The Zacks Consensus Estimate for revenues is pegged at $6.89 billion, suggesting a decline of 3.87% from the year-ago quarter’s reading.

Applied Materials projects non-GAAP earnings to be $2.18 (+/- $0.20). The Zacks Consensus Estimate for earnings is pegged at $2.19 per share, indicating a decline of 7.98% from the year-ago quarter’s reported figure. The figure has remained unchanged in the past 60 days.

AMAT has an impressive earnings surprise history. AMAT beat the Zacks Consensus Estimate in each of the past four quarters, with an average earnings surprise of 4.17%.

Applied Materials, Inc. price-eps-surprise | Applied Materials, Inc. Quote

Our proven model predicts an earnings beat for AMAT this earnings season. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat, which is the case here.

Earnings ESP: Earnings ESP, which represents the difference between the Most Accurate Estimate ($2.26 per share) and the Zacks Consensus Estimate ($2.19 per share), is +3.06%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Zacks Rank: AMAT carries a Zacks Rank #2 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

AMAT’s wafer fabrication equipment (WFE) is experiencing increased demand due to a rise in the usage of semiconductors in artificial intelligence and high performance computing (HPC). In the previous quarter, AMAT reported that its leading-edge foundry/logic, DRAM and advanced packaging will be the fastest-growing areas of the WFE market.

AMAT’s flash memory or NAND sales nearly doubled to $1.41 billion in fiscal 2025 from the year-ago sales of $747.4 million. Although AMAT has a lower market share in the NAND space, it is gaining prominence. This trend is likely to have persisted in the to-be-reported quarter, supporting AMAT’s top-line growth.

Applied Materials’ leadership in GAA transistors at 2nm and below, Backside power delivery, Advanced wiring and interconnect, HBM stacking and hybrid bonding and 3D device metrology, which are indispensable for manufacturing next-generation semiconductor chips, are likely to have driven AMAT’s semiconductor segment in the fiscal first quarter.

AMAT’s display business has rebounded in the fiscal 2025 with year-over-year growth of 19.8%. In the fourth quarter of fiscal 2025, the display revenues grew 68.2% year over year as Applied Materials shipped a richer mix of advanced systems and increased prices broadly. These factors are likely to have benefited AMAT’s corporate and other segment’s revenues.

The company’s Applied Global Services segment is also likely to have seen steady growth, aided by strong demand for comprehensive service agreements and the expansion of its subscription-based business.

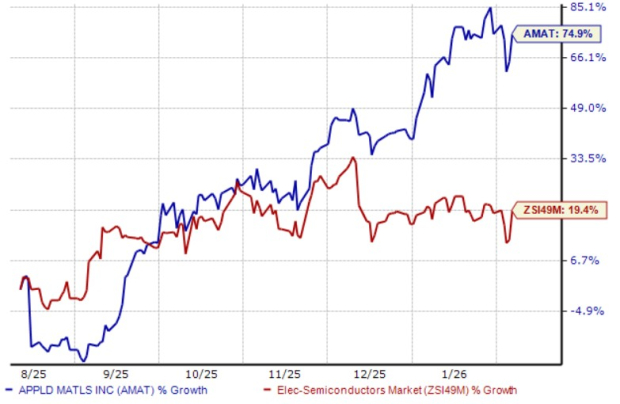

Applied Materials shares have gained 74.9% over the past six months, outperforming the Zacks Electronics – Semiconductors industry, which has gained 19.4%.

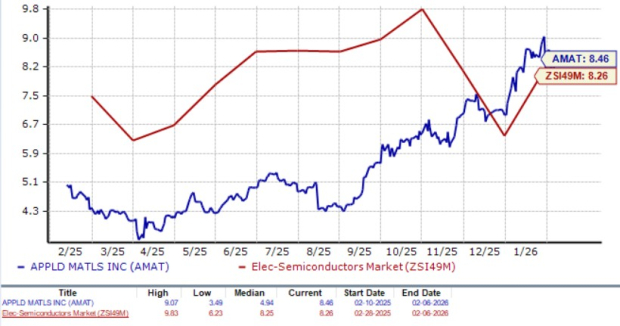

Let us now look at the value Applied Materials offers to its investors at current levels. AMAT is currently trading at a premium with a forward 12-month price-to-sales (P/S) of 8.46X compared with the industry’s 8.26X.

Applied Materials operates in a highly competitive market space where it faces competition from players, including Lam Research LRCX in the semiconductor space, ASML Holding ASML in the photolithography and advanced manufacturing equipment segment. KLA Corporation KLAC is a dominant competitor in the wafer inspection space.

For instance, Lam Research develops Atomic Layer Deposition tools like AT200M, AT410 and AT650P that are similar to the devices made by AMAT. Both ASML and AMAT specialize in advanced semiconductor nodes, although developing solutions for various stages of semiconductor production. ASML Holding develops lithography solutions, including EXE and NXE systems.

Applied Materials and KLA Corporation offer similar solutions, such as Wafer Inspection, Yield Enhancement and Process Control inspection systems. KLA Corporation develops inspection systems, including 3935 and 3920 EP broadband plasma defect inspection systems. Although Applied Materials is dealing with a broader market sell-off and growing competition, not everything is gloom and doom for the company.

Applied Materials leads the market with its superior design wins. It is well-positioned to capitalize on the technology-inflection-led growing demand for next-generation chips on the back of its product innovations and leadership in leading-edge logic, compute memory, high bandwidth memory and advanced packaging.

AMAT is likely to capitalize on AI-driven semiconductor demand. The company has made significant strides in cutting-edge chip manufacturing, particularly in gate-all-around (GAA) transistors, high-bandwidth memory and advanced packaging. These innovations are critical to enabling faster, more energy-efficient AI processing.

AMAT is gaining from continuous strength across wafer fabrication equipment for foundry/logic, DRAM, NAND, flash memory, GAA and advanced packaging driven by increased usage of semiconductors in artificial intelligence and HPC. AMAT’s HBM stacking and hybrid bonding and 3D device metrology technologies are indispensable for manufacturing next-generation semiconductor chips. Considering these factors, we suggest investors buy this stock now.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| 3 hours | |

| 5 hours | |

| 10 hours | |

| 10 hours | |

| 12 hours | |

| 12 hours | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-08 | |

| Aug-08 | |

| Aug-08 | |

| Aug-07 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite