|

|

|

|

|||||

|

|

|

Ciena Corporation CIEN stock has gained 210.2% in the past six months, outperforming the Zacks Computer & Technology sector and the Zacks Communication - Components industry’s growth of 11.1% and 123.3%, respectively. The S&P 500 composite has also risen 11.7% over the same time frame. The company’s shares have climbed 23.6% in the past month.

CIEN has outpaced its peers, Cisco Systems, Inc. CSCO, Nokia NOK and Arista Networks, Inc. ANET. CSCO, NOK and ANET have climbed 24.2%, 76.3% and 3%, respectively, in the past six months.

Ciena continues to benefit from increased network traffic, demand for bandwidth and the adoption of cloud architecture. CIEN is currently trading at $289.68 and has a 52-week high of $297.01.

Following a strong rally, investors may wonder whether CIEN still has upside or if expectations have outpaced fundamentals. Let’s break down to see what’s driving the rally, the bull and bear cases, and a practical approach to managing risk and position size.

Ciena continues to benefit from higher network traffic and demand for bandwidth, which are mainly attributed to increasing AI technology use cases. Ciena’s Cloud and Service Provider customers are prioritizing network investments to support AI-driven traffic growth, highlighting long-term opportunities for its Systems and Interconnects businesses. To capitalize on this, it is focusing R&D on Coherent Optical Systems, Interconnects, Coherent Routing, and solutions like DCOM, while scaling back investments in residential broadband. Blue Planet plays a key role in major provider projects, supporting digital transformation with AI and data-driven tools.

With a $5 billion backlog, including $3.8 billion in hardware and software, Ciena has solid support for 2026 revenue and clear demand signals into 2027 and beyond. Management is taking steps to offset input cost pressures through supply rebalancing, cost reductions and pricing actions, with benefits expected to emerge in late fiscal 2026. As these measures take effect, margins are expected to improve from the first half to the second half of the year.

Ciena Corporation price-consensus-chart | Ciena Corporation Quote

Also, the company is benefiting from strong demand for packet optical transport, switching products, integrated networking solutions and service management software. Its expanding presence in data center connectivity has increased exposure to a broader, end-to-end optical and data equipment market. The company remains a leading supplier of 40G and 100G optical transport technologies, while Fiber Deep represents a meaningful opportunity supported by widespread adoption among major global cable operators.

Ciena’s portfolio, including WaveLogic, Reconfigurable Line System (RLS), Navigator and Interconnect Solutions, remains a recognized industry standard, with WaveLogic 6 and RLS giving it a technology lead and strong positioning to serve global AI network opportunities. The WaveLogic 6 Extreme deployment enabling Poland’s first 1.2 Tb/s optical transmission highlights its technology leadership. Additionally, the Nubis acquisition strengthens AI interconnect capabilities, while continued investments in routing, switching, subsea, long-haul, metro data center interconnect (DCI) and managed optical fiber networks (MOFN) support long-term growth opportunities.

Ciena expects fiscal 2026 revenues of $5.7-$6.1 billion, or roughly 24% growth at the midpoint, up from the 17% outlook issued in September. The company continues to expect gross margins to rise to 43% (+/-1%) in fiscal 2026. It expects the fiscal 2026 operating margin to improve further to 17% (+/-1 pt).

For the first quarter of fiscal 2026, management expects revenues in the range of $1.35-$1.43 billion. The adjusted gross margin is estimated between 43% and 44%. Adjusted operating margin estimated at 15.5-16.5%. The company is scheduled to report fiscal first-quarter results on March 5, 2026.

Ciena continues to incur a lumpsum amount of expenses, primarily due to strategic investments in its business expansion and technology enhancements. Fiscal fourth-quarter adjusted operating expenses jumped 15.2% year over year to $408.7 million, coming in above the $390–$400 million guidance, mainly due to higher incentive payouts tied to orders and financial results. The company is encountering near-term pressure from NPI ramp challenges and escalating input costs, as tightening supply constraints struggle to keep pace with surging demand. Ciena forecasts $250–$275 million in fiscal 2026 capex, well above historical levels, pressuring near-term cash flow as the company absorbs higher investment requirements and rising 3-nanometer mask set costs.

In addition, a significant portion of Ciena’s revenue is derived from a limited number of large global communications service providers. Given the highly competitive industry landscape, the loss of any major customer could materially affect the company’s performance.

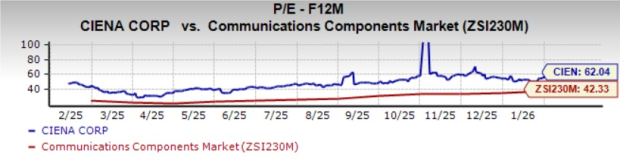

CIEN trades at a forward 12-month price-to-earnings (P/E) of 62.04X, above the industry’s 42.33X. CSCO, NOK and ANET trades at a forward 12-month P/E ratio of 25.37X, 18.45X and 47.24X, respectively.

The Zacks Consensus Estimate for CIEN’s earnings for fiscal 2026 has been revised upward over the past 60 days.

CIEN is treading in the middle of the road. Growth is supported by rising network traffic, strong bandwidth demand and increasing adoption of cloud architectures, reinforced by a solid outlook and upward earnings estimate revisions. However, these positives are tempered by a relatively expensive valuation, rising cost pressures and risks related to customer concentration.

Existing investors may consider holding their positions, while new investors could wait for a better entry point.

CIEN currently carries a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 15 hours | |

| Jul-18 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite