|

|

|

|

|||||

|

|

|

Lumentum Holdings LITE shares have surged 24% following the release of its second-quarter fiscal 2026 results on Feb. 4, 2026. The uptick can be attributed to a remarkable 65.5% top-line growth, which beat the Zacks Consensus Estimate by 1.85%. EPS of $1.67 surpassed the consensus mark by 18.68%. This exceptional performance reflects accelerating demand for optical connectivity solutions powering AI infrastructure, successful execution across multiple product lines and the company's strategic positioning as a foundational technology provider to hyperscale data center customers.

LITE shares have appreciated 128.6% over the past three months, significantly outperforming the Zacks Computer and Technology sector's decline of 1.3% and the Communication - Components industry's advance of 44.8%. The stock has substantially outpaced peers, with Coherent Corp. COHR shares advancing 53.4%, Broadcom AVGO declining 2%, and Marvell Technology MRVL declining 7.9% over the same period. This remarkable outperformance reflects the company's technology leadership in ultra-high-power lasers and early mover advantage in optical circuit switches, positioning it as a critical supplier for AI data center connectivity.

The fiscal second-quarter results mark a significant inflection point for LITE, driven by strengthening demand for AI infrastructure connectivity solutions. Robust revenue growth reflects accelerating customer adoption of optical technologies that address bandwidth and power efficiency challenges in modern AI workloads. The balanced contributions from Components at $443.7 million and Systems at $221.8 million indicate broad-based strength across the value chain. The company's technology leadership in high-speed optical components has positioned it as an essential supplier to hyperscale customers deploying next-generation network architectures.

Profitability improved dramatically, with non-GAAP operating margin reaching 25.2%, an expansion of 1,730 basis points year over year. This margin expansion reflects operational leverage as production scales, strategic pricing power enabled by tight supply conditions and a favorable product mix shift toward advanced offerings like 200-gigabit lane speed devices. LITE expects robust momentum to continue, with revenues anticipated at $780-830 million for the fiscal third-quarter. Operating margin is projected to expand further to 30-31%, while EPS is expected at $2.15-2.35. This outlook represents meaningful acceleration, which reflects intensifying AI infrastructure investments by hyperscale operators, successful capacity expansion initiatives and the company's broadening product portfolio across optical circuit switches, co-packaged optics and cloud transceivers.

The Zacks Consensus Estimate for fiscal third-quarter EPS is pegged at $2.24, up by 47.4% over the past 30 days. The figure indicates 292.98% growth year over year.

Lumentum Holdings Inc. price-consensus-chart | Lumentum Holdings Inc. Quote

LITE has become a key technology provider for AI networks, benefiting from the shift toward optical connectivity solutions. Traditional electrical switches struggle with the bandwidth and power needs of AI training clusters, driving demand for Optical Circuit Switches (OCS). OCS technology allows hyperscale operators to dynamically reconfigure network setups and optimize resources based on changing workload demands. The OCS business has emerged as a major growth driver, with fiscal second-quarter revenue surpassing $10 million three months earlier than expected. The order backlog has jumped past $400 million, positioning LITE to exit 2026 at a quarterly OCS run rate well above the earlier $100 million target.

Co-packaged optics (CPO) and cloud transceivers represent additional growth opportunities reshaping data center connectivity. CPO integrates optical connections directly into processor packages, cutting power use and boosting performance as AI systems become more densely packed. LITE has secured a multi-hundred-million-dollar purchase order for ultra-high-power lasers supporting CPO applications, with deliveries expected in the first half of 2027. The transceiver business has rebounded strongly, with fiscal second-quarter revenue exceeding previous levels as customers shift to 1.6-terabit speeds. LITE competes effectively with Broadcom, Marvell Technology and Coherent Corp. across these segments, with higher-speed products commanding better prices and manufacturing improvements strengthening profit margins.

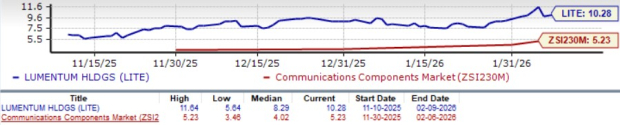

LITE is trading at a forward 12-month price-to-sales of 10.28x, above the sub-industry average of 5.23x and sector average of 6.49x. Among peers, Broadcom commands 15.42x, while Coherent Corp. trades at 5.85x and Marvell Technology at 6.9x. The premium valuation appears justified given the company's exceptional fundamentals, including revenue growth exceeding 85% year over year, operating margins expanding toward 30% and diversified revenue streams across optical circuit switches, co-packaged optics and cloud transceivers.

LITE demonstrates exceptional execution with strong fiscal second-quarter performance and substantially increased forward guidance. The company's diversified portfolio across optical circuit switches, co-packaged optics and cloud transceivers, backed by an order backlog exceeding $400 million, provides strong revenue visibility into 2027. The early mover advantage in OCS and technology leadership position LITE favorably against peers. Despite the recent rally, the premium valuation appears justified given exceptional growth trajectory, rapidly expanding profitability and strategic positioning within the multi-year AI infrastructure buildout cycle.

Lumentum Holdings currently sports a Zacks Rank #1 (Strong Buy) and a Growth Score of B, a favorable combination that offers a strong investment opportunity, per the Zacks Proprietary methodology. You can see the complete list of today's Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 36 min | |

| Jul-26 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite