|

|

|

|

|||||

|

|

|

Amphenol’s APH AI-driven datacom momentum is transforming its growth profile, with recent fourth-quarter results indicating a capacity-driven infrastructure shift rather than a short-term surge. IT datacom — the segment most exposed to AI infrastructure — generated triple-digit organic growth, fueled by high-speed and power interconnect products supporting next-generation data centers. Record bookings and a strong book-to-bill ratio are aligned with AI investment cycles, as customers extend commitments for large-scale system buildouts. This visibility reflects multi-quarter capacity planning, confirming demand tied to expansion initiatives and supporting revenue durability.

Amphenol is deepening its competitive positioning amid this demand expansion. The inclusion of CommScope’s CCS business enhances its fiber, copper and power connectivity portfolio, positioning the company to serve a wider range of AI datacenter architectures. AI workloads are simultaneously increasing performance thresholds, reinforcing the importance of Amphenol’s mission-critical interconnect solutions. Segment performance shows communications and datacom contributing a rising portion of total revenues, highlighting a structural mix shift toward high-growth markets. Management expects IT datacom demand to remain elevated, backed by continued AI deployments and investment plans.

Record AI-driven bookings combined with portfolio expansion and strong execution suggest Amphenol’s datacom momentum is tied to long-cycle infrastructure spending. Management’s first-quarter 2026 revenue outlook of $6.9-$7 billion further underscores this acceleration. Amphenol is positioned to benefit from an extended AI buildout, supporting durable long-term growth. This backdrop lays the foundation for sustainable top-line expansion going forward.

Amphenol operates in a highly competitive AI infrastructure market, contending with strong rivals such as TE Connectivity TEL and Broadcom AVGO.

TE Connectivity is emerging as a strong rival to Amphenol in AI infrastructure by focusing on high-density data and power connectivity for hyperscale systems. Rapid AI program wins and early co-design partnerships embed TEL into customer roadmaps, increasing switching costs and margin leverage. Its platform-level integration and scalable manufacturing intensify competitive pressure on Amphenol, as TEL strengthens its position in next-generation AI rack connectivity.

Broadcom poses a strong competitive challenge to Amphenol in AI infrastructure, controlling the silicon, switching and optical technologies that form hyperscale AI architectures. The growth of AI switches and custom accelerator solutions places Broadcom at the core of cluster design decisions. This ecosystem control indirectly pressures Amphenol’s interconnect positioning, as Broadcom continues to build the backbone of next-generation AI clusters.

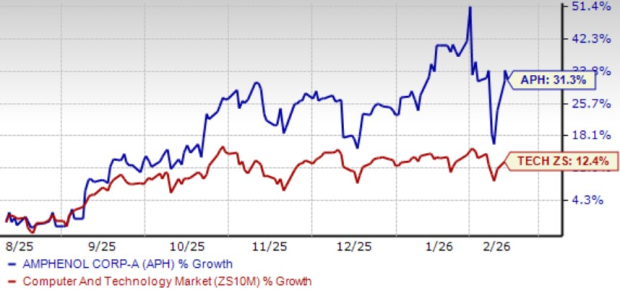

Amphenol’s shares have gained 31.3% over the past six months, outperforming the broader Zacks Computer and Technology sector’s 12.4% growth.

Amphenol shares are trading at a premium, as suggested by a Value Score of D. In terms of the forward 12-month price-to-earnings (P/E), APH is trading at 32.65X, higher than the sector’s 25.91X.

The Zacks Consensus Estimate for Amphenol’s 2026 earnings is pegged at $4.32 per share, up 6.4% over the past 30 days. The figure indicates a 29.34% increase year over year.

APH currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 29 min | |

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 8 hours | |

| 8 hours | |

| 9 hours | |

| 11 hours | |

| 12 hours | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite