|

|

|

|

|||||

|

|

|

CONMED Corporation CNMD is well-positioned for growth on the back of rising adoption of its high-margin, differentiated platforms like AirSeal, Buffalo Filter and BioBrace. The company’s long-term prospects seem good as robotic procedure volume rises, coupled with the expanding penetration of Ambulatory Surgery Centers. Moreover, improving supply-chain bottlenecks should drive top- and bottom-line growth.

Meanwhile, CONMED is facing tariff headwinds that are unfavorably impacting its EPS and revenue expansion. Higher operating expense investments and the company’s operation in a stiff competitive and regulatory requirement space remain a concern.

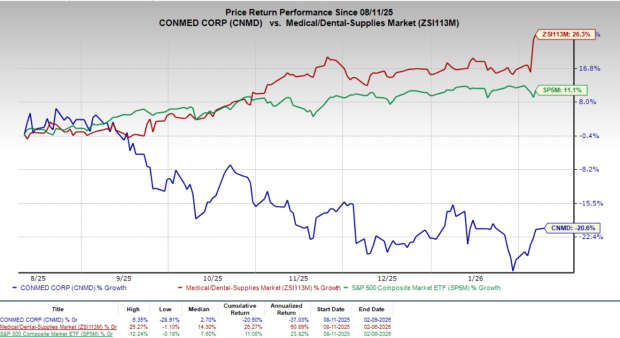

Shares of this Zacks Rank #3 (Hold) company have lost 20.6% in the past six months against the industry’s 26.3% growth and the S&P 500 Index’s 11.1% rise.

CONMED, a renowned global medical products manufacturer specializing in surgical instruments and devices, has a market capitalization of $1.29 billion. The company projects 5.2% earnings growth over the next five years.

Its earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 7.56%.

Strong Growth Drivers in High-Margin Segment: CONMED delivered solid fourth-quarter fiscal 2025 results, driven primarily by strong orthopedic performance, operational execution and continued expansion of its higher-growth, higher-margin product platforms. For fiscal 2026, management emphasized that the company will continue concentrating on investments and commercial execution on its three core high-growth platforms — AirSeal insufflation systems, Buffalo Filter and the BioBrace — as these categories combine attractive procedural growth with strong margin profiles.

CONMED highlighted that AirSeal remains underpenetrated in traditional laparoscopy, where it is currently used in only about 6%-7% of the more than 3 million annual laparoscopic procedures in the United States. This underpenetration is expected to provide a substantial long-term growth runway as clinical awareness and commercial coverage increase.

Buffalo Filter remains a key long-term growth driver, supported by a surgical smoke evacuation market exceeding $1 billion globally. Regulatory momentum is strengthening demand, with 20 states of the United States implementing smoke-free operating room legislation, alongside growing adoption in Nordic countries and Canada. The company’s newly launched next-generation PlumeSafe X5 system offers quieter operation, faster smoke clearance and improved performance, enhancing both clinical and economic value for healthcare providers.

BioBrace, a key growth platform, is utilized in more than 70 surgical procedures, reflecting broad adoption and technology versatility. The launch of the BioBrace RC delivery system has improved reproducibility in rotator cuff repairs and expanded surgeon access. Clinical validation continues to strengthen, with a 268-patient randomized trial ongoing and guideline support emerging. Utilization is also increasing in foot and ankle procedures, with expanding adoption expected to support improved healing outcomes and lower revision rates.

Together, these drivers reinforce CONMED’s strategy to concentrate on R&D spending, sales resources and capital investments on these higher-margin growth engines throughout fiscal 2026 and beyond.

Supply-Chain Normalization Boosting Orthopedics Recovery: Resolving the sports medicine supply-chain constraints remains a central operational priority entering fiscal 2026 and beyond. During fiscal 2025, the company invested in additional planning capabilities, infrastructure, external operational expertise and leadership resources, including back-order levels and the number of affected SKUs declining to a three-year low by year-end.

This improvement enabled the orthopedics segment to return to stronger growth, with fourth-quarter orthopedic sales rising 12.1% in constant currency, reflecting both improving product availability and continued demand for key offerings such as BioBrace and other soft-tissue repair solutions.

Management’s near-term objective is to stabilize and scale supply processes to ensure consistent product availability, while the long-term objective is to build a more agile, data-driven, high-performance supply chain to support sustained innovation and above-market growth in the orthopedic portfolio over time.

Margin Improvement Initiatives and Capital Returns: Several structural actions underway are expected to strengthen profitability and shareholder returns beginning in fiscal 2026 and continuing thereafter. The strategic exit from the gastroenterology product lines is intended to concentrate resources on higher-growth, higher-margin businesses and is expected to improve the company’s consolidated long-term gross margin profile by 80 bps once the transition is completed.

For fiscal 2026, CONMED guided to an additional 50 to 100 basis points of gross-margin expansion, driven by favorable product mix and cost improvements. The company suspended its dividend and authorized a $150 million share repurchase program, with management indicating that redeploying the prior dividend amount toward buybacks is expected to contribute 7 cents of EPS accretion in fiscal 2026, supporting ongoing capital-return priorities while maintaining flexibility to invest in innovation and growth initiatives.

Revenue & EPS Headwinds From GI Exit and Tariffs: While CNMD has taken steps for strong long-term growth and profitability opportunities, temporary headwinds associated with strategic portfolio actions and external cost pressures remain a concern. Management guided that fiscal 2026 revenue growth is expected to remain moderate, with constant-currency organic growth projected at 4.5% to 6%, reflecting the impact of portfolio actions and the transition away from lower-priority product lines. U.S. general surgery performance has been affected by portfolio rationalization, including the exit of certain smaller product lines, reduced emphasis on OEM smoke-evacuation offerings and the broader strategic decision to exit the gastroenterology business.

Adjusted EPS is expected to be in the range of $4.30 to $4.45 for fiscal 2026 compared with $4.59 in fiscal 2025, reflecting the impact of the company’s planned exit from the gastroenterology product lines, which is projected to reduce fiscal 2026 earnings by 45-50 cents per share and incremental tariff-related costs expected to create an additional 30-35 cents per share headwind. While these factors weigh on near-term earnings, management emphasized that the GI exit is a deliberate strategic decision designed to improve long-term margin quality and focus investments on higher-growth platforms.

Rising Operating Expense Investments: Operating expenses are expected to rise in fiscal 2026 as the company increases investments to accelerate its core growth platforms and innovation pipeline. Adjusted SG&A expense is projected to increase to 38.0% to 38.5% of sales, reflecting both lower revenues following the GI portfolio exit and increased commercial spending to support expansion of key surgical and orthopedic franchises. R&D spending is expected to rise 4.5% to 5% of sales, representing a step-up from prior years as CNMD directs additional resources toward product development, clinical evidence generation and technology innovation in areas such as robotic and laparoscopic surgery, smoke evacuation and soft-tissue repair.

Strong Competition in Targeted Markets: CONMED operates in highly competitive markets against large, diverse device companies and specialized surgical firms. In general surgery, its AirSeal system competes with insufflation platforms from Medtronic and J&J’s Ethicon, while smoke-evacuation products face increasing competition from Stryker and Olympus despite Buffalo Filter’s leadership position. In orthopedics, the company competes with Stryker, Zimmer Biomet, Smith & Nephew and Arthrex across sports medicine, biologics and extremities, including the fast-growing foot and ankle segment. Although smaller in scale, CONMED focuses on differentiated, high-growth niches supported by innovation and regulatory tailwinds to drive market share gains against larger competitors.

CONMED Corporation price | CONMED Corporation Quote

CONMED is witnessing a declining estimate revision trend for fiscal 2026. In the past 60 days, the Zacks Consensus Estimate for earnings has moved south 25 cents to $4.36 per share.

The Zacks Consensus Estimate for first-quarter fiscal 2026 revenues and EPS is pegged at $310.7 million and 82 cents, respectively, suggesting 3.3% and 13.7% declines from the year-ago reported numbers.

Some better-ranked stocks in the broader medical space are Intuitive Surgical ISRG, Align Technology ALGN and Cardinal Health CAH.

Intuitive Surgical, sporting a Zacks Rank #1 (Strong Buy) at present, has an estimated long-term growth rate of 15.7%. ISRG’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 13.2%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Intuitive Surgical’s shares have gained 4.4% against the industry’s 0.7% decline over the past six months.

Align Technology, carrying a Zacks Rank of 2 (Buy) at present, has an estimated long-term growth rate of 10.1%. ALGN’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 6.2%.

ALGN’s shares have climbed 42.8% compared with the industry’s 26.2% growth over the past six months.

Cardinal Health, currently carrying a Zacks Rank #2, has an estimated long-term growth rate of 14.8%. CAH’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 9.3%.

CAH’s shares have rallied 43.2% compared with the industry’s 26.2% growth over the past six months.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 12 min | |

| 31 min | |

| 36 min | |

| 2 hours | |

| 3 hours | |

| Aug-03 | |

| Aug-03 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite