|

|

|

|

|||||

|

|

|

In the competitive world of fresh produce, Mission Produce Inc. AVO and Limoneira Company LMNR represent two distinct paths to growth. Mission Produce has emerged as a global powerhouse in avocados, operating one of the world’s largest vertically integrated avocado networks. With sourcing, farming, packing and ripening operations spanning North America, Latin America, Europe and Asia, Mission Produce commands a strong position in the rapidly expanding global avocado market. Its scale and year-round supply capabilities give it meaningful leverage with major retailers and foodservice players.

Limoneira, in contrast, is a diversified agribusiness best known for its leadership in lemons, alongside avocado production and valuable agricultural real estate assets. While smaller in global scale, Limoneira maintains a solid foothold in the U.S. citrus market and differentiates itself through land monetization strategies and joint ventures.

This face-off highlights a battle of focus versus diversification — global avocado dominance against a multi-crop agricultural model competing for share in evolving fresh produce markets.

Mission Produce has firmly established itself as a global leader in avocados, leveraging scale, vertical integration and international reach to command a meaningful position in a fast-growing category. The company has built one of the most comprehensive avocado platforms in the world, moving hundreds of millions of pounds annually through its marketing and distribution network. In fiscal 2025, the company delivered record revenues of $1.39 billion, up 13% year over year, driven by a 7% increase in avocado volumes to a record 691 million pounds sold.

Management consistently emphasizes its volume-driven model and ability to influence category growth rather than simply react to pricing swings. In fiscal 2025, its International Farming segment more than doubled exportable Peruvian avocado production to approximately 105 million pounds from 43 million pounds last year. With avocados now penetrating roughly 70% of U.S. households and management targeting further gains toward 73-75% over the next few years, Mission Produce is positioned to capture incremental share in a category still expanding globally.

Mission Produce’s strength lies in its integrated global platform, spanning sourcing, owned farming, packing, ripening, distribution and category management. This structure allows it to pivot across geographies in real time, optimize per-unit margins and program fruit where it creates the most value. Its expansion in Europe and Asia, combined with infrastructure investments in the U.K., Guatemala and North America, strengthens its international market position and deepens customer penetration.

Beyond avocados, Mission Produce is scaling adjacent categories like mangoes, where it has grown share and increased household penetration using the same consumer engagement and programming playbook. Blueberries add further portfolio diversification, anchored by premium varietals and long-term acreage expansion.

From a financial standpoint, Mission Produce’s model is built around disciplined capital allocation, cash generation and balance sheet strength. Following a multi-year infrastructure investment cycle, capital intensity is moderating, creating room for enhanced free cash flow and strategic flexibility. Although tariff dynamics and cross-border trade policies can influence the flow of produce and short-term pricing, Mission Produce’s diversified sourcing network and global footprint mitigate concentrated risks.

In essence, AVO is not merely a commodity distributor; it is a scaled, data-enabled category partner positioned to consolidate share in a growing global avocado industry.

Limoneira’s investment case is rooted in its long-standing position as a diversified agribusiness operator with deep exposure to lemons and a growing footprint in avocados. The company controls significant citrus acreage in California and Arizona, and maintains a meaningful presence in the U.S. lemon market, positioning itself as a steady supplier to retail, foodservice and export channels.

In avocados, however, Limoneira remains a relatively small player compared to global leaders, with production largely concentrated in domestic orchards and joint ventures rather than commanding a dominant share of the broader avocado industry. Its portfolio also includes valuable real estate development projects, adding a non-operating asset dimension that differentiates it from pure-play produce distributors.

Limoneira emphasizes disciplined cost management, water resource optimization and strategic land monetization to enhance long-term value. Its brand positioning leans on heritage and quality in lemons, targeting mainstream grocery consumers and foodservice buyers seeking a consistent domestic supply. Unlike vertically integrated global avocado marketers, Limoneira’s model is more land-intensive and crop-cycle dependent, limiting its flexibility in rapidly shifting global supply environments. While management highlights operational improvements and balance sheet focus, growth remains tied closely to agricultural yields, commodity pricing and real estate execution.

Tariff dynamics and cross-border trade policies further complicate the outlook, particularly given the reliance on U.S. production and export markets. Although the company benefits from asset ownership and long-term land value appreciation, its comparatively smaller avocado exposure and heavier dependence on citrus cycles may constrain scalability. Over time, limited category leadership and exposure to agricultural volatility could temper its competitive positioning relative to larger, globally diversified peers.

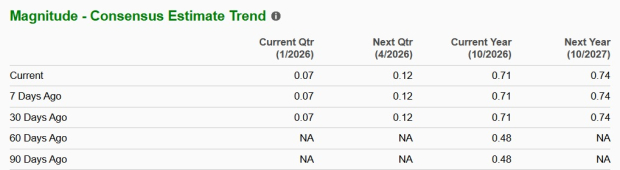

The Zacks Consensus Estimate for Mission Produce’s fiscal 2026 EPS suggests a year-over-year decline of 10.1%, while the estimate for fiscal 2027 indicates growth of 4.2%. AVO’s EPS estimates for both periods have been unchanged in the past 30 days.

LMNR’s estimate for the fiscal 2026 loss per share of 24 cents is slated to improve year over year from the prior year’s reported loss of 79 cents. The estimate for the fiscal 2027 earnings per share of 93 cents suggests a significant improvement from the estimated loss of 24 cents for fiscal 2026. LMNR’s bottom-line estimates for both periods have been unchanged in the past 30 days.

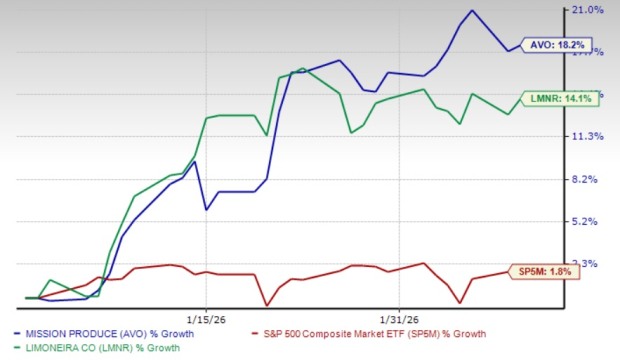

In the past six months, the AVO stock has recorded a total return of 18.2%. This has noticeably outpaced LMNR’s 14.1% rise and the benchmark S&P 500’s return of 1.8%

From a valuation perspective, Mission Produce trades at a forward price-to-sales (P/S) multiple of 0.77X, which is below its 5-year median of 0.85X. Moreover, the AVO stock trades below Limoneira’s forward 12-month P/S multiple of 2.05X and a 5-year median of 1.54X.

In the race for fresh produce leadership, Mission Produce clearly pulls ahead. While Limoneira offers stability through citrus operations and real estate assets, AVO’s global avocado dominance, vertically integrated platform and expanding international footprint provide stronger long-term growth drivers. Its robust year-to-date return signals rising investor confidence in its scalable, category-leading model.

Despite this momentum, AVO trades below its historical valuation levels and at a discount to LMNR on a forward price-to-sales basis, suggesting that the market has yet to fully price in its earnings potential. Combining growth prospects with an attractive valuation, Mission Produce appears best positioned to win this battle. LMNR currently carries a Zacks Rank #5 (Strong Sell), while AVO has a Zacks Rank #2 (Buy).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Jul-23 | |

| Jul-17 | |

| Jul-10 | |

| Jun-10 | |

| Jun-10 | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 | |

| Jun-08 | |

| Jun-02 | |

| May-28 | |

| May-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite