|

|

|

|

|||||

|

|

|

Amazon.com, Inc. AMZN delivered a mixed fourth-quarter 2025 performance, posting revenues of $213.4 billion, which beat expectations and increased 14% year over year. However, earnings per share of $1.95 narrowly missed the consensus estimate by 1.52%. While the top-line strength was encouraging, the stock fell sharply after management unveiled a staggering $200 billion capital expenditure plan for 2026, marking a steep rise from the $125 billion it spent in 2025. This aggressive spending trajectory has sparked debate among investors about whether the AI-fueled investment spree will reward shareholders or weigh on returns in the near term.

The Zacks Consensus Estimate for AMZN’s 2026 earnings is pegged at $7.72 per share, which has seen a downward revision of 2.2% over the past 60 days. The figure indicates a 7.67% increase from the figure reported in the year-ago quarter.

Amazon.com, Inc. price-consensus-chart | Amazon.com, Inc. Quote

Amazon Web Services (“AWS”) remains the crown jewel of Amazon's portfolio, posting $35.6 billion in fourth-quarter revenues, representing a 24% year-over-year increase that marked the segment's fastest growth in 13 quarters. AWS' order backlog surged 40% year over year to $244 billion, underscoring robust multi-year demand visibility.

The custom silicon strategy is gaining traction, with Trainium and Graviton chips reaching a combined annual revenue run rate exceeding $10 billion, growing at triple-digit percentages. Trainium3 is delivering production workloads, with nearly all supply expected to be committed by mid-2026, while Trainium4 is targeted for 2027. In January 2026, Amazon announced plans to invest up to $50 billion to build purpose-built AI and supercomputing infrastructure for U.S. government agencies, adding 1.3 gigawatts of capacity.

The magnitude of capital deployment is pressuring free cash flow, which declined 71% year over year on a trailing 12-month basis to $11.2 billion, raising legitimate concerns about near-term returns.

For the first quarter of 2026, Amazon guided net sales between $173.5 billion and $178.5 billion, representing 11-15% year-over-year growth. Operating income guidance of $16.5-$21.5 billion incorporates approximately $1 billion in higher year-over-year costs from Amazon Leo, the company's low Earth orbit satellite constellation, as well as investments in quick commerce and sharper international pricing.

The advertising business continues to deliver, with fourth-quarter ad revenues reaching $21.3 billion, up 23% year over year. Amazon also announced 16,000 corporate layoffs in January 2026 to flatten its organizational structure, reduce bureaucracy, and improve efficiency. On the consumer side, Prime delivery speeds reached record levels in 2025, with more than eight billion items arriving same-day or next-day in the United States, a 30%-plus increase from the prior year. Meanwhile, Rufus, the AI-powered shopping assistant, generated nearly $12 billion in incremental annualized sales after being used by more than 300 million customers.

From a valuation standpoint, AMZN stock appears overvalued, trading at a forward 12-month price/earnings ratio of 25.67X, higher than the Zacks Internet - Commerce industry’s 22.23X. Amazon has a Value Score of C.

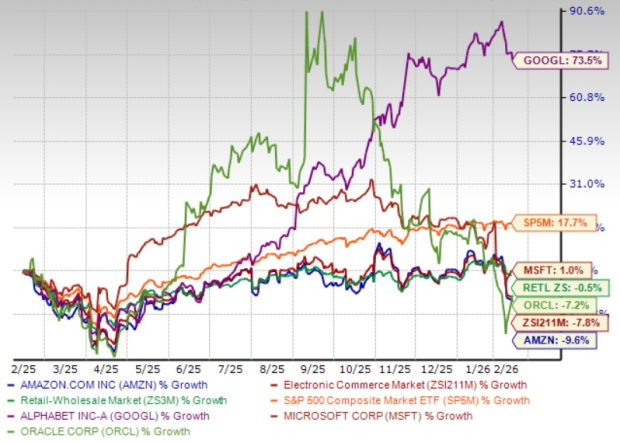

Amazon shares have lost 9.6% over the past year, underperforming the broader Zacks Retail-Wholesale sector and the S&P 500. Amazon’s competitors, Microsoft MSFT and Alphabet GOOGL-owned Google, have returned 1% and 73.5%, respectively, while shares of Oracle ORCL have lost 7.2%.

Alphabet’s Google Cloud posted 48% revenue growth in the fourth quarter, while Microsoft Azure recorded 39% growth, both outpacing AWS on a percentage basis off smaller revenue bases. Oracle continues to expand its cloud infrastructure aggressively through initiatives like the Stargate joint venture. While Amazon maintains overall cloud market leadership, the competitive gap is narrowing. Alphabet’s AI-first strategy, Microsoft’s deep enterprise integration through Copilot, and Oracle’s growing government and enterprise cloud partnerships all pose credible competitive threats that investors should monitor closely.

Amazon's long-term positioning across cloud computing, AI, advertising and e-commerce remains compelling. The company is making bold bets that could define the next decade of growth. However, the $200 billion capex plan introduces meaningful near-term uncertainty, particularly around free cash flow and margin pressure from satellite investments and international expansion. The premium valuation relative to industry peers further limits the margin of safety. For existing shareholders, holding the stock appears prudent, given the strength of AWS' AI-driven momentum and the expanding addressable market. For prospective investors, patience may be warranted, as a pullback or improved clarity on capital returns could present a more attractive entry point later in 2026. Amazon carries a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 |

Dow Jones Futures: Market Triggers Sell Signal; Apple Earnings, Iran News, Fed Meeting In Focus

AMZN MSFT

Investor's Business Daily

|

| Jul-25 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

What to watch next week: Big Tech earnings, the Fed, and Consumer Confidence

GOOGL MSFT

Yahoo Finance Video

|

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite