|

|

|

|

|||||

|

|

|

JPMorgan JPM is the largest U.S. bank, with a deep global footprint and a highly diversified franchise spanning consumer banking, corporate and investment banking, commercial banking, and asset and wealth management. Truist Financial TFC, by contrast, is a leading regional bank with a strong Southeast/Mid-Atlantic presence, pairing selective branch buildouts with a growing emphasis on digital banking and client experience.

Following an impressive 2025 performance, let’s examine how JPM and TFC are positioned to manage shifting interest rate dynamics, loan growth, credit quality and fee-income trends, and which appears better placed in 2026.

JPMorgan’s balance sheet is highly asset-sensitive. Therefore, lower rates are likely to adversely impact the company’s net interest income (NII). Nonetheless, continued loan and deposit growth will likely support the company’s NII, which is projected to grow more than 7% to $103 billion in 2026.

Additionally, the shift toward easier monetary policy supports client activity, deal flow and asset values. Thus, JPMorgan’s non-interest income streams will likely see decent improvement.

Further, JPM continues to invest in brick-and-mortar to strengthen its competitive edge in relationship banking. The company is targeting to expand its affluent banking services and plans to open more than 500 new branches by 2027 to boost cross-selling across mortgages, loans, investments and credit cards. Apart from this, in 2021, the company launched its digital retail bank, Chase, in the U.K. and plans to expand the reach of its digital bank across the European Union (to open a digital bank in Germany by mid-2026).

Moreover, the company has expanded through strategic acquisitions, including a larger stake in Brazil’s C6 Bank, partnerships with Cleareye.ai and Aumni, and the 2023 purchase of First Republic Bank.

Lower rates will likely support JPMorgan's asset quality, as declining rates will ease debt-service burdens and improve borrower solvency. It expects card service NCO rate to be roughly 3.4% “on favorable delinquency trends driven by the continued resilience of the consumer.”

Unlike JPM, Truist is less sensitive to interest rate cycles. Since the divestiture of its insurance subsidiary in 2024, the company has been trying to strengthen its balance sheet through repositioning and making efforts to enhance its non-interest revenue sources.

In 2025, TFC announced a growth plan – opening 100 new branches and renovating more than 300 existing locations in high-growth opportunity cities by 2030 and investing in its business banking ecosystem – to capitalize on growth opportunities in dynamic U.S. markets while strengthening its digital capabilities.

Also, the company is focusing on wealth management and capital markets businesses to drive non-interest income higher. This will also help alleviate Truist’s dependence on spread income to sustain top-line growth as rates come down. The company projects mid to high single-digit growth in non-interest income for this year.

For 2026, TFC anticipates NII to be up in the range of 3-4%, primarily driven by low single-digit loan and deposit growth, fixed-rate asset repricing, improved earning asset mix and lower deposit costs.

Like JPM, the company’s asset quality is expected to benefit as interest rates decline. As such, TFC expects net charge-offs to be relatively stable in 2026. As Truist gets on with its branch expansion plan, upgrade technology and hire personnel to drive commercial banking business, operating expenses will likely remain high. The company expects non-interest expenses to rise 1.25-2.25% this year.

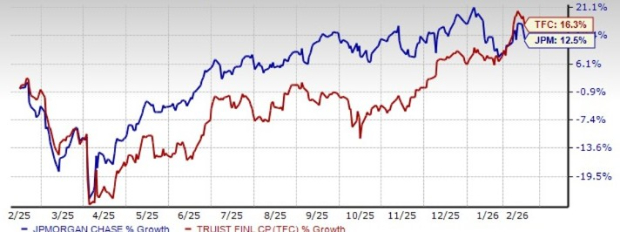

In the past year, shares of JPMorgan have gained 12.5%, while Truist rallied 16.3%.

JPM & TFC 1 Year Price Performance

In terms of investor sentiments, TFC clearly has the edge.

In terms of valuation, JPM is currently trading at a 12-month forward price-to-earnings (P/E) of 14.42X, while the TFC stock is currently trading at a 12-month forward P/E of 11.88X.

P/E F12M

So, JPMorgan is expensive compared to TFC.

After clearing the 2025 stress test, JPM announced a hike in its quarterly dividends, while Truist maintained it at the same level. JPMorgan increased its dividend by 7% to $1.50 per share, while Truist will continue to pay 52 cents per share as a dividend. At present, JPM's dividend yield is 1.93%, which is less than Truist’s 3.85%.

Dividend Yield

JPMorgan’s return on equity (ROE) of 17.16% is above TFC’s 9.03%. This reflects that JPM is more efficiently using shareholder funds to generate profits.

ROE

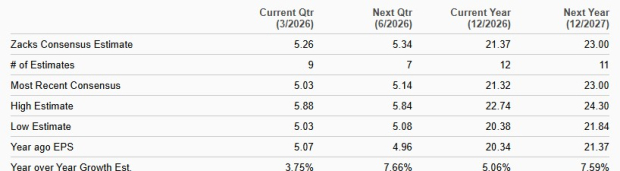

The Zacks Consensus Estimate for JPM’s 2026 and 2027 revenue implies year-over-year growth of 5.1% and 3.1%, respectively. The consensus estimate for earnings indicates a 5.1% and 7.6% rise for 2026 and 2027, respectively.

JPM Earnings Estimate

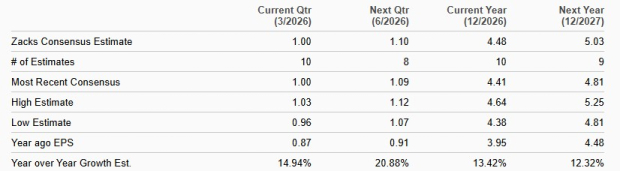

Meanwhile, the Zacks Consensus Estimate for TFC’s 2026 and 2027 revenue suggests year-over-year growth of 4.8% and 4.2%, respectively. The consensus estimate for earnings indicates a 13.4% and 12.3% rise for 2026 and 2027, respectively.

TFC Earnings Estimate

JPMorgan appears better placed than TFC heading into 2026, thanks to the sheer breadth of its earnings engines and its ability to offset rate-driven pressure on NII with stronger loan/deposit growth and rising fee businesses. Even in a lower-rate backdrop, JPM’s NII is projected to climb more than 7%, while easier policy should lift capital markets activity, IB momentum and asset-management fees. Add to that a steady expansion strategy, 500+ branches by 2027, and a growing international digital presence, and JPM’s scale advantage becomes difficult to match.

Truist is making the right moves post-insurance divestiture by repositioning the balance sheet, investing in branches and pushing wealth/capital markets to broaden revenues. Still, its 2026 NII outlook looks more modest, and elevated spending tied to expansion and technology upgrades may constrain operating leverage. Despite trading cheaper and offering a higher yield, JPM’s superior profitability (higher ROE), capital return momentum and diversified growth profile make it the sturdier 2026 setup.

Currently, JPM and TFC carry a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 18 hours | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 |

Four Takeaways From Our Report on the IRS Chief Who Spied on Colleagues at JPMorgan

JPM

The Wall Street Journal

|

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite