|

|

|

|

|||||

|

|

|

Iridium Communications IRDM reported earnings per share (EPS) of 24 cents for the fourth quarter of 2025, beating the Zacks Consensus Estimate by 4.4%. The bottom line, however, compared unfavorably with the prior year quarter's figure of 32 cents.

Iridium reported quarterly total revenue of $212.9 million, flat year over year, missing the consensus estimate by 3%. Service revenue growth largely offset declines in subscriber equipment revenue. This mix shift continues to enhance visibility and margin stability, as service revenue is primarily recurring and subscription-driven. For the full year, revenue grew 5% to $871.7 million, fueled by rising IoT demand and deeper integration into mission-critical applications.

Total Service revenues rose 3% year over year to $158.9 million. The growth in recurring revenues, led by higher subscriber engagement, drove the performance. Service revenues contributed 75% to total revenues in the fourth quarter. Our estimate for the metric was $157.8 million.

Commercial service revenue grew 3% year over year to $131.2 million, accounting for 62% of total revenue in the quarter. Growth was driven by a 4% increase in voice and data revenue, supported by summer price hikes, and an 11% rise in commercial IoT revenue. In 2025, Iridium added new partners and certified more than 30 IoT products. These new relationships and applications are expected to expand its sales pipeline and extend its satellite technology to more industries and customers in the coming years. This segment remains the structural growth pillar of the business.

Iridium Communications Inc price-consensus-eps-surprise-chart | Iridium Communications Inc Quote

Hosted payload and other data services revenue fell 13% year over year to $13.4 million in the quarter, mainly due to a delay in a PNT deployment by an existing customer. Excluding this delay, demand for Iridium’s assured PNT services remains strong, and the company continues to target $100 million in annual service revenue from this business by the end of the decade. Government service revenue rose 3% to $27.6 million, driven by a contractual rate increase under the Enhanced Mobile Satellite Services (EMSS) contract with the U.S. Space Force. Our estimate for total commercial service and government service revenues was pegged at $137.5 million and $26.3 million, respectively.

Subscriber Equipment sales declined 21% to $17 million. Although down year over year, it aligns with Iridium’s outlook for normalized annual equipment sales of $80–$90 million. We projected the figure to be $18.6 million.

Engineering and support revenue inched down 1% year over year at $37.1 million. Engineering revenue rose sharply in 2025 and is expected to grow again in 2026, providing diversification beyond pure subscription revenue.

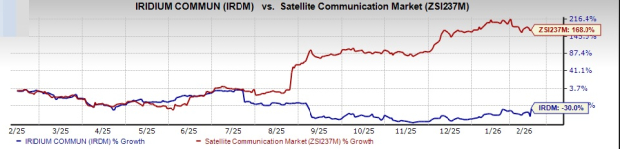

Following the announcements, IRDM’s shares jumped 21.3% in trading and closed the session at $22.39 on Feb. 12. In the past year, shares have declined 30% against the Zacks Satellite and Communication industry's growth of 168%.

Total operating expenses were $157.7 million compared with $160.9 in the prior-year quarter, primarily due to lower research and development costs.

Operational EBITDA (OEBITDA) of $115.3 million was down 2% year over year. OEBITDA fell by a $3 million inventory charge recorded in the fourth quarter.

Operating income came in at $55.3 million compared with $52.1 million in the year-ago quarter.

Iridium ended the fourth quarter with 2,537,000 total billable subscribers, up 3% from 2,460,000 at the prior-year quarter end. The year-over-year rise was backed by strength in commercial IoT. Commercial IoT now represents 83% of commercial subscribers, reinforcing Iridium’s strategy of serving industrial, maritime, aviation, oil & gas, mining and asset-tracking markets.

As of Dec. 31, 2025, total cash and cash equivalents were $96.5 million, with $1.7 billion of net debt. Capital expenditures were $33.5 million in the quarter under review.

Due to the suspension of its share repurchase program as announced on the third-quarter earnings call, Iridium did not buy back any shares in the fourth quarter. In 2025, Iridium bought back about 6.8 million shares for a total of roughly $185 million. As of Dec. 31, 2025, $245.3 million remained available under the current authorization, which runs through 2027.

For 2026, service revenue is expected to be flat to up 2%, reflecting continued IoT growth offset by moderation elsewhere, following 2025 service revenue of $634 million.

Iridium expects 2026 OEBITDA of $480–$490 million compared with $495.3 million reported in 2025. The guidance includes a roughly $17 million hit from paying incentive compensation fully in cash rather than a mix of cash and equity. Excluding this accounting change, 2026 OEBITDA would have been $497–$507 million, indicating no underlying operational deterioration.

Iridium currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 (Strong Buy) Rank stocks here

America Movil, S.A.B. de C.V. AMX reported net income per ADR of 35 cents for fourth-quarter 2025, up from 7 cents in the prior-year quarter. The earnings figure, however, missed the Zacks Consensus Estimate of 43 cents. Net income in the quarter was Mex$19,134 million, or Mex$0.32 per share, compared with Mex$4,074 million, or Mex$0.07 per share, in the year-ago quarter.

Lumen Technologies, Inc. LUMN reported a fourth-quarter 2025 adjusted earnings (excluding special items) of 23 cents per share, which was significantly higher than the Zacks Consensus Estimate of a loss of 21 cents. The company reported adjusted loss per share of 9 cents in the prior-year quarter. Quarterly total revenues were $3.041 billion, down 8.7% year over year and missed the Zacks Consensus Estimate by 1.4%.

BCE Inc. BCE reported fourth-quarter 2025 adjusted EPS of C$0.69 (49 cents), down from C$0.79 in the prior-year quarter. The Zacks Consensus Estimate was pegged at 45 cents. Quarterly total operating revenues dipped 0.3% year over year to C$6.4 billion ($4.6 billion). The consensus estimate was pegged at $4.7 billion. The decline is attributed to a 15% fall in Product revenues, which totaled C$965 million, amid 2.9% growth in Service revenues, which came in at C$5.4 billion.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite