|

|

|

|

|||||

|

|

|

AECOM ACM recently raised full year earnings guidance as it enjoys a record backlog. This Zacks #1 Rank (Strong Buy) is expected to grow earnings by the double digits in fiscal 2026 and 2027.

AECOM is a global infrastructure leader. It solves clients’ complex challenges in water, environment, energy, transportation, and buildings. AECOM partners with public- and private-sector clients to create innovative and resilient solutions throughout the project lifecycle, from advisory, planning, design and engineering to program and construction management.

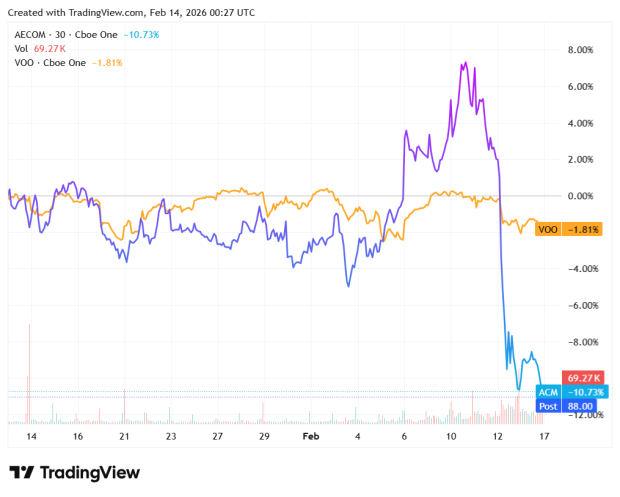

On Feb 9, 2026, AECOM reported its fiscal first quarter 2026 results and missed on the Zacks Consensus for the first time in seven quarters. The company reported $1.29 versus the Zacks Consensus of $1.41.

That was a miss of $0.12.

However, the backlog rose by 9%, to a record highlighted by some of the largest and most iconic projects in the world.

Some of those projects include AECOM’s selection as a preferred bidder on Scottish Water’s new multi-billion-dollar investment program to its selection as Delivery Partner to the Games Independent Infrastructure and Coordination Authority for the Brisbane 2032 Olympic and Paralympic Games.

It has a 1.5x book-to-burn ratio.

The company had outperformance in the design business in the first quarter, a lower than previously expected tax rate, and a record backlog and pipeline across the enterprise. It feels confident in its long-term outlook.

It raised its full year earnings outlook to a range of $5.85 and $6.05, compared to its prior guidance of $5.65 to $5.85.

This guidance was above the Zacks Consensus. As a result, the analysts have raised their earnings estimates.

Three estimates were raised in the last week, which has bumped the Zacks Consensus up to $5.98 from $5.65. That’s earnings growth of 13.7% as the company made just $5.26 last year.

Two estimates were also revised higher for fiscal 2027 in the last week as well. The 2027 Zacks Consensus has jumped to $6.59 from $6.18. That’s another 10.2% earnings growth.

Here’s what it looks like on the price and consensus chart.

AECOM also completed the review of strategic alternatives for its Construction Management business and has concluded that it will continue to own and operate the business.

It has a strong backlog and pipeline and has worked on important projects in its markets.

AECOM shares have fallen in the last six months.

The stock is cheap. It trades with a forward price-to-earnings (P/E) ratio of 14.8. A P/E of 15 or under usually indicates a stock is a value.

AECOM also has a price-to-sales (P/S) ratio of 0.7. A P/S ratio under 1.0 usually indicates a company is undervalued.

The company is shareholder friendly. In the fiscal first quarter, it returned more than $340 million to shareholders through repurchases and dividends in the quarter. The dividend is yielding 1.4%.

After the first quarter ended, the Board of Directors approved an increase in the share repurchase authorization to $1 billion.

For those investors looking for an infrastructure company with growing earnings that is also a value, they might want to keep AECOM on their short list.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-31 | |

| Jul-27 | |

| Jul-20 | |

| Jul-13 | |

| Jul-07 | |

| Jul-06 | |

| Jun-29 | |

| Jun-22 | |

| Jun-08 | |

| Jun-03 | |

| May-21 | |

| May-20 | |

| May-13 | |

| May-12 | |

| May-12 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite