|

|

|

|

|||||

|

|

|

Coconut water company The Vita Coco Company (NASDAQ:COCO) beat Wall Street’s revenue expectations in Q4 CY2025, but sales were flat year on year at $127.8 million. The company’s full-year revenue guidance of $690 million at the midpoint came in 0.9% above analysts’ estimates. Its GAAP profit of $0.09 per share was 29.6% below analysts’ consensus estimates.

Is now the time to buy Vita Coco? Find out by accessing our full research report, it’s free.

Founded in 2004 followed by a 2021 IPO, The Vita Coco Company (NASDAQ:COCO) offers coconut water products that are a natural way to quench thirst.

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $609.8 million in revenue over the past 12 months, Vita Coco is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

As you can see below, Vita Coco grew its sales at a solid 12.5% compounded annual growth rate over the last three years as consumers bought more of its products.

This quarter, Vita Coco’s $127.8 million of revenue was flat year on year but beat Wall Street’s estimates by 6.2%.

Looking ahead, sell-side analysts expect revenue to grow 12% over the next 12 months, similar to its three-year rate. This projection is noteworthy and indicates the market sees success for its products.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

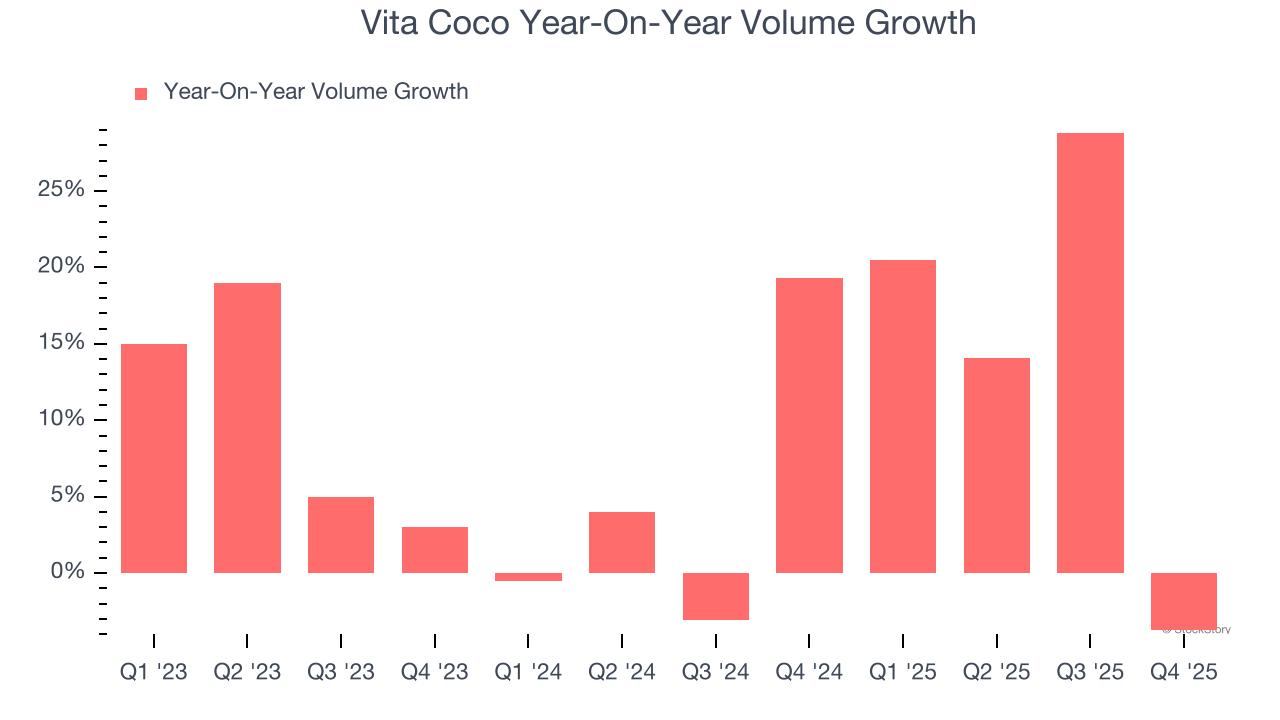

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Vita Coco’s average quarterly volume growth was a robust 9.9% over the last two years. This is good because meaningful volume growth is hard to come by in the stable consumer staples sector.

In Vita Coco’s Q4 2025, sales volumes dropped 3.7% year on year. This result was a reversal from its historical levels. A one quarter hiccup shouldn’t deter you from investing in a business, and we’ll be monitoring the company to see how things progress.

We liked that Vita Coco beat analysts’ revenue and EBITDA expectations this quarter. We were also excited its EBITDA guidance outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock traded up 4.4% to $59.00 immediately after reporting.

Sure, Vita Coco had a solid quarter, but if we look at the bigger picture, is this stock a buy? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-11 | |

| Jul-09 | |

| Jun-18 | |

| Jun-15 | |

| Jun-03 | |

| May-26 | |

| May-05 | |

| May-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite