|

|

|

|

|||||

|

|

|

Cameco CCJ reported fourth-quarter 2025 results on Feb. 13, with adjusted earnings per share rising 38% year over year to 36 cents. Earnings beat the Zacks Consensus Estimate by a margin of 24%.

Let us delve deeper into the company’s fourth-quarter results and long-term prospects before assessing whether to buy, hold or sell the stock.

Cameco reported a 2% decline in uranium production to 6 million pounds in the fourth quarter. Its share of production from Cigar Lake was 2.6 million pounds (up 4% year over year) while output from McArthur River/Key Lake fell 8% to 3.3 million pounds.

The company sold 11.2 million pounds of uranium, 12.8% lower than in the fourth quarter of 2024. Lower volumes, somewhat offset by 13% increase in the Canadian dollar average realized price due to fixed-price contracts, led to a 1% decline in uranium revenues to CAD 1,027 million ($750 million).

In Fuel Services, production increased 6% year over year to 3.8 million kgUs and sales volume rose 6% to 4.4 million kgUs. Segment revenues jumped 18% to CAD 174 million ($127 million), aided by higher sales volumes and 11% increase in average realized prices.

Overall, total revenues were up 1.5% year over year to CAD 1,201 million ($862 million).

Total cost of sales dipped 0.5% to around CAD 928 million ($677 million). Uranium segment’s costs of sales were down 2% due to lower sales volume, offset by an increase of 11% in the average unit cost of sales. In fuel services, the cost of products and services sold rose 13% due to a 7% increase in the unit cost of sales on higher input costs.

Cameco’s total gross profit was up 9% to CAD 273 million ($199 million). Adjusted earnings gained 38% year over year to 36 cents per share in the fourth quarter.

At the end of the fourth quarter, CCJ had C$1.2 billion ($0.88 billion) in cash and cash equivalents, and C$1 billion ($0.73 billion) in long-term debt.

Westinghouse revenues (CCJ’s share) were up 14% to CAD 958 million ($699 million) and adjusted EBITDA rose 30% to CAD 211 million ($154 million).

For 2026, CCJ expects 9.5–10 million pounds of uranium from the Cigar Lake mine and output at McArthur River/Key Lake is predicted at 10.0-11.5 million pounds. This implies a combined production of 19.5-21.5 million pounds compared with the 21 million pounds of uranium in 2025.

Cameco is targeting uranium deliveries at 29–32 million pounds. In 2025, CCJ delivered 33 million pounds of uranium. For 2026, uranium revenues are projected at CAD 2.54–2.73 billion, based on an average realized price of CAD85.00-89.00 per pound. Uranium revenues were around CAD 2.874 billion in 2024.

In the fuel services segment, CCJ guides uranium hexafluoride production between 13 million and 14 million kgU in 2026. Fuel services revenues are projected at CAD 590-630 million for 2026.

This takes Cameco’s total revenue guidance for the year to CAD 3.13-3.37 billion. The company had reported CAD 3.482 billion in revenues in 2025.

Cameco expects its share of adjusted EBITDA from Westinghouse to be $370-$430 million for 2025.

In the uranium segment, CCJ continued to expand its long-term portfolio. After meeting 2025 commitments, the company has long-term obligations to deliver about 230 million pounds of uranium, with an average annual delivery of roughly 28 million pounds over the next five years.

In Fuel Services, strong demand and high UF6 conversion pricing enabled Cameco to secure new long-term conversion contracts, bringing total contracted volumes to about 83 million kgU of UF6, providing solid visibility for future operations.

In fourth-quarter 2025, CCJ, Brookfield and Westinghouse entered into a strategic partnership with the U.S. Government to accelerate the deployment of Westinghouse nuclear reactors in the United States and globally.

This collaboration provides financing support as well as fast-tracking approvals for new Westinghouse nuclear reactors to be built in the United States, with an aggregate investment value of at least $80 billion.

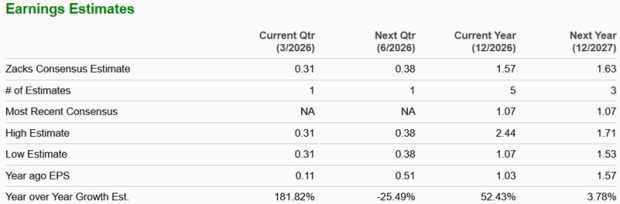

The Zacks Consensus Estimate for Cameco’s earnings for 2026 has moved up over the past 60 days, while the same for 2027 has moved down.

The consensus estimate for Cameco’s earnings for fiscal 2026 indicates year-over-year growth of 52.4%. The same for 2026 implies growth of 3.8%.

In the past year, Cameco shares have gained 142.7% compared with the industry’s 35.7% growth. Cameco has lagged its peer Energy Fuels UUUU, which gained 322.1% in the past year but fared better than Ur-Energy Inc.’s URG 58.9%.

CCJ stock is trading at a forward price-to-sales ratio of 19.54 compared with the industry’s 4.62. CCJ’s Value Score of F suggests that the stock is not so cheap and a stretched valuation at this moment.

Energy Fuels is trading higher at 45.00, while Ur Energy is a cheaper option, trading way lower, at 6.49.

Cameco’s uranium production capacity is among the largest globally, accounting for nearly 15% of worldwide output. The company has secured contracts to sell about 230 million pounds of U3O8 to 39 customers and roughly 83 million kilograms of UF6 conversion to 33 customers, ensuring strong long-term demand visibility.

The company is investing to expand production and capture favorable market conditions, including extending Cigar Lake’s mine life to 2036 and ramping up output at McArthur River and Key Lake toward their licensed annual capacity of 25 million pounds (100% basis).

Rising energy security concerns, geopolitical tensions and the global push for low-carbon energy continue to create structural tailwinds for nuclear power. With low-cost, high-grade assets and a diversified nuclear fuel cycle portfolio, Cameco is well-positioned to benefit from sustained growth in nuclear energy demand.

Cameco’s strong earnings momentum, robust long-term contract portfolio and strategic positioning across the nuclear fuel cycle reinforce its compelling growth outlook. With rising global emphasis on energy security and low-carbon power, sustained demand for nuclear fuel is expected to drive higher volumes and pricing over time. The company’s capacity expansion plans, solid balance sheet and growing contribution from Westinghouse further enhance its earnings visibility.

Despite a premium valuation, these structural tailwinds and improving fundamentals support a bullish long-term investment case. The stock currently sports a Zacks Rank #1 (Strong Buy).

You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite