|

|

|

|

|||||

|

|

|

In a world where data is growing exponentially, fueled by AI, cloud adoption, real-time analytics and digital transformation, storage systems have become critical infrastructure. While legacy HDDs once dominated data centers, the shift toward all-flash storage has transformed the industry. At the forefront of this transition is Pure Storage, Inc. PSTG, whose flash-first portfolio has evolved into a key margin driver, driving higher revenues, better margins, more recurring income and stronger market positioning.

PSTG’s core portfolio includes FlashArray and FlashBlade. FlashArray supports block storage for databases, applications and virtual machines, while FlashBlade is built for unstructured data workloads such as AI and high-performance computing. It has certified its flash platforms for integration with leading AI hardware ecosystems and achieved design wins from hyperscaler engagements, signaling that its flash technology can handle next-gen workloads at scale. AI adoption is boosting demand for flash, which carries higher pricing and more recurring revenue due to its performance and scalability, fueling long-term margin expansion.

Pure’s recent performance shows how Flash products underpin revenue growth and margin expansion. In the fiscal third quarter, it refreshed its core FlashArray portfolio, introducing FlashArray//XL190 R5, FlashArray//X R5 and FlashArray//C R5. The non-GAAP product gross margin was 72.9%, up from 67.4%, driven by higher sales of high-performance FlashArrays, a modest increase in Portworx term-license revenue and increased hyperscaler shipments. By broadening its product portfolio, Pure Storage is strengthening its foothold across industries ranging from financial services and healthcare to AI-driven startups and large-scale cloud providers.

Driven by momentum, PSTG raised its fiscal 2026 outlook, projecting revenue of $3.63–$3.64 billion (up 14.5–14.9% year over year) and non-GAAP operating income of $629–$639 million, both above prior estimates. While rising commodity costs and robust demand may tighten global supply chains and extend lead times, the company’s diversified sourcing, multiple manufacturing sites and continuity plans position it well to manage disruptions. Notably, higher component prices tend to lift revenue more than they pressure margins, potentially providing an additional top-line tailwind.

Continued momentum across the all-flash portfolio, with especially strong Keystone adoption and growth in first-party and marketplace cloud storage services, is driving NetApp Inc.’s NTAP performance. Nearly 46% of systems in the installed base under active support contracts are now all-flash. It expects the new AFF A-series, along with its C-series and ASA products, to capture further share in the all-flash market. Apart from the demand for flash and block, the increasing demand for NetApp’s cloud storage and AI solutions bodes well. For the third quarter, it expects non-GAAP gross margin to be 72.3% to 73.3%, and non-GAAP operating margin to be 30.5% to 31.5%.

Sandisk SNDK is focused on bringing advanced storage technologies and broad flash storage products for AI workloads in data centers, edge devices and consumers. SanDisk delivered strong gains in both fiscal second-quarter revenue and profitability, fueled by AI-driven demand across data center, edge and consumer segments. Management signaled a structurally higher margin and return outlook for the NAND business, backed by disciplined capacity expansion, long-term supply agreements and ongoing innovation. For the fiscal third quarter, Sandisk expects revenues between $4.4 billion and $4.8 billion. Its upbeat guidance reflects confidence in durable demand and reinforces the company’s strategic role as NAND becomes a core building block of global AI infrastructure.

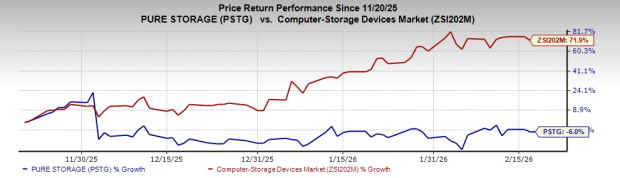

Shares of PSTG have lost 6% in the past three months against Zacks Computer-Storage Devices industry’s growth of 71.9%.

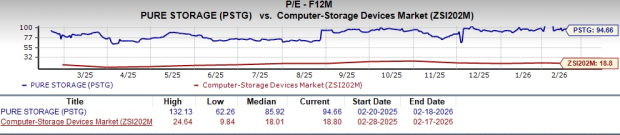

PSTG stock is not cheap, as its Value Style Score of F suggests a stretched valuation at this moment. In terms of forward price/earnings, PSTG’s shares are trading at 94.66X, way higher than the industry’s 18.8X.

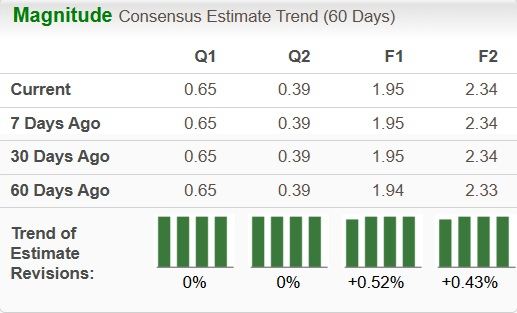

The Zacks Consensus Estimate for PSTG’s earnings for fiscal 2026 has been revised upward marginally over the past 60 days.

PSTG currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 34 min | |

| 1 hour | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 5 hours | |

| 7 hours | |

| 8 hours | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 |

AMD vs. Sandisk: Which company will get some post-earnings market love?

SNDK +6.03%

Yahoo Finance Video

|

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite