|

|

|

|

|||||

|

|

|

Vale S.A. VALE reported fourth-quarter and full-year 2025 results on Feb. 12, posting a 9% increase in revenues and a 70% jump in earnings. While the top-line figure surpassed the Zacks Consensus Estimate, earnings fell short.

Over the past year, Vale shares have gained 57.7%, outperforming the industry’s 56.2% growth, the broader Zacks Basic Materials sector’s 40.5% gain and the S&P 500’s 14.3% rise. The stock has also outpaced peers such as Rio Tinto RIO, BHP Group BHP and Fortescue Ltd FSUGY, which have gained 53.9%, 43% and 22.4% respectively.

Let us delve deeper into the company’s fourth-quarter results and long-term prospects before assessing whether to buy, hold or sell the stock.

Vale’s net operating revenues were up 9.2% year over year to around $11 billion. Iron Solutions segment’s revenues rose 3% year over year to $8.4 billion, driven by a 5% increase in sales volumes and 3% higher iron ore fines realized prices.

The Base Metals segment’s net operating revenues surged 36% year over year to $2.69 billion. Copper net revenues gained 62% to $1.57 billion, aided by 9% higher volumes and a 20% rise in average realized prices for copper. Nickel revenues were up 24% year over year to $1.32 billion, attributed to a 5% increase in sales volume and higher byproduct prices that offset the 7% decline in average realized prices.

Vale’s pro-forma adjusted EBITDA (including associates and joint ventures and excluding expenses related to Brumadinho) was up 17% year over year to $4.8 billion on stronger copper and by-products reference prices as well as higher sales volumes of iron ore and copper. Proforma EBITDA margin was 43.7% in the fourth quarter compared with 40.7% in the year-ago quarter. Adjusted earnings per share surged 70% to 34 cents.

Vale’s iron ore production for 2025 was around 336 Mt, higher than its original guidance of 325-335 Mt. Copper output was around 382.4 kt in 2025, also above the guided 340-370 kt. Nickel output was reported at 177.2 kt compared with the company’s original target of 160-175 kt. Iron ore and copper output reached the highest levels since 2018, and nickel production was the strongest since 2022.

The company has budgeted capital expenditure for the Iron Ore Solutions Business at $4 billion in 2026 and $3.9 billion from 2027 onward. It plans to increase its iron ore production capacity to 335-345 Mt in 2026 and 360 Mt by 2030.

The Vargem Grande 1 (VGR1) project and the Capanema Maximization project are expected to play a key role in attaining these targets, each expected to add about 15 Mtpy of capacity. Additional initiatives, including Compact Crushing at S11D and Serra Sul, are also set to boost capacity from the second half of 2026.

Vale is also investing heavily in the base metals business to benefit from the global energy transition. It expects to invest $1.6 billion in 2026 and about $2 billion annually from 2027.

In 2026, Vale's copper production is expected to be between 350 kt and 380 kt, and reach 420-500 kt as of 2030 and 700 kt by 2035. With these projections, the company promises a 7% CAGR over 2024-2035 compared with the 4% average for peers.

The Bacaba project will extend the life of the Sossego Mining Complex, contributing an average annual copper output of 50 ktpy over an eight-year mine life. Other projects, such as Salobo Coarse Particle Flotation (CPF), Alemão and Cristalino, will increase Vale’s copper production capacity.

Vale recently signed an agreement with Glencore Canada (Glencore) to jointly evaluate a potential brownfield copper development project at their adjacent properties in the Sudbury Basin, with an expected start-up in 2030.

For 2026, Vale expects its nickel production to be between 175 kt and 200 kt, reflecting replenishment projects in Canada, exposure to Pomalaa and Morowali, and the start-up of the second furnace at Onça Puma. For 2030, nickel production is anticipated at 210-250 kt, with input from projects such as Thompson Ultramafics, Sorowako HPAL, partnership projects and offtake.

Vale continues to focus on cost control, with fixed costs reduced to $5.8 billion in 2025 from $6.3 billion a few years ago, and a further decline to $5.7 billion is targeted for 2026. It has managed to lower all-in costs by 3% in its iron business, 77% in the copper business and 27% in the nickel business in 2025, marking the second consecutive year of cost reduction.

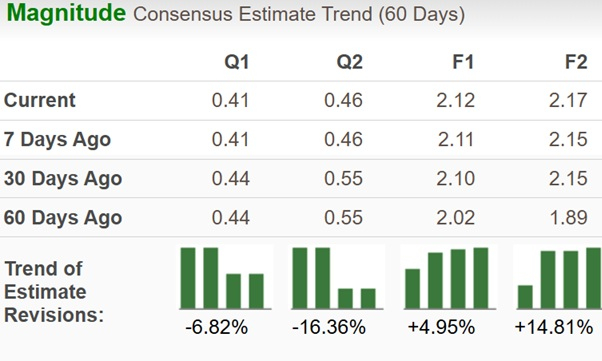

The Zacks Consensus Estimate for Vale’s earnings for both fiscal 2026 and fiscal 2027 has moved up over the past 60 days. This is shown in the chart below.

The earnings estimates for fiscal 2026 indicate year-over-year growth of 16.5%. Earnings estimates for fiscal 2027 imply year-over-year growth of 2.5%.

The company’s current dividend yield of 5.52% is higher than the sector’s 1.70% and the S&P 500’s 1.09%.

VALE’s return on equity, a profitability measure of how prudently it is utilizing its shareholders’ funds, is 20.16%, higher than the sector’s average of 11.55%.

The company is trading at a forward 12-month P/E ratio of 7.52X, at a slight premium to the industry’s 7.50X. The stock is cheaper than Rio Tinto, Fortescue and BHP Group, which are trading at 12.21X, 14.37X and 15.84X, respectively.

Recent operational setbacks include pit overflows at the Fábrica and Viga mines in January, leading to temporary suspensions. Vale recently announced that three requests for asset freezes, filed on a preliminary basis and totaling R$ 2.846 billion, have been denied by the respective competent courts. Only one decision remains pending, related to an asset freeze request in the amount of R$ 200 million. The company’s guidance, however, remains unchanged.

Iron ore prices have fallen below $100 per ton, declining 6.38% over the past month as demand in China softened ahead of the Lunar New Year. At the same time, increasing output from Australia and Brazil, along with anticipated seaborne supply from new projects like Simandou, has added to supply-side pressure.

Weak iron ore prices may weigh on near-term performance, but Vale’s strong production profile, robust project pipeline, expanding base metals exposure and disciplined cost structure support its long-term outlook. Investors already holding the stock may consider staying invested to benefit from its growth projects, improving earnings trajectory and attractive dividend, while new investors may wait for clearer signs of stabilization in iron ore prices before building positions. Vale currently carries a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite