|

|

|

|

|||||

|

|

|

STAAR Surgical STAA recently announced that the FDA has approved an expanded age indication for its EVO/EVO+ Visian Implantable Collamer Lenses (EVO ICL), extending eligibility in the United States to patients aged 21 to 60 years. Previously, the EVO ICL was approved for patients aged 21 to 45 years.

The approval follows the publication of three-year FDA clinical trial data involving 629 eyes, which demonstrated a robust safety profile. Reported outcomes included a safety index of 1.25 at three years, with no cases of pupillary block or pigment dispersion, but a low anterior subcapsular cataract incidence of 0.16%.

An AECOS analysis spanning 19 United States refractive practices reported that EVO ICL was used in over 70% of procedures for patients with -8.0 diopters and above. This suggests a growing preference among experienced surgeons for lens-based correction in high myopia.

Management noted that the consistent preference among surgeons for lens-based correction in high myopia signals a significant shift in treatment paradigms. Coupled with supportive long-term FDA safety data and the recent age-indication expansion, EVO ICL is viewed as playing a central role in shaping the future treatment pathway across a broad spectrum of myopia.

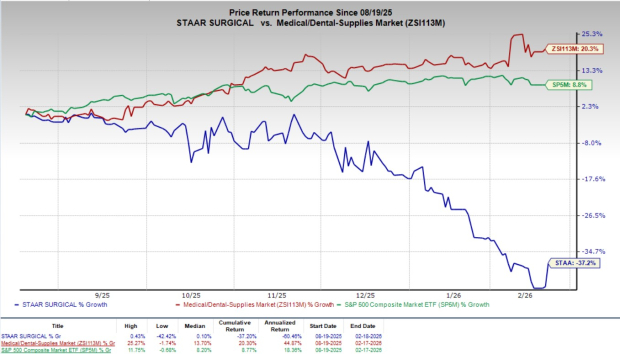

Shares of STAA have gained 8.4% since the announcement on Tuesday. Over the past six months, shares of the company have lost 37.2% against the industry’s 20.3% growth and the S&P 500’s 8.8% rise.

In the long run, STAAR Surgical stands to benefit from the FDA approval for the expanded age indication for EVO ICL due to declining LASIK demand and growing patient interest in lens-based alternatives. The approval, backed by strong long-term safety data and favorable real-world adoption trends, should support higher procedure volumes and strengthen surgeon confidence. Overall, the expansion of age indication positions EVO ICL to capture a significant share in the refractive market as well as reinforce STAA’s growth outlook and competitive positioning in vision correction solutions.

STAA currently has a market capitalization of $805.82 million.

The expanded approval comes against a backdrop of shifting dynamics in the U.S. refractive market. Laser-based procedures involving corneal tissue removal have fallen to multi-decade lows, declining nearly 40% over the past three years, while EVO ICL volumes in the United States continue to rise. Recent patient survey data show that 53% of U.S. vision correction consumers are now considering LASIK alternatives, highlighting a prominent change in patient preferences.

Management estimates that 24 million myopic adults in the United States, including 8 million aged 46-60, could be candidates for EVO ICL. In the international markets, EVO lenses have long been used in patients aged 21-60, with the 46-60 age segment representing about 6% of the total EVO ICL patient base in markets approved up to age 60. The platform’s safety and efficacy are supported by extensive clinical experience and more than 100 peer-reviewed studies.

The EVO lens is implanted through a quick, minimally invasive procedure while preserving corneal tissue and the eye’s natural crystalline lens. This procedure offers a reversible, lens-based vision correction option that maintains flexibility for future treatments. For many patients, this supports a longer-term vision care strategy by delivering immediate visual improvement while allowing surgeons to adjust future treatments as vision needs change. In the United States, EVO Visian ICL is approved for phakic patients aged 21-60 for the correction or reduction of myopia and myopic astigmatism.

Going by the data provided by Precedence Research, the intraocular lens market is valued at $5.34 billion in 2026 and is expected to witness a CAGR of 4.72% through 2035.

Factors like the rising prevalence of eye disorders and aging population, growing patient awareness and acceptance of vision correction options, technological advances in premium IOLs and strong strategic investments and global expansion are boosting the market’s growth.

STAAR Surgical recently announced that its board of directors has appointed Warren Foust (President and COO) and Deborah Andrews (CFO) as interim co-CEOs, effective Feb. 1, 2026. The two executives will jointly oversee day-to-day operations alongside the existing leadership team, with the board oversight during the transition period. Chairman Neal C. Bradsher noted the board’s confidence in their leadership to maintain business continuity while a formal search for a permanent CEO is underway.

STAAR Surgical Company price | STAAR Surgical Company Quote

Currently, STAAR Surgical has a Zacks Rank #3 (Hold).

Some better-ranked stocks from the broader medical space are Intuitive Surgical ISRG, Cardinal Health CAH and McKesson Corporation MCK.

Intuitive Surgical, sporting a Zacks Rank #1 (Strong Buy) at present, reported fourth-quarter 2025 adjusted earnings per share (EPS) of $2.53, beating the Zacks Consensus Estimate by 12.4%. Revenues of $2.87 billion surpassed the Zacks Consensus Estimate by 4.7%. You can see the complete list of today’s Zacks #1 Rank stocks here.

ISRG has an estimated long-term earnings growth rate of 15.7% compared with the industry’s 13% rise. The company beat earnings estimates in the trailing four quarters, the average surprise being 13.2%.

Cardinal Health, currently sporting a Zacks Rank #1, reported a second-quarter fiscal 2026 adjusted EPS of $2.63, which surpassed the Zacks Consensus Estimate by 10%. Revenues of $65.6 billion beat the Zacks Consensus Estimate by 0.9%.

CAH has an estimated long-term earnings growth rate of 15% compared with the industry’s 9.8% rise. The company beat earnings estimates in the trailing four quarters, the average surprise being 9.3%.

McKesson, currently carrying a Zacks Rank #2 (Buy), reported a third-quarter fiscal 2026 adjusted EPS of $9.34, which beat the Zacks Consensus Estimate by 0.3%. Revenues of $106.2 billion beat the Zacks Consensus Estimate by 0.5%.

MCK has an estimated long-term earnings growth rate of 15.9% compared with the industry’s 9.8% rise. The company beat earnings estimates in the trailing four quarters, the average surprise being 3.6%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 10 hours | |

| 10 hours | |

| 17 hours | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 |

Cardinal Health makes acquisition duo worth $360m for home care business advance

CAH

Medical Device Network

|

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite