|

|

|

|

|||||

|

|

|

Barrick Mining Corporation B and Kinross Gold Corporation KGC are two prominent players in the gold mining space with global operations. While gold prices have fallen from their January 2026 highs, they remain favorable. Against this backdrop, comparing these two major gold producers is particularly relevant for investors seeking exposure to the precious metals sector.

Heightened geopolitical strains, including the unrest in Iran with the possibility of U.S. intervention, a weaker greenback, fresh tariff threats and renewed concerns over the independence of the Federal Reserve, drove bullion to a record high of nearly $5,600 per ounce in late January. While gold prices have pulled back from that level, partly due to aggressive profit-taking and a rebound in the U.S. dollar, they remain elevated, currently hovering near $5,000 per ounce.

Sustained central-bank purchases, hopes of more interest rate cuts following the softer-than-anticipated inflation data and persistent safe-haven demand tied to prevailing geopolitical tensions due to U.S.-Iran tensions and broader macroeconomic uncertainties are likely to continue to support gold prices.

Let’s dive deep and closely compare the fundamentals of these two Canada-based gold miners to determine which one is a better investment now.

Barrick is well-placed to benefit from the progress in key growth projects, which should significantly contribute to its production. Its major gold and copper growth projects, including Goldrush, the Pueblo Viejo plant expansion and mine life extension, Fourmile, Lumwana Super Pit and Reko Diq, are underway. These projects are advancing on schedule and within budget, laying the groundwork for the next generation of profitable production.

The Goldrush mine is ramping up to the targeted 400,000 ounces of production per annum by 2028. Bordering Goldrush is the 100% Barrick-owned Fourmile, which is yielding grades double those of Goldrush and is anticipated to become another Tier One mine. The project has progressed to a prefeasibility study on the back of a successful drilling program, which shows significant resource growth potential. The Reko Diq copper-gold project in Pakistan is designed to produce 460,000 tons of copper and 520,000 ounces of gold annually in its second development phase. The first production is expected by the end of 2028.

Moreover, the $2-billion Super Pit Expansion Project at its Lumwana mine is progressing steadily, accelerating its shift into a Tier One copper mine. Barrick stated that the Lumwana expansion is the result of a significant turnaround, transforming the mine from an underperforming asset into a vital part of both its global copper portfolio and Zambia’s long-term development strategy. The expansion is expected to produce 240,000 tons of copper annually.

Barrick has a solid liquidity position and generates healthy cash flows, positioning it well to take advantage of attractive development, exploration and acquisition opportunities, drive shareholder value and reduce debt. At the end of fourth-quarter 2025, Barrick’s cash and cash equivalents were around $6.7 billion. It generated strong operating cash flows of roughly $2.7 billion in the fourth quarter, up 13% year over year, while free cash flow rose 9% year over year to around $1.6 billion. For full-year 2025, operating cash flow surged 71% year over year to around $7.7 billion, and free cash flow shot up 194% to $3.9 billion.

Barrick returned $2.4 billion to its shareholders in 2025 through dividends and repurchases. It repurchased shares worth $1.5 billion during 2025, including $500 million in the fourth quarter. The company increased its dividend to 42 cents per share for the fourth quarter of 2025, marking a 140% increase over the third quarter. It also announced a new dividend policy that targets a total payout of 50% of attributable free cash flow on an annualized basis.

Barrick offers a dividend yield of 1.5% at the current stock price. Its payout ratio is 29% (a ratio below 60% is a good indicator that the dividend will be sustainable), with a five-year annualized dividend growth rate of roughly 5.9%.

Barrick, however, is challenged by higher costs, which may weigh on its margins. Its total cash costs per ounce of gold and all-in-sustaining costs (AISC) — a critical cost metric for miners — increased around 15% and 9% year over year, respectively, in the fourth quarter, and rose from the previous quarter as well. AISC of $1,581 increased from the year-ago quarter due to higher total cash costs per ounce. AISC also rose 10% year over year to $1,637 in 2025.

Lower year-over-year production, partly due to the suspension of operations at the Loulo-Gounkoto mine, contributed to the rise in its unit costs. Barrick’s consolidated gold production fell roughly 19% year over year to 871,000 ounces in the fourth quarter, and declined 17% in 2025.

For 2026, Barrick projects AISC in the range of $1,760-$1,950 per ounce, indicating a significant year-over-year increase at the midpoint. Cash costs per ounce are forecast to be $1,330-$1,470, up from $1,199 in 2025. Lower grades mined, higher prices of key consumables and raised gold price assumptions are the factors expected to contribute to increased costs in 2026. The increase also reflects a higher cost base at Loulo-Gounkoto as the company ramps up mining following the return of control in December 2025.

Kinross has a strong production profile and boasts a promising pipeline of exploration and development projects. Its key development projects and exploration programs remain on track. These projects are expected to boost production and cash flow and deliver significant value. The successful execution of these projects will position the company for a new wave of low-cost, long-life production.

KGC, last month, said that it is progressing with the construction of three organic growth projects to expand its U.S. portfolio. This is aimed at extending mine life and cost optimization. The projects are Round Mountain Phase X and Bald Mountain Redbird 2 in Nevada, and the Kettle River–Curlew project in Washington.

Together, these projects are expected to contribute significantly to Kinross’ U.S. production profile and add a strong value proposition with a combined Internal Rate of Return (IRR) of 59% and a combined incremental post-tax Net Present Value (NPV) of $4.3 billion. These projects are expected to contribute 3 million ounces of life-of-mine production to KGC’s portfolio, adding grades and mine lives. Kinross Gold is planning to self-fund three growth projects entirely from operating cash flows, reflecting its disciplined strategy.

Tasiast and Paracatu, the company’s two biggest assets, remain the key contributors to cash flow generation and production. Tasiast is the highest-margin asset within its portfolio, with a consistently strong performance. Paracatu continues to deliver a strong performance, with fourth-quarter production rising 25% year over year on higher grades. La Coipa also saw a strong fourth quarter on increased mill throughput. KGC also completed the commissioning of its Manh Choh project and commenced production during the third quarter of 2024, leading to a substantial increase in higher-grade production at the Fort Knox operation.

KGC has strong liquidity of $3.5 billion and generates substantial cash flows, which allows it to finance its development projects, pay down debt and drive shareholder value. Kinross reactivated its share buyback program in April 2025. It completed a $600 million share repurchase program as of Dec. 31, 2025. KGC generated a record free cash flow of roughly $2.5 billion last year. It returned $752.4 million to its shareholders through dividends and buybacks in 2025, ending the year with about $1 billion in net cash.

In 2025, the company repaid $700 million of debt. With $1.7 billion in available credit (as of Dec. 31, 2025) and no debt maturities until 2033, Kinross is well-positioned to support growth while strengthening its balance sheet and delivering shareholder value.

KGC’s board has approved a 14% increase to its quarterly dividend, amounting to 16 cents per share on an annualized basis. Kinross is targeting to return 40% of its free cash flow through share buybacks and dividends in 2026. KGC offers a dividend yield of 0.4% at the current stock price. It has a payout ratio of 9%.

However, KGC is exposed to higher production costs. It saw fourth-quarter attributable AISC of $1,825 per ounce, marking a 21% increase from the prior-year quarter and a rise from $1,622 in the prior quarter. For full-year 2025, Kinross’ AISC was $1,571, up from $1,388 in 2024. Kinross expects AISC to be $1,730 per ounce (+/-5%) in 2026, indicating a year-over-year increase partly due to inflationary impacts.

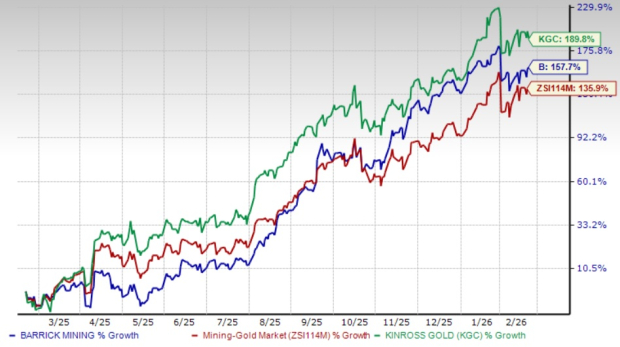

Barrick stock has popped 157.7% over the past year, while KGC stock has rallied 189.8% compared with the Zacks Mining – Gold industry’s increase of 135.9%.

Barrick is currently trading at a forward 12-month earnings multiple of 13.12, lower than its five-year median. This represents a roughly 6% discount when stacked up with the industry average of 13.96X.

Kinross is trading at a modest premium to Barrick. The KGC stock is currently trading at a forward 12-month earnings multiple of 13.46, slightly below the industry.

The Zacks Consensus Estimate for B’s 2026 sales and EPS implies a year-over-year rise of 14.6% and 48.8%, respectively. The EPS estimates for 2026 have been trending higher over the past 60 days.

The consensus estimate for KGC’s 2026 sales and EPS implies year-over-year growth of 9.2% and 40.2%, respectively. The EPS estimates for 2026 have been trending northward over the past 60 days.

Both B and KGC currently have a Zacks Rank #3 (Hold), so picking one stock is not easy. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Both Barrick and Kinross are well-positioned to capitalize on the current favorable gold price environment. Both have a strong pipeline of development projects and solid financial health. They are seeing favorable estimate revisions and delivering incremental returns to their shareholders. Barrick appears to have an edge over Kinross due to its more attractive valuation and higher growth projections. Investors seeking exposure to the gold space might consider Barrick as the more favorable option at this time.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite