|

|

|

|

|||||

|

|

|

Among large-cap U.S. MedTech companies, Boston Scientific BSX and Abbott ABT continue to attract significant investor focus. Abbott’s business model is diversified, having leading businesses and products in diagnostics, medical devices, nutritionals and branded generic medicines. Boston Scientific advanced the practice of less-invasive medicine and has a portfolio of devices and therapies used across cardiovascular, respiratory, digestive, oncological, neurological and urological diseases and conditions.

Innovation sits at the core of both companies’ success. Each one also maintains a disciplined capital allocation strategy, emphasizing strategic M&A to fuel growth. In this faceoff, let’s assess whether ABT or BSX presents the more compelling investment opportunity today.

Boston Scientific’s operational sales grew 14% year over year in the fourth quarter of 2025, surpassing the Zacks Consensus Estimate by 2.6%. In MedSurg, Urology’s full-year results lagged expectations, but management expects the business to return to market growth in 2026 as it rolls out new products and banks on the sacral neuromodulation franchise. The recently announced acquisition of Valencia is also set to expand the pelvic health portfolio.

Neuromodulation performance continues to benefit from the strength of the brain and pain franchises. The Nalu acquisition expands the portfolio into a new adjacency in peripheral nerve pain. During the quarter, Boston Scientific received expanded reimbursement coverage for the Intracept procedure and initiated a full market launch of the Intracept EDGE Stylet, designed to improve the treatment experience.

Among Cardiovascular businesses, Interventional Cardiology Therapies is gaining from the coronary therapies franchise, led by AGENT Drug-Coated Balloon. Boston Scientific completed the first U.S. cases with SEISMIQ IVL for peripheral above-the-knee procedures and plans to expand the indication to include below-the-knee procedures later in the year. Interventional Oncology & Embolization achieved nearly $1 billion in 2025 sales.

Meanwhile, WATCHMAN sales grew 29% year over year in the fourth quarter, supported by continued strong adoption of the concomitant procedures. Electrophysiology (EP) momentum also continued with higher FARAPULSE PFA catheter utilization, supported by ramping adoption of the OPAL HDx mapping system.

Earlier this year, Boston Scientific announced an agreement to acquire Penumbra, offering an opportunity to enter new, fast-growing vascular segments. On a full-year basis, adjusted gross and operating margins expanded by 30 and 100 bps, respectively. Meanwhile, the discontinuation of the ACURATE valve and a transient impact associated with the product removal of certain AXIOS device sizes are expected to weigh on near-term revenue growth.

Abbott’s fourth-quarter 2025 sales rose 4.4% on a reported basis year over year, but fell short of the Zacks Consensus Estimate by 2.8%. In Nutrition, the company is taking steps to transition towards a more volume-driven business by reprioritizing innovation. Abbott has started rolling out pricing and promotional initiatives, and expects to introduce at least eight new products over the course of the next 12 months. Meanwhile, Core Lab Diagnostics continues to see durable demand across global markets.

The Established Pharmaceuticals (EPD) business benefits from exposure to high-demand therapeutic areas aligned with local healthcare needs. Abbott is advancing its biosimilar strategy, a key growth pillar for EPD, by initiating the launch sequence in emerging markets. In Diabetes Care, the FreeStyle Libre continuous glucose monitoring (CGM) system has established a leading global position across both Type 1 and Type 2 diabetes populations. CGM sales exceeded $7.5 billion in 2025, marking the third straight year of more than $1 billion in annual revenues.

In 2025, Abbott achieved several milestones within Medical Devices, including regulatory approvals for the Volt and TactiFlex Duo PFA products, a new indication for the Navitor TAVR valve, and CMS’ national coverage for TriClip and CardioMEMS. Beyond the high-growth segments, the company’s investments in foundational businesses, such as Rhythm Management and Vascular, are also generating impressive returns.

The company also took a major strategic step by announcing the acquisition of Exact Sciences, expanding into cancer diagnostics and adding a new, high-growth business with an attractive pipeline. Despite tariff pressures, Abbott’s adjusted gross and operating margins increased 20 and 150 basis points, respectively, in the fourth quarter, on a year-over-year basis.

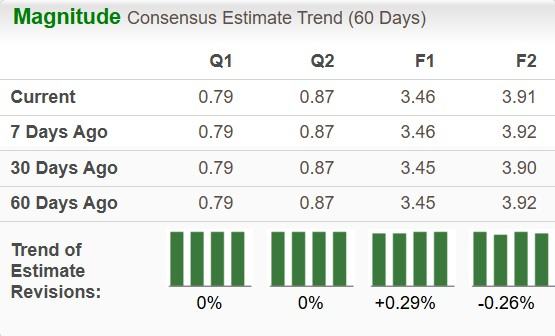

The consensus estimate for Boston Scientific’s 2025 EPS implies a year-over-year increase of 13.1% to $3.46. The estimate has moved up 1 cent in the last 60 days.

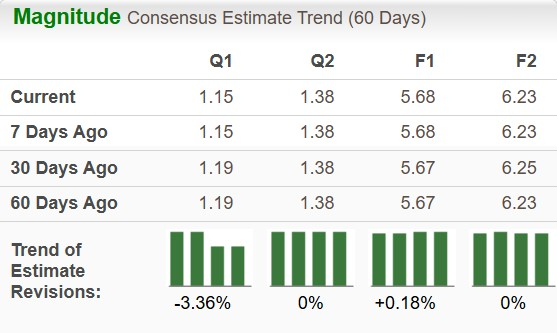

Meanwhile, the consensus mark for Abbott’s 2026 EPS of $5.68 has also risen by 1 cent in the past 60 days. The estimate implies a 10.3% improvement over 2025.

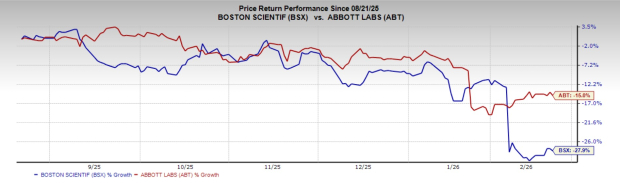

In the last six months, shares of Boston Scientific have fallen 27.9%, while Abbott stock has declined 15%.

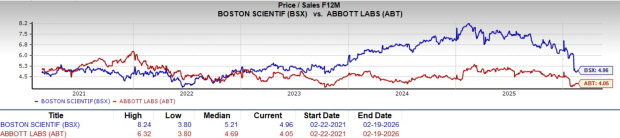

Boston Scientific is trading at a forward, five-year Price/Sales (P/S) of 4.96X, lower than its own median of 5.21X. Abbott trades at a 5-year P/S of 4.05X, also discounted compared to its median of 4.69X.

Both Boston Scientific and Abbott are MedTech heavyweights, taking strategic actions to further long-term growth prospects. Boston Scientific’s latest quarterly performance highlights the strength of its business units, including EP and WATCHMAN, as well as solid operational execution. Near-term revenue impact from the ACURATE discontinuation, along with the AXIOS withdrawal are expected.

Abbott’s 2025 marked several important milestones, with fourth-quarter performance reflecting broad-based growth in EPD, momentum in CGM, as well as robust sales in Electrophysiology. Analysts continue to be bullish on both companies, as seen by their rising earnings estimates. That said, in terms of valuation and recent performance, ABT appears to be the more attractive option at present.

BSX and ABT each carry a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-21 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 |

Abbott Bounds Higher After Hiking 2026 Profit View On Second-Quarter Beat

ABT +10.71%

Investor's Business Daily

|

| Jul-16 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite