|

|

|

|

|||||

|

|

|

Ironwood Pharmaceuticals IRWD and Bausch Health BHC operate in the branded gastrointestinal (GI) drug market, with a focus on treatments for irritable bowel syndrome (IBS) and other therapeutic areas.

While Ironwood is a smaller, more focused company built around its key GI drug and pipeline, Bausch Health is a larger and more diversified drugmaker that markets a wide range of branded, generic, as well as over-the-counter pharmaceutical products.

But which one makes for a better investment pick today? Let's examine the fundamentals of the two stocks to make a prudent choice.

Ironwood’s sole marketed product, Linzess (linaclotide), is approved for the treatment of irritable bowel syndrome with constipation (IBS-C) and functional constipation.

Ironwood markets Linzess in the United States in collaboration with drug giant AbbVie ABBV. The companies equally share Linzess’ brand collaboration profits and losses in the United States.

Ironwood’s top line primarily comprises revenues recorded under its collaborative arrangements with ABBV for the development and commercialization of Linzess in the United States.

Linzess sales picked up momentum in the second half of 2025 on the back of increasing demand. In the first nine months of 2025, Ironwood’s share of net profit from Linzess sales in the United States was $244.1 million. Sales of the drug have been rising owing to strong demand growth in the United States. IRWD is scheduled to report fourth-quarter and full-year 2025 results on Feb. 25 before the opening bell.

Building on this momentum, Ironwood expects a significant improvement in Linzess’ sales in 2026 and subsequently its share of net profit from the sales of the drug in the United States. Ironwood expects total revenues of $450-$475 million in 2026. The revenue outlook for 2026 indicates an increase of 54% year over year at the midpoint compared with 2025.

Besides Linzess, Ironwood has apraglutide in its pipeline, a next-generation GLP-2 analog. It is being developed for treating patients with short bowel syndrome with intestinal failure (SBS-IF) who are dependent on parenteral support. The company recently met with the FDA to align on a confirmatory phase III study design of apraglutide for the treatment of SBS-IF. Ironwood remains on track to initiate a confirmatory study on apraglutide for the given indication in the first half of 2026.

Rising demand for Linzess and upbeat 2026 guidance position Ironwood for sustained long-term growth. However, the company’s heavy reliance on a single product remains a concern. Additionally, any delay or setback in the development of apraglutide could weigh on its near-term growth prospects.

Bausch Health Companies operates across multiple therapeutic areas, while its eye health business is housed under Bausch + Lomb Corporation. Within the Bausch Health segment, revenues are recorded under four divisions: Salix, International, Solta Medical and Diversified Products.

Earlier this week, Bausch Health reported fourth-quarter 2025 results. The company missed earnings estimates but beat the same for revenue.

The company’s revenues are being aided by the Salix business segment, which consists of GI products in the United States. In this segment, Xifaxan is the top revenue generator, which continues to witness strong volume growth.

Xifaxan 550 mg tablets are indicated for the reduction in the risk of overt hepatic encephalopathy recurrence and the treatment of IBS-D in adults.

BHC’s top line is also aided by meaningful contributions from the International and Diversified Products segments. However, revenues from Solta Medical are being impacted by anticipated one-time events related to Solta’s acquisition of Shibo's full-service aesthetics distribution business in China.

Meanwhile, the company’s Bausch + Lomb business segment is also witnessing strong growth across each business — vision care, surgical and pharmaceuticals. The business continues to operate efficiently and deliver organic growth year over year.

Building on this momentum, the company expects a stronger growth rate in the first half of 2026. BHC expects 2026 revenues to be in the range of $10.625-$10.875 billion. Excluding Bausch + Lomb, revenues are now projected to be in the range of $5.250-$5.400 billion. Bausch + Lomb revenues are expected to be in the range of $5.375-$5.475 billion.

BHC also has a deep pipeline and the successful development of the same will expand its portfolio. However, the company recently faced a major setback with the failure of the late-stage RED-C clinical program, which consisted of two phase III studies. The studies evaluated rifaximin solid soluble dispersion for the delay of the first episode of hepatic encephalopathy (HE) in adults with liver cirrhosis who had no prior HE episodes. The studies did not meet the primary endpoint.

The huge levels of debt and generic competition in the target market also remain a concern for the company.

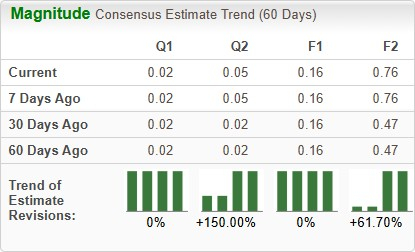

The Zacks Consensus Estimate for Ironwood’s 2026 sales implies a year-over-year increase of around 50.5%, while the same for earnings per share (EPS) suggests a year-over-year increase of 375%. EPS estimates for 2026 (F2) have been trending upward over the past 30 days.

For Bausch Health, the Zacks Consensus Estimate for 2026 sales implies a year-over-year increase of 4.2%, while EPS estimates suggest an upside of 11.8%. EPS estimates for 2026 (F1) have remained stable over the past 30 days.

In the past six months, shares of IRWD have skyrocketed 291.5%, while those of BHC have plunged 21%. The industry has declined 2.7%, as seen in the chart below.

From a valuation standpoint, Ironwood looks more expensive than Bausch Health, going by the price-to-sales (P/S) ratio. IRWD’s shares currently trade at 2.42 times trailing sales value, higher than 0.22 for BHC.

Out of the two stocks discussed above, Ironwood, which currently carries a Zacks Rank #1 (Strong Buy), is clearly the better pick over Bausch Health, which carries a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

While Bausch Health remains financially robust with its diversified operations, the current upward momentum in Ironwood’s business gives it an edge. Ironwood’s approach of strengthening the Linzess franchise while progressing apraglutide, which has blockbuster potential, positions it for long-term growth and profitability.

Despite a premium valuation, Ironwood’s recent price rally and rising earnings estimates also indicate analysts' optimistic outlook for the stock. Though Bausch Health holds a diversified revenue stream, the recent pipeline setbacks and historically high debt levels keep investors worried about sustainable growth in the long run.

Overall, IRWD presents a more visible growth story, making it the better pick over BHC for investors seeking to make meaningful gains in both the short and long term.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite