|

|

|

|

|||||

|

|

|

Willdan Group, Inc. WLDN is scheduled to report its fourth-quarter fiscal 2025 results on Feb. 26, 2026, after market close.

In the last reported quarter, Willdan delivered a record performance, driven by strong execution and broad-based demand. Contract revenue rose 15% year over year to $182 million, while net revenue increased 26% year over year to $95 million (which topped the Zacks Consensus Estimate by 11.5%). Growth included 20% organic expansion, supplemented by acquisitions. Gross profit climbed 30% year over year to $67.1 million, reflecting solid project execution. Adjusted EBITDA surged 53% year over year to $23.1 million, with margin reaching 24% of net revenue. Adjusted EPS rose 65.8% year over year to $1.21 from a year ago and exceeded the consensus mark by 49.4%. The quarter highlighted sustained momentum across energy and infrastructure services.

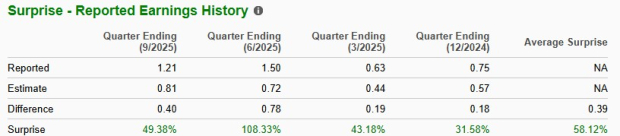

WLDN’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 58.1%, as shown in the chart below.

The Zacks Consensus Estimate for the fourth-quarter earnings per share (EPS) has remained unchanged at 79 cents over the past 30 days. The estimated figure indicates 5.3% growth from the year-ago reported EPS of 75 cents. The consensus mark for revenues is pegged at $87.5 million, suggesting a 39.3% year-over-year decline.

For 2026, Wildan is expected to register a 4.8% increase from a year ago in revenues. Its EPS is expected to witness 9.6% growth from the year ago. Below is what to expect in the fourth quarter of 2025 and for 2026 for WLDN stock.

Fiscal fourth-quarter revenues are expected to have reflected continued strength in Willdan’s Energy segment, which represents roughly 85% of total revenue mix. Robust electricity load growth, driven by data centers and electrification trends, has been a major catalyst for demand in planning, engineering and program management services. Management highlighted accelerating demand for studies assessing electricity load growth impacts, with this upstream advisory work expanding rapidly. Such momentum is likely to have supported the fiscal fourth-quarter activity, particularly in policy, forecasting and data analytics.

Recent contract wins, including large-scale energy and infrastructure upgrades and multiple substation projects, are expected to have contributed meaningfully to the fiscal fourth-quarter revenues as execution progressed. The APG acquisition, focused on power engineering solutions for data centers and renewable developers, has been collaborating effectively and building backlog, positioning it for strong growth. Incremental contributions from acquisitions completed during 2025 are likely to have provided additional support to the quarter’s topline.

Utility programs, which are typically three- to five-year contracts funded by ratepayer fees, continue to provide recurring revenue visibility. Government work, funded largely through user fees and municipal bonds, has also remained healthy, supporting steady demand entering year-end.

However, topline risks for the quarter may have included project timing variability and the inherent lumpiness associated with engineering and infrastructure execution. Additionally, exposure to subcontractor services can create variability in reported contract revenue, depending on project mix.

On the profitability front, management has guided for full-year 2025 adjusted EBITDA of $77-$78 million and net revenues of $360-$365 million. Achieving these targets implies continued margin discipline in the fiscal fourth quarter, supported by favorable project execution, scale benefits and a richer mix of higher-value engineering and data analytics work.

Operating leverage from revenue growth and effective cost control were key drivers of the prior margin expansion, trends likely extending into the fourth quarter. Additionally, the company has targeted a full-year effective tax benefit of approximately 10%, which may have favorably influenced reported earnings in the quarter.

That said, integration costs from recent acquisitions, stock-based compensation and ongoing investments in personnel and capabilities to support anticipated 2026 growth might have tempered margin expansion. Any rise in subcontractor mix or project startup costs may also have exerted pressure on gross margins.

Overall, fourth-quarter 2025 results are likely to reflect continued strong demand in energy and infrastructure markets, balanced against integration and execution-related cost considerations as Willdan scales into a new growth phase.

Our proven model does not conclusively predict an earnings beat for WLDN for the quarter to be reported. That is because a stock needs to have both a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) for this to happen. This is not the case here, as you will see below.

Earnings ESP: WLDN has an Earnings ESP of 0.00%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks Rank: The company currently carries a Zacks Rank #3.

You can see the complete list of today’s Zacks #1 Rank stocks here.

WLDN stock has rallied 19.4% over the past three months, comfortably outperforming the broader Zacks Business - Services industry as well as key peers such as AECOM ACM, ICF International, Inc. ICFI and Tetra Tech, Inc. TTEK. During the same period, AECOM declined 5.8%, lagging WLDN by a wide margin, while ICF International posted a modest 3% gain and Tetra Tech advanced 11%, both trailing WLDN’s stronger momentum.

Compared with AECOM, ICF International and Tetra Tech, WLDN has demonstrated superior near-term price performance, underscoring its relative strength within the engineering and consulting services space.

Price Performance

In terms of the forward 12-month price/earnings (P/E), WLDN stock is currently trading at a premium to its industry.

WLDN’s P/E Ratio (Forward 12-Month) vs. Industry

Willdan has delivered strong operational momentum, driven by robust energy demand, solid execution and acquisition-led expansion. The company has consistently topped earnings estimates and management’s guidance implies continued margin discipline into year-end. However, fourth-quarter consensus estimate points to a sharp year-over-year revenue decline, highlighting project timing variability and contract mix risks. While 2026 forecasts call for modest revenue and EPS growth, the near-term outlook appears balanced. With shares rallying recently and trading at a premium valuation, much of the optimism seems priced in. WLDN appears fairly valued, supporting a Hold stance for now.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite