|

|

|

|

|||||

|

|

|

Centrus Energy LEU and Cameco CCJ are both well-positioned to benefit from the accelerating global shift toward nuclear energy. Centrus Energy supplies nuclear fuel and services for the nuclear power industry, and is pioneering the production of High-Assay, Low-Enriched Uranium (HALEU). Cameco is one of the largest global providers of uranium fuel, with controlling ownership of the world’s largest high-grade reserves and low-cost operations.

For investors keen on this sector, we analyze and compare the fundamentals, growth prospects and risks of LEU and CCJ to determine which stock offers the stronger investment case.

The company, through its Low-Enriched Uranium segment, supplies components of nuclear fuel to commercial customers. This includes the supply of the enrichment component of Low-Enriched Uranium to utilities that operate commercial nuclear power plants. The enrichment component of LEU is measured in Separative Work Units (SWU). Centrus Energy also sells natural uranium hexafluoride.

The Technical Solutions segment provides advanced uranium enrichment services to the nuclear industry and the U.S. government, as well as advanced manufacturing and other technical services to government and private sector customers.

In fourth-quarter 2025, Centrus Energy reported total revenues of $146 million, down 4% year over year. Revenues for the Low-Enriched Uranium segment rose 2% year over year to $124.4 million. This was mainly led by SWU revenues, which surged 128% to $111 million. However, uranium revenues plunged 82% to $13.4 million in the quarter due to a substantial one-time uranium sale in the fourth quarter of 2024. The Technical Solutions’ segment revenues declined 27% year over year to $21.8 million in the quarter.

Total cost of sales rose 24%, resulting in a 43% year-over-year slump in gross profit to $35 million. Operating income fell 72% to $12.8 million, and operating margin contracted sharply to 9% from 30% a year earlier. LEU reported adjusted earnings per share of 79 cents, which marked a 75% year-over-year plunge. A shipment from Russia that was due in the fourth quarter was delayed and pushed out to the first quarter of 2026. This also weighed on margins and net income in the quarter.

Centrus Energy ended 2025 with a $3.8 billion revenue backlog, which includes long-term sales contracts with major utilities through 2040 and a cash balance of $2 billion. It plans capital deployment of $350-$500 million in 2026 to support industrial buildout tied to its centrifuge manufacturing expansion.

In September 2025, the company announced ambitious plans to significantly expand its uranium enrichment plant in Piketon, OH, to boost the production of Low-Enriched Uranium and High-Assay, Low-Enriched Uranium (HALEU). In December, it began design work on a 150,000 square foot training, operations & maintenance facility at the site. It also began domestic centrifuge manufacturing to support commercial LEU enrichment activities at the facility, reinforcing its first-mover advantage in U.S.-owned uranium enrichment.

The company aims to leverage this multi-billion-dollar expansion to address more than $2.3 billion in contingent LEU sales contracts with both domestic and international customers. It is targeting 12 metric tons of HALEU production per year sometime after 2030, with at least some HALEU production by the end of the decade.

Centrus Energy is the only licensed producer of HALEU in the Western world. HALEU demand is expected to surge to power existing reactors and a new generation of advanced reactors. HALEU opportunity is estimated at $8 billion per year by 2035, which provides a strategic advantage to the company.

Cameco's tier-one mining and milling operations have the licensed capacity to produce more than 30 million pounds (its share) of uranium concentrates annually. It holds some of the world's most promising uranium projects and continues to invest in ongoing exploration activities. Cameco accounted for 15% of global uranium production in 2025.

CCJ is also a leading supplier of uranium refining, conversion and fuel manufacturing services. Its ownership stakes in Westinghouse and Global Laser Enrichment (GLE) further strengthen opportunities across the nuclear fuel cycle.

Cameco reported a 2% decline in uranium production to 6 million pounds in the fourth quarter of 2025. Its share of production from Cigar Lake was 2.6 million pounds (up 4% year over year) while output from McArthur River/Key Lake fell 8% to 3.3 million pounds. The company sold 11.2 million pounds of uranium, 12.8% lower than in the fourth quarter of 2024.

Lower volumes, somewhat offset by 13% increase in the Canadian dollar average realized price due to fixed-price contracts, led to a 1% decline in uranium revenues to CAD 1,027 million ($750 million). In Fuel Services, production increased 6% year over year to 3.8 million kgUs and sales volume rose 6% to 4.4 million kgUs. Segment revenues jumped 18% to CAD 174 million ($127 million), aided by higher sales volumes and 11% increase in average realized prices. Overall, total revenues were up 1.5% year over year to CAD 1,201 million ($862 million).

Total cost of sales dipped 0.5% to around CAD 928 million ($677 million). Cameco’s total gross profit was up 9% to CAD 273 million ($199 million). Adjusted earnings gained 38% year over year to 36 cents per share in the fourth quarter. At the end of the fourth quarter, CCJ had C$1.2 billion ($0.88 billion) in cash and cash equivalents, and C$1 billion ($0.73 billion) in long-term debt.

For 2026, CCJ expects 9.5–10 million pounds of uranium from the Cigar Lake mine and output at McArthur River/Key Lake is predicted at 10.0-11.5 million pounds. This implies a combined production of 19.5-21.5 million pounds compared with the 21 million pounds of uranium in 2025. Cameco is targeting uranium deliveries at 29–32 million pounds. In 2025, CCJ delivered 33 million pounds of uranium.

For 2026, uranium revenues are projected at CAD 2.54–2.73 billion, based on an average realized price of CAD 85.00-89.00 per pound. Uranium revenues were around CAD 2.874 billion in 2025. In the fuel services segment, CCJ guides uranium hexafluoride production between 13 million and 14 million kgU in 2026. Fuel services revenues are projected at CAD 590-630 million for 2026. This takes Cameco’s total revenue guidance for the year to CAD 3.13-3.37 billion. The company had reported CAD 3.482 billion in revenues in 2025. Cameco expects its share of adjusted EBITDA from Westinghouse to be $370-$430 million for 2025.

The company has secured contracts to sell about 230 million pounds of uranium to 39 customers and roughly 83 million kilograms of UF6 conversion to 33 customers, ensuring strong long-term demand visibility. Cameco is investing to expand production and capture favorable market conditions, including extending Cigar Lake’s mine life to 2036 and ramping up output at McArthur River and Key Lake toward their licensed annual capacity of 25 million pounds (100% basis).

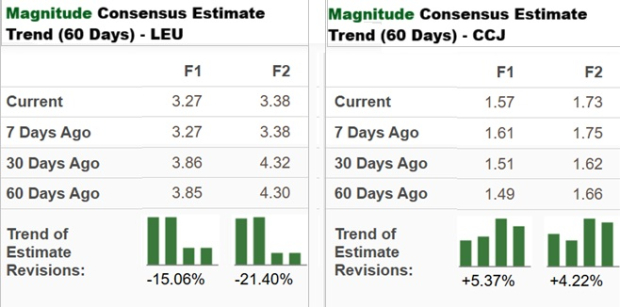

The Zacks Consensus Estimate for Centrus Energy’s 2028 revenues is $457.76 million, implying 2% growth from the year-ago quarter’s actual. The consensus mark for 2026 earnings is pegged at $3.27 per share, which indicates a year-over-year decline of 16%.

The consensus estimate for Centrus Energy’s 2026 revenues of $490.5 million indicates year-over-year growth of 7%. The estimate for earnings is pinned at $3.38 per share, indicating a year-over-year growth of 3.5%.

The Zacks Consensus Estimate for Cameco’s fiscal 2026 revenues is $2.5 billion, implying a 0.5% uptick from the prior year. The estimate for earnings is $1.57 per share, indicating 52% year-over-year growth.

The consensus estimate for Cameco’s 2028 revenues is $2.88 billion, which indicates year-over-year growth of 15%. The consensus mark from earnings per share is $1.73, projecting 10% year-over-year growth.

In the past 60 days, both the earnings estimates for Centrus Energy for 2026 and 2027 have moved down. Meanwhile, Cameco has experienced upward revisions, as shown in the chart below.

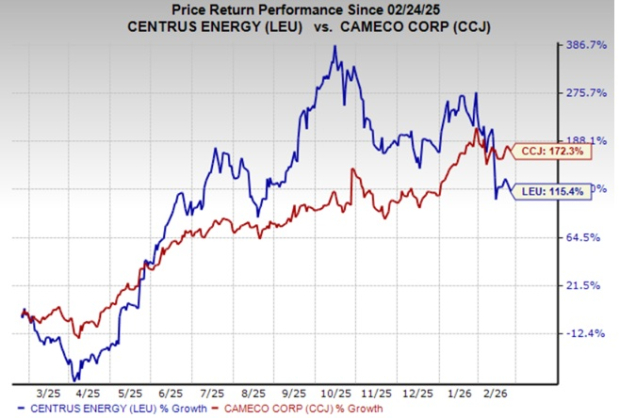

LEU shares have gained 115.4% in the past year, while CCJ shares have gained 172.3%.

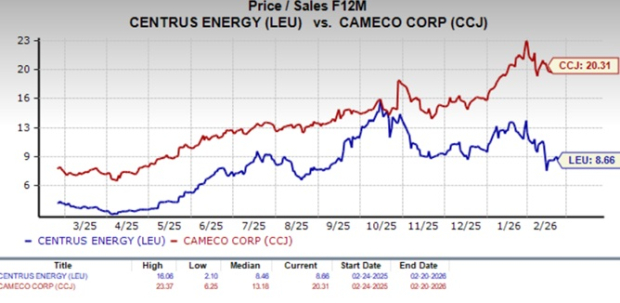

Centrus Energy is trading at a forward price-to-sales multiple of 8.66X. Cameco is trading higher, at a forward price-to-sales multiple of 20.31X.

Both Centrus Energy and Cameco are poised to thrive as nuclear energy gains global traction. Cameco offers scale, diversification and steady earnings visibility through its integrated fuel cycle and Westinghouse investment. Centrus Energy is uniquely positioned to drive the next phase of nuclear innovation through HALEU production.

Both stocks currently have a Zacks Rank #3 (Hold) each, which makes choosing one a difficult task. From a price performance standpoint, earnings visibility and upward estimate momentum, Cameco is the more appealing option at the moment, albeit at a premium valuation.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-29 | |

| Jul-28 | |

| Jul-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite