|

|

|

|

|||||

|

|

|

In an earnings lineup that includes Q4 results from Nvidia NVDA, Dillard’s DDS will also be a stock to watch this week.

Dillard's unique business model, in which it owns most of its retail department stores rather than leasing them, has placed the company in a league of its own as it relates to profitability.

Instead of chasing rapid reinvention, Dillard’s has doubled down on fundamentals — tight inventory control, disciplined operations, and a strong regional footprint — allowing it to thrive while peers like Macy’s M, Kohl’s KSS, and Nordstrom have often stumbled.

Keeping this in mind, Dillard’s stock looks like a top buy-the-dip target ahead of its Q4 report on Tuesday, February 24.

In the last five years, Dillard’s stock has produced market-leading gains of nearly 700%, blowing away the benchmark S&P 500’s 80% and its Zacks Retail-Regional Department Stores Industry’s 51%.

DDS is up a very respectable 30% in the last year, but is 15% from a 52-week and all-time high of $741 a share, which it hit in early December.

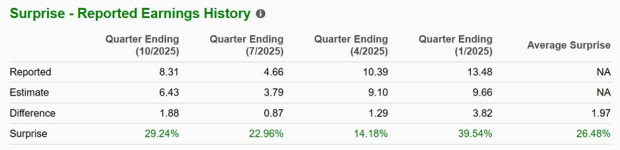

Based on Zacks estimates, Dillard’s Q4 sales are expected to be virtually flat from a year ago at $2.02 billion. Following a tough period to compete against in terms of operational performance, Dillard’s Q4 EPS is thought to have dipped to $9.98 from $13.48 per share in the comparative quarter.

That said, it’s noteworthy that Dillard’s has exceeded the Zacks EPS Consensus for five straight quarters with an impressive average earnings surprise of 26.48% in its last four quarterly reports.

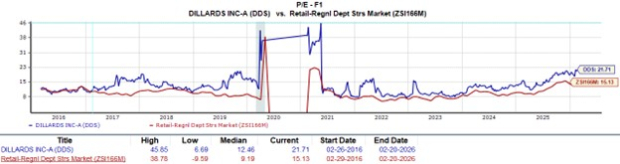

While Dillard’s bottom line is expected to contract, full-year EPS projections are still over a whopping $30.00 per share for fiscal 2026 and FY27. Making its robust earnings and the recent drop in Dillard’s stock more attractive is that DDS is now trading at a forward P/E multiple of 21X.

Offering a pleasant discount to the benchmark, DDS has gotten closer to its industry average of 15X forward earnings despite being a clear leader in the space.

Underscoring Dillard’s exceptional operational efficiency and cost discipline, the company’s cash position has surged past $1 billion, while total assets now exceed $4 billion against roughly $2.25 billion in total liabilities — highlighting one of the strongest balance sheets in the retail sector.

Dillard’s stock looks like a compelling buy-the-dip candidate ahead of its Q4 report because the setup combines temporary earnings pressure with underlying strength, exactly the mix that often creates opportunity when expectations erode beyond what fundamentals justify.

To that point, Dillard’s Q4 EPS expectations are unusually low, driven by margin pressure rather than collapsing demand, as sales forecasts suggest its core business is holding up even as profitability tightens.

Sporting a Zacks Rank #2 (Buy), Dillard’s top line is expected to increase by roughly 1% in FY26 and FY27, with projections edging north of $6.5 billion. More importantly, EPS revisions have trended higher for both fiscal years in the last 60 days.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 11 min | |

| 6 hours | |

| 10 hours | |

| 16 hours | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite