|

|

|

|

|||||

|

|

|

CorMedix CRMD and Theravance Biopharma TBPH occupy a similar niche in the market as small-cap biopharmaceutical companies working to turn promising science into sustainable revenues. Both companies, having a market cap of less than $1 billion, are either in the early stages of commercialization or working to expand the reach of key therapies, which means their stock prices can move sharply on clinical updates, regulatory decisions and early sales trends. For investors, that creates a classic biotech setup — higher risk, but also the potential for meaningful upside if execution goes well.

CorMedix’s lead product, DefenCath (Taurolidine + Heparin), received FDA approval in late 2023 as the first and only antimicrobial catheter lock solution available in the United States. It is indicated for reducing catheter-related bloodstream infections in adult patients with kidney failure undergoing chronic hemodialysis through a central venous catheter.

Although Theravance’s commercial portfolio lacks a marketed product, the company has collaborated with Viatris VTRS to develop and commercialize Yupelri, as a once-daily, nebulized treatment of chronic obstructive pulmonary disease (COPD).

While both companies face the usual risks and rewards of small-cap biotech investing, they are pursuing very different growth strategies. CorMedix is focused on driving near-term revenue through the commercial rollout of DefenCath, while Theravance is leveraging its stronger balance sheet to advance late-stage clinical programs and expand its pipeline. This contrast — immediate sales execution versus longer-term clinical upside — gives investors two distinct ways to play for the next potential growth story in the sector. Let’s dive into their fundamentals, growth outlook and potential challenges to make a well-informed comparison.

DefenCath is the first approved product in CorMedix’s marketed portfolio, giving the company a regular income stream. The product was launched in 2024 in both hospital inpatient and outpatient hemodialysis settings and has witnessed strong market adoption since.

Last month, CorMedix reported preliminary fourth-quarter and full-year 2025 results, with net revenues of approximately $127 million and $310 million, respectively. Preliminary net revenues for the fourth quarter and full-year 2025 reflect the growing momentum with DefenCath and early Melinta portfolio contributions. DefenCath holds a unique market position as the only FDA-approved therapy for a niche condition, supported by patent protection through 2033. CRMD is also planning future potential label expansion of DefenCath into total parenteral nutrition to increase its customer base

In August 2025, CorMedix took a significant step toward diversifying its revenues and reducing dependence on DefenCath with the $300 million acquisition of Melinta Therapeutics. The acquisition added seven approved therapies to CRMD’s portfolio, strengthening its presence in hospital acute care and infectious disease markets. The Melinta acquisition underscores CorMedix’s long-term strategy to accelerate growth by expanding its hospital-focused offerings while building a more durable, diversified commercial platform.

CorMedix’s latest future financial outlook has tempered investor expectations around DefenCath’s growth trajectory. Management introduced full-year 2026 revenue guidance of $300-$320 million, but DefenCath sales are expected to be front-loaded in early 2026, with only modest utilization gains offsetting ongoing pricing pressure. More importantly, the company projected 2027 DefenCath revenues of $100-$140 million based on higher net selling prices compared to 2026. Both guidance assumes flat usage among existing customers and excludes any benefit from new accounts, Medicare Advantage contracting, or reimbursement changes — signaling a more conservative, slower-growth outlook than many investors had anticipated and contributing to recent bearish sentiment. Amid such concerns, CorMedix’s heavy reliance on DefenCath for revenues remains a challenge.

The Viatris collaboration is the primary top-line contributor for Theravance. Viatris and TBPH are sharing U.S. profits and losses received in connection with the commercialization of Yupelri. While Viatris gets 65% of the profits, Theravance receives the remaining 35%. Theravance is entitled to low double-digit royalties on ex-U.S. net sales. Viatris recognizes product sales from Yupelri. VTRS also owns a stake in Theravance.

Yupelri is a once-daily nebulized long-acting muscarinic antagonist (LAMA) approved for COPD patients. LAMAs are recognized by international COPD treatment guidelines as a cornerstone of maintenance therapy for COPD, irrespective of the severity of the disease. Yupelri provides COPD patients with access to a nebulized LAMA therapy, offering a consistent 24-hour lung function improvement with the convenience of once-daily dosing delivered through any standard jet nebulizer.

The product has been witnessing strong sales, generating higher profit-sharing revenues for Theravance. Revenues from the Viatris collaboration rose 18.5% year over year in the first nine months of 2025.

Theravance is developing its lead pipeline candidate, ampreloxetine (TD-9855), a norepinephrine reuptake inhibitor for the treatment of symptomatic neurogenic orthostatic hypotension (nOH) in patients with multiple system atrophy (MSA).

The company initiated the phase III CYPRESS study evaluating ampreloxetine for nOH MSA in 2024. In August 2025, the company completed patient enrollment in the CYPRESS study. Top-line data from the same is expected in the first quarter of 2026. Theravance plans a regulatory filing, under the FDA’s priority review pathway, for ampreloxetine if the study data are found to be positive. The candidate enjoys the FDA’s Orphan Drug Designation status for the nOH indication in the United States.

Around mid-2025, Theravance agreed to sell its remaining royalty interest in net sales of Trelegy Ellipta to GSK for $225 million in cash. Following this, Theravance received a one-time cash payment of $225 million, significantly strengthening its balance sheet, reducing near-term financing risk, and extending its cash runway to advance pipeline development. Theravance held some royalty interest in GSK’s COPD medicine, Trelegy Ellipta.

Despite its solid cash position and growing collaboration revenues, Theravancefaces notable challenges that investors should watch closely. The company remains heavily dependent on profit-sharing income from Viatris for Yupelri, as it currently has no wholly-owned marketed products. Any disruption in this partnership or slower-than-expected sales growth could weigh on its top line. In addition, Theravance’s prospects hinge on the success of its late-stage candidate ampreloxetine, which has already faced clinical setbacks and enrollment delays in the ongoing late-stage study. A failure to achieve positive results or obtain regulatory approval would significantly limit TBPH’s near-term growth potential.

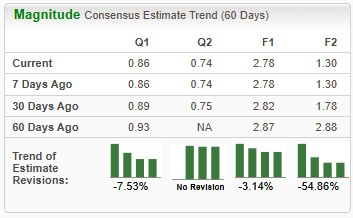

The Zacks Consensus Estimate for CorMedix’s 2025 sales and earnings per share (EPS) implies a year-over-year increase of around 614% and 1,027%, respectively. However, EPS estimates for 2025 and 2026 have been trending downward over the past 60 days.

The Zacks Consensus Estimate for Theravance’s 2025 sales implies a year-over-year increase of around 65%. Its EPS estimate for 2025 is currently pegged at 24 cents. EPS estimates for both 2025 and 2026 have remained constant over the past 60 days.

In the past six months, CRMD shares have plunged 48.9%, while TBPH shares have rallied 39.8%. In comparison, the industry has returned 22.8%, as seen in the chart below.

From a valuation standpoint, Theravance is more expensive than CorMedix based on the price-to-book (P/B) ratio. TBPH shares currently trade at 4.19 times trailing book value, higher than 1.48 for CRMD.

For investors seeking a small-cap biotech with visible earnings momentum and diversified growth potential, Theravance Biopharma, carrying a Zacks Rank #3 (Hold), is clearly the better pick over CorMedix, which currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Based on the above discussion, Theravance Biopharma appears to offer the more balanced risk-reward profile at this stage. Unlike CorMedix, which remains heavily dependent on a single product, TBPH benefits from a profit-sharing stream from Yupelri and a significantly strengthened balance sheet following the $225 million Trelegy royalty sale. That cash infusion reduces near-term financing risk and gives the company flexibility to advance its late-stage pipeline without immediate dilution concerns — a key advantage in the capital-intensive biotech space. Meanwhile, steady growth in collaboration revenues provides a measure of operating stability that many small-cap biotechs lack.

In contrast, CorMedix’s outlook has become uncertain as management signaled a more conservative trajectory for DefenCath, its primary revenue driver. Slowing growth expectations, pricing pressure and competitive risks create a narrower margin for error. TBPH, by comparison, combines growing collaboration income with a potentially transformative late-stage catalyst in ampreloxetine, supported by the Orphan Drug status and a clear regulatory pathway. For investors seeking a stronger small-cap play with diversified drivers and a fortified cash position, TBPH currently stands out as the more compelling pick in 2026 over CRMD.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 2 hours | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-04 | |

| Jul-29 | |

| Jul-29 | |

| Jul-22 | |

| Jul-09 | |

| Jul-01 | |

| Jun-30 | |

| Jun-29 | |

| Jun-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite