|

|

|

|

|||||

|

|

|

Both Iovance Biotherapeutics IOVA and Rigel Pharmaceuticals RIGL are small-cap companies focused on the successful commercialization of their marketed products.

While Iovance is a cancer biotech concentrated on developing immunotherapies, Rigel's focus is on hematologic disorders and cancer.

But which one makes for a better investment pick today? Let's examine the fundamentals of the two stocks to make a prudent choice.

This California-based company has two marketed products in its portfolio, the IL-2 product Proleukin and the TIL therapy Amtagvi. While Proleukin is approved to treat metastatic renal cell carcinoma and metastatic melanoma in adults, Amtagvi is approved for the advanced melanoma indication.

Amtagvi is the first FDA-approved, individualized, one-time cell therapy for melanoma patients. Before the drug’s commercial launch in second-quarter 2024, there were no marketed therapies for advanced melanoma that progressed on or after prior anti-PD-1/L1 therapy. In the first nine months of 2025, Iovance generated $155.1 million from Amtagvi’s sales, up 183% year over year, fueled by patient enrolments. This momentum is expected to continue in the soon-to-be-reported fourth-quarter 2025 results and beyond.

This encouraging demand is expected to drive Proleukin sales, as it is used in the Amtagvi regimen. IOVA anticipates generating total product revenues between $250 million and $300 million for the full year 2025, with the majority coming from Amtagvi.

The company is evaluating Amtagvi across several label expansion studies in other cancer indications, which include cervical cancer, endometrial cancer, non-small cell lung cancer (NSCLC), and head and neck squamous cell carcinoma (HNSCC) indications. Iovance is on track to submit a regulatory filing with the FDA for the drug in the NSCLC indication later this year and expects to report data from the cervical cancer study in early 2026.

Iovance is developing other pipeline candidates. It is currently evaluating IOV-2001 in relapsed/refractory chronic lymphocytic leukemia (CLL) or small lymphocytic leukemia (SLL) in a phase I/II study. Another phase I/II study is evaluating the company’s first TALEN-edited TIL therapy candidate, IOV-4001, in patients with advanced melanoma and metastatic NSCLC in two separate cohorts. Data from the efficacy portion of this study is expected in early 2026. The company is assessing IOV-3001, a second-generation modified IL-2 analog, for use in the TIL therapy treatment regimen in a phase I/II study.

The year 2025 was turbulent for Iovance. It started when the company cautioned investors (in an annual SEC filing) against facing economic uncertainty due to geopolitical conflicts and inflation that could harm its business and market performance. In May, IOVA lowered its full-year 2025 product revenue guidance to $250-$300 million from the prior projection of $450-$475 million due to the anticipated growth in authorized treatment centers, adoption trends and patient referral timelines. In August, Iovance announced that it had voluntarily withdrawn the regulatory filing for Amtagvi in the EU due to a lack of alignment with the EMA on clinical data supporting the submission. These developments were responsible for the negative sentiments surrounding IOVA stock, which led to a substantial drop in stock price last year.

In contrast, Rigel Pharmaceuticals has delivered an encouraging performance in 2025, driven by the strong financial performance of its marketed products, especially Tavalisse, which accounts for the majority of the company’s top line. This drug is approved to treat adults with low platelet counts due to chronic immune thrombocytopenia (ITP) who have an insufficient response to prior treatment.

Although RIGL has yet to report its fourth-quarter and full-year 2025 results, it released preliminary figures last month indicating a strong finish. Based on the unaudited numbers, full-year 2025 product sales are expected to rise 60% year over year to $232 million, exceeding prior guidance of $225-$230 million. This outperformance reflects sustained demand for all marketed drugs.

Tavalisse remained the key driver of revenues for Rigel, generating nearly $159 million during the full year, reflecting a 52% year-over-year increase and accounting for more than half of the company’s top line. Continued strong new patient demand supported the performance, reinforcing the drug’s position as the foundation of Rigel’s commercial portfolio.

The company’s two oncology assets added incremental momentum. The RET-gene targeting drug Gavreto contributed about $42 million in full-year sales, while the acute myeloid leukemia (AML) drug Rezlidhia added $31 million. Though smaller in scale compared to Tavalisse, these therapies are gradually expanding and diversifying Rigel’s revenue base.

Rigel projects 2026 net product sales of $255-$265 million, suggesting continued portfolio momentum. It expects to achieve positive net income for the full year while continuing to fund existing and new clinical development programs.

Beyond its commercial portfolio, RIGL continues to advance its pipeline programs. Its lead candidate is a dual IRAK1/4 inhibitor called R289, which is being evaluated in a phase Ib study for lower-risk myelodysplastic syndrome (MDS). A data readout from this study is expected before the end of this year. The company is exploring label expansion opportunities for Rezlidhia in other cancer indications, through collaborations with the University of Texas MD Anderson Cancer Center and Collaborative Network for Neuro Oncology Clinical Trials.

Rigel faces stiff competition from Big Pharma in its target markets. Last year, the FDA approved Sanofi’s SNY Wayrilz, a novel BTK inhibitor, for an indication similar to Tavalisse. Though both the RIGL and SNY medications are built on different mechanisms, a successful launch of Wayrilz is likely to pose a significant threat to Tavalisse, given the resources available for a large drugmaker like Sanofi.

Gavreto competes in the RET fusion-positive NSCLC and advanced thyroid cancer markets against Eli Lilly’s LLY Retevmo, another RET inhibitor with an established presence.

The Zacks Consensus Estimate for IOVA’s 2026 sales is expected to grow by more than 81% year over year, while the company’s loss estimates per share are expected to improve by 34%. Bottom-line estimates per share for 2026 have remained stable in the past 30 days.

For Rigel, the Zacks Consensus Estimate for 2026 sales is expected to decline by 3% year over year, while EPS estimates are expected to drop by about 41%. Bottom-line estimates for 2026 have been trending upwards over the past 30 days.

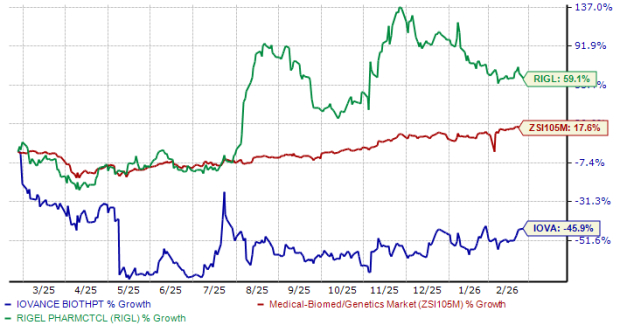

In the past year, shares of IOVA have plummeted 46%, while those of RIGL have surged 59%. In comparison, the industry has climbed nearly 18%, as seen in the chart below.

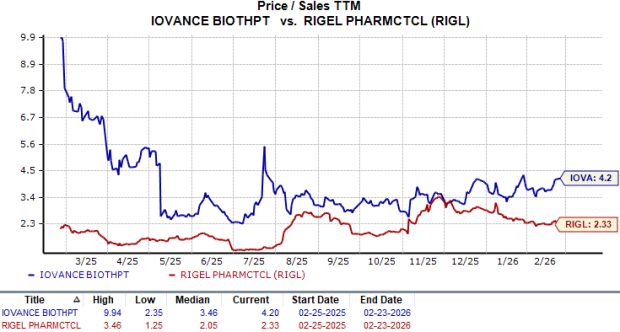

From a valuation standpoint, Iovance Biotherapeutics seems to be trading at a premium compared to Rigel Pharmaceuticals, going by the price/sales (P/S) ratio. IOVA’s shares currently trade at 4.20 times trailing 12-month sales, higher than 2.33 for RIGL.

Both stocks have a Zacks Rank #3 (Hold), which makes choosing one over the other difficult. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Iovance seems to be the safer pick at present, despite its premium valuation. The company benefits from a longer growth runway, supported by the expanding commercial opportunity for Amtagvi and multiple ongoing label-expansion and pipeline programs. Rigel, although operationally stronger in the near term, has a more concentrated portfolio and faces rising competitive pressure in its key markets from Big Pharma.

IOVA has significantly underperformed RIGL, reflecting past execution and regulatory setbacks rather than a deterioration in long-term fundamentals. If commercialization trends stabilize and pipeline catalysts play out, Iovance offers greater upside optionality, whereas Rigel’s recent rally leaves comparatively less room for multiple expansion.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 8 hours |

There's A Hidden Gem In Eli Lilly's Weight-Loss News - And It Could Slam Compounders

LLY

Investor's Business Daily

|

| 8 hours | |

| 8 hours | |

| 10 hours | |

| 11 hours | |

| 13 hours | |

| 14 hours | |

| 15 hours |

Eli Lilly Preparing Retatrutide Applications After Positive Weight-Loss Data

LLY

The Wall Street Journal

|

| 15 hours | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite