|

|

|

|

|||||

|

|

|

Walmart Inc. WMT and Dollar General Corporation DG are both stalwarts in the retail sector, selling everyday essentials like groceries, household goods and basic apparel.

Walmart is a global behemoth with massive scale, sprawling supercenters, and a growing e-commerce business and recently approached the $1 trillion market cap milestone, underscoring its dominant footprint. Dollar General, by contrast, operates a dense network of smaller stores focused on convenience and low prices, particularly in rural and suburban America, with a market cap around $33 billion reflective of a leaner, niche-focused business model.

What ties the two together is their positioning in value-oriented retail. Both cater to cost-conscious consumers and have been shaped by macro-economic pressures like inflation and shifting spending patterns. As retail dynamics shift, comparing their different approaches to scale and convenience offers useful insight for investors.

Walmart’s strength is grounded in the durability of its scale-driven model and ability to generate consistent cash flow across cycles. As the largest retailer globally, its purchasing leverage, logistics network, and everyday low-price positioning create structural cost advantages that support traffic stability and market share gains. The business is anchored in essential categories such as grocery, which drive recurring visits and make earnings more defensive relative to discretionary-focused peers.

WMT’s recently reported fourth-quarter fiscal 2026 results reinforced these fundamentals. The quarter showed steady revenue growth, with operating income expanding at a faster pace, reflecting improved mix and productivity initiatives. Digital channels continue to scale, with strength in e-commerce, marketplace penetration and advertising. These higher-margin revenue streams are gradually diversifying the profit base. Omnichannel capabilities, including pickup and delivery, further deepen customer engagement.

Operational investments in automation, fulfillment, and data analytics are improving productivity and strengthening omnichannel integration across stores and digital platforms. Ongoing supply-chain upgrades and store remodels enhance in-stock levels, speed and overall customer experience, reinforcing Walmart’s competitive position. Strong operating cash flow funds these initiatives while supporting dividends and share repurchases, maintaining financial flexibility and balance sheet strength.

While the retail environment remains competitive, with ongoing price pressure, a heavier mix of lower-margin essentials, rising wages, and continued investment spending, Walmart’s scale and steady customer traffic provide stability. Its expanding higher-margin businesses and strong cash generation support a positive long-term outlook, positioning the company to navigate shifts in consumer spending while delivering consistent earnings growth over time.

Dollar General continues to capture market share, supported by a steady essential-heavy assortment, a clear value focus and ongoing store expansion. Its renewed emphasis on core retail execution has reinforced operational discipline, strengthening a model that typically performs well when household budgets are tight. This value positioning helps maintain consistent traffic while also attracting a broader customer base, including higher-income shoppers looking for everyday savings.

Growth is further underpinned by an active and structured real estate plan focused on productivity and reach. In fiscal 2026, the company intends to complete roughly 4,730 real estate projects, including approximately 450 new U.S. store openings, around 10 new stores in Mexico, 2,000 Project Renovate remodels and 2,250 Project Elevate remodels. These initiatives are aimed at refreshing older locations, optimizing assortments and improving store layouts to sustain sales performance. With an estimated 11,000 additional potential store opportunities across the United States, the runway for expansion remains significant.

Operationally, progress in lowering shrink and improving merchandise margins has supported a gradual margin recovery. Better inventory management and forecasting are helping balance availability with profitability. While consumables continue to anchor traffic, discretionary categories such as home, seasonal and apparel are also contributing, reflecting improved merchandising and space utilization.

Digital and convenience initiatives are also advancing. myDG Delivery now serves more than 17,000 stores, expanding same-day access to essentials, particularly in rural markets. Partnerships with platforms such as DoorDash and Uber Eats further extend reach, supporting incremental traffic, larger baskets and stronger customer engagement.

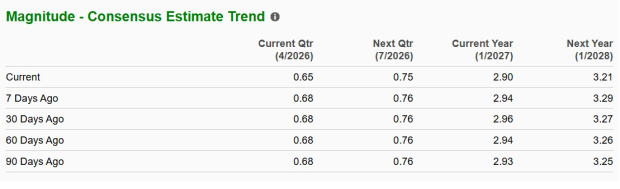

The Zacks Consensus Estimate for Walmart’s current and next fiscal-year earnings per share (EPS) has gone down 1.4% to $2.90 and 1.5% to $3.21, respectively, over the past 60 days. However, these consensus estimates imply year-over-year growth of 9.9% and 10.7%, respectively.

Wall Street analysts have expressed confidence in Dollar General by raising their earnings estimates. Over the past 60 days, the Zacks Consensus Estimate for the current and next fiscal years has risen by a couple of cents to $6.49 and $7.08 per share, respectively. These estimates indicate year-over-year growth rates of 9.6% and 9.2%, respectively.

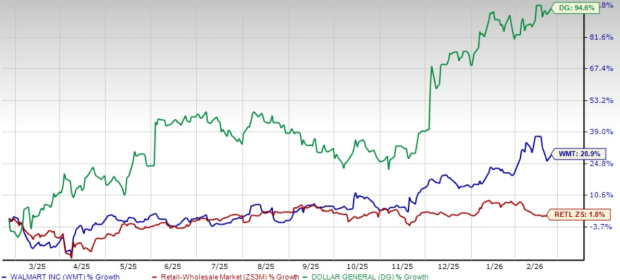

Over the past year, shares of Walmart have rallied 28.9%, while Dollar General has soared 94.6% — both comfortably outpacing the Zacks Retail – Wholesale sector’s return of 1.8% in the same time frame.

Walmart trades at a forward P/E of 43.13, above its one-year median of 36.27, reflecting the market’s willingness to pay a premium for its scale, earnings visibility and defensive positioning. Dollar General, at a forward P/E of 21.42 versus a one-year median of 17.27, has also seen some valuation expansion but remains lower on an absolute basis.

Both Walmart and Dollar General are strong retailers with distinct strengths. Walmart offers unmatched scale, stability and steady growth, making it a dependable choice for long-term investors who value consistency. Dollar General, meanwhile, appears to be amid an operational recovery, supported by improving margins, disciplined expansion and strengthening earnings sentiment. With sharper recent stock momentum, improving fundamentals and a comparatively more moderate valuation, DG currently looks like the more attractive bet for investors seeking greater upside potential.

Dollar General currently carries a Zacks Rank #2 (Buy), while Walmart has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-09 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite