|

|

|

|

|||||

|

|

|

Behind every generative AI model and autonomous system is massive compute infrastructure, especially data centers full of GPUs that train and serve models. Two very different public companies that are riding this trend are CoreWeave, Inc. CRWV, a specialized AI infrastructure upstart, and Microsoft Corporation MSFT, an established tech giant.

As enterprises and governments race to deploy generative AI, spending on AI data centers and accelerated computing is surging, creating a multitrillion-dollar opportunity for the companies that supply the backbone of this ecosystem. Both CoreWeave and Microsoft are key players in the AI infrastructure space. CRWV as a specialized GPU-based cloud provider and MSFT as a dominant cloud and AI platform through Azure, making them natural competitors for investors seeking exposure to AI computing demand.

While both are direct beneficiaries of the AI wave, their risk-reward profiles are very different. So, let’s deep dive into which might be the smarter bet now, based on growth potential, fundamentals, valuation and risk profile.

CoreWeave has emerged as one of the most important GPU cloud providers for AI workloads. It is benefiting from strong demand for its AI cloud, a rapidly expanding backlog and a growing, diversified customer base. Although supply-chain constraints have prompted cuts to its full-year revenue and CapEx outlook, the company highlighted its operational agility, broad growth roadmap and solid access to capital. Management remains confident in its ability to meet long-term demand, scale capacity and strengthen its position in AI cloud as new offerings, partnerships and federal deals ramp, keeping the hypergrowth story intact.

CoreWeave’s moat is its pure-play specialization. Its partnerships with NVIDIA Corporation NVDA, OpenAI, Meta and others underline its relevance in the compute stack. Multi-billion-dollar, long-term contracts with top AI players, including an expanded OpenAI deal worth up to $6.5 billion (taking total OpenAI agreements to about $22.4 billion) and a Meta cloud capacity agreement valued at up to $14.2 billion through 2031, provide strong revenue visibility and a durable growth pipeline.

NVIDIA’s $2 billion investment in January 2026, which nearly doubled its stake, supports CoreWeave’s plan to scale to 5GW of data-center capacity by 2030 and underscores confidence in AI demand. The planned early deployment of NVIDIA’s Rubin platform in the second half of 2026 further positions CoreWeave at the leading edge of next-gen AI workloads, including agentic AI, advanced reasoning and large-scale inference.

CRWV’s disciplined capacity expansion lifted contracted power to 2.9 GW in the third quarter, with no data center partner accounting for more than roughly 20%, improving resilience and geographic diversification. The company also walked away from the Core Scientific acquisition on valuation grounds, noting the decision does not affect its growth outlook and that it will continue leveraging the approximately 590 MW already leased. Expanding its capacity and service offerings remains a key performance catalyst to its success in a structurally undersupplied market.

However, powered shell delays are set to drag on fourth-quarter results, with softer 2025 revenue and profit guidance, even though active power is still expected to exceed 850 MW by year-end. As major deployments come online in the fourth quarter, a timing gap between initial cost outlays and revenue contribution will likely weigh on adjusted operating margins for the quarter. Nonetheless, with powered shell deliveries taking longer, more infrastructure is staying in the build phase, pushing most of the previously expected fourth-quarter spend into first-quarter 2026.

Microsoft reported a strong second-quarter fiscal 2026, with Microsoft Cloud revenue topping $50 billion and strong traction in Copilot and AI infrastructure. The results reflect its deep push into AI, expansion of the platform ecosystem and new long-term agreements that justify sustained high CapEx. Management remains upbeat about ongoing growth across commercial and enterprise segments, driven by global capacity buildout and multiple revenue pillars, while noting investor focus on the payback from heavy AI spending and exposure to a few large customers.

Microsoft’s model combines cloud infrastructure, productivity tools, business applications, gaming, professional networking and advertising, giving it a highly diversified revenue base that helps cushion against weakness in any single segment. Its subscription-driven offerings — including Microsoft 365, Azure and Dynamics deliver predictable, recurring income with strong renewal rates. The company is also geographically balanced, with meaningful contributions from North America, Europe and Asia-Pacific, limiting reliance on one economy. A core focus on enterprise customers ties performance to relatively resilient corporate IT spending, while Xbox and Activision Blizzard provide consumer entertainment exposure, and LinkedIn adds a distinct presence in professional services, together creating a well-rounded, durable growth portfolio.

Microsoft’s moat is breadth and integration. AI runs through its cloud, productivity suites, developer tools, search and advertising, and enterprise software. This means Microsoft is not dependent on sales like GPU hours alone. It also benefits from robust recurring revenue streams. Moreover, Microsoft’s partnerships, including a major equity stake and AI collaboration with OpenAI, put it at the center of the AI ecosystem.

Microsoft’s commercial RPO climbed to $625 billion with an average duration of 2.5 years, giving it powerful forward revenue visibility. About 25% is set to be recognized within the next 12 months, up 39% year over year, signaling faster backlog conversion. Large AI commitments from OpenAI and Anthropic underscore Azure’s leadership, while the remaining 55% of RPO grew 28%, pointing to broad, global demand. This record backlog lowers near-term growth risk, supports upcoming revenue guidance and better aligns infrastructure spending with revenue realization, reinforcing expectations for sustained double-digit growth through fiscal 2026.

However, Azure is under constant pressure from deep-pocketed rivals. AWS still leads with unmatched scale and a broader service stack, while Google Cloud competes aggressively on price to gain share. As cloud infrastructure becomes more commoditized, pricing battles are squeezing margins, and niche providers are chipping away at specialized workloads. This forces Microsoft to keep investing heavily just to defend its position, raising the risk to profitability and making it harder to sustain premium growth in its most critical segment.

Further, Microsoft’s surging AI and cloud buildout has pushed capital spending to record levels, with fiscal 2026 CapEx set to grow even faster than in 2025. These hefty annual investments mark a sharp break from past spending trends, putting pressure on near-term cash flow and reducing financial flexibility. The long payback period also raises execution risk if AI monetization or cloud growth falls short of expectations.

In the past three months, CRWV has surged 27.4% while MSFT is down 19.4%.

In terms of Price/Book, CRWV shares are trading at 9.05X, higher than MSFT’s 7.3X.

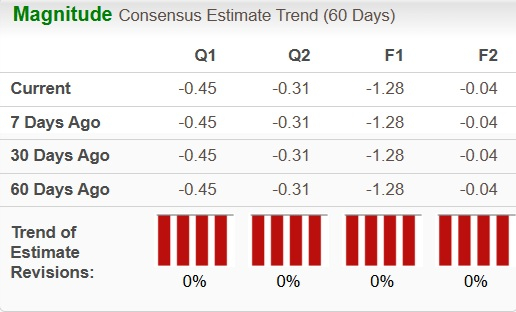

The Zacks Consensus Estimate for CRWV’s earnings for the current year has remained unchanged over the past 60 days.

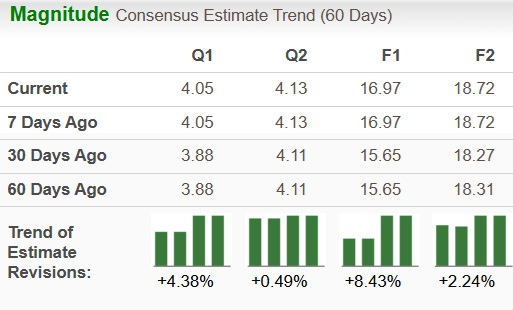

For MSFT, there has been an upward revision.

Both companies are central to the AI revolution. CRWV looks better positioned for near-term outperformance because we are in the AI capacity-deployment phase, where backlog conversion, new cluster go-lives and surging compute demand can drive faster revenue growth and estimate upgrades. It’s the higher-beta way to play the current AI infrastructure ramp.

MSFT, however, remains the stronger long-term buy, with AI monetization through Azure and Copilot, massive RPO visibility and diversified cash flows that should translate into steadier compounding as margins expand. CRWV and MSFT both have a Zacks Rank #3 (Hold). Consequently, in terms of valuation, CRWV seems to be a better pick at the moment. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 2 hours | |

| 3 hours | |

| Jul-29 | |

| Jul-29 |

Even $64 Billion in Quarterly Profit Is a Disappointment for Chip Investors

MSFT MSFT +7.12%

The Wall Street Journal

|

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Dow Jones Futures Rise; Microsoft, Meta Lead Big Earnings After Market Tumbles, Oil Prices Soar

MSFT MSFT +7.12%

Investor's Business Daily

|

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite