|

|

|

|

|||||

|

|

|

Cisco Systems’ CSCO networking revenues picked up in the second quarter of fiscal 2026, with the figure hitting $8.29 billion, up 21% on a year-over-year basis and 6.8% sequentially. The second-quarter fiscal 2026 results benefited from robust demand for AI infrastructure and campus networking solutions. The company’s networking portfolio, powered by Silicon One, AI-native security solutions and operating systems, is expanding CSCO’s AI footprint.

Cisco’s prospects ride on strong product growth. In the fiscal second quarter, networking product orders continued to accelerate, reaching more than 20% and marked the sixth consecutive quarter of double-digit growth. This was driven by service provider routing, data center switching, campus switching, wireless, servers and industrial IoT products.

Campus networking is benefiting from strong demand for next-gen solutions, including smart switches, secure routers and Wi-Fi 7 wireless products. CSCO’s networking portfolio, powered by Silicon One, AI-native security solutions and operating systems, is expanding CSCO’s AI footprint. Networking product orders grew 20% in the fiscal second quarter, which marked the sixth consecutive quarter of double-digit growth driven by hyperscale infrastructure, enterprise routing, campus switching, wireless, industrial IoT and servers. This bodes well for Networking revenues in fiscal 2026.

Cisco is facing stiff competition from Arista Networks ANET and Hewlett Packard HPE in the networking domain.

Arista Networks holds a leadership position in 100-gigabit Ethernet switches and is increasingly gaining market traction in 200 and 400-gigabit high-performance switching products. ANET’s advanced cloud native software and smart Wi-Fi solutions deliver intelligent application identification, automated troubleshooting and location services, efficiently supporting apps like Teams, Zoom and Google Meet. The Arista 2.0 strategy is resonating well with customers, as its modern networking platforms are foundational for the transformation from silos to data centers.

Hewlett Packard Enterprise views AI, Industrial Internet of Things (IoT) and distributed computing as the next major markets. The acquisition of Juniper Networks has elevated Hewlett Packard Enterprise’s competitive stance by expanding its networking domain in AI, cloud and hybrid solutions. Its multi-billion-dollar investment plan across expanding networking capabilities will diversify the business from the server and hardware storage markets and boost margins in the long run.

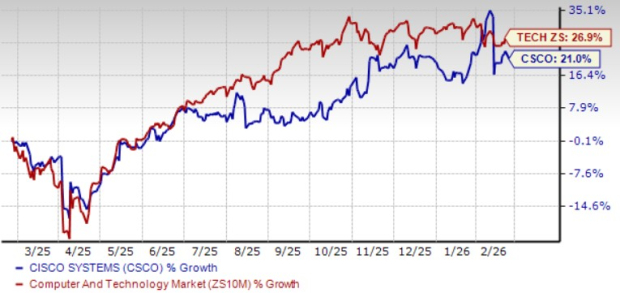

Cisco shares have appreciated 21% in a year, underperforming the broader Zacks Computer and Technology sector’s return of 26.9%.

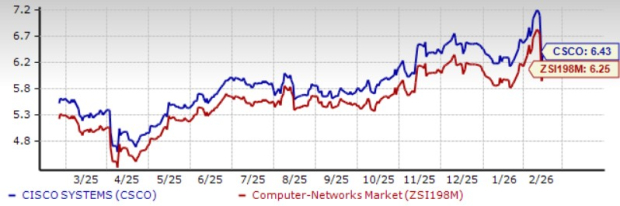

The CSCO stock is trading at a premium, with a trailing 12-month price/book of 6.43X compared with the Zacks Computer Networking industry’s 6.25X. Cisco has a Value Score of F.

The Zacks Consensus Estimate for second-quarter fiscal 2026 earnings is currently pegged at $1.03 per share, up by a penny over the past 30 days, suggesting 7.3% growth from the figure reported in the year-ago quarter.

Cisco Systems, Inc. price-consensus-chart | Cisco Systems, Inc. Quote

Cisco currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite