|

|

|

|

|||||

|

|

|

As the Q4 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the auto parts retailer industry, including O'Reilly (NASDAQ:ORLY) and its peers.

Cars are complex machines that need maintenance and occasional repairs, and auto parts retailers cater to the professional mechanic as well as the do-it-yourself (DIY) fixer. Work on cars may entail replacing fluids, parts, or accessories, and these stores have the parts and accessories or these jobs. While e-commerce competition presents a risk, these stores have a leg up due to the combination of broad and deep selection as well as expertise provided by sales associates. Another change on the horizon could be the increasing penetration of electric vehicles.

The 5 auto parts retailer stocks we track reported a mixed Q4. As a group, revenues were in line with analysts’ consensus estimates.

While some auto parts retailer stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 3.2% since the latest earnings results.

Serving both the DIY customer and professional mechanic, O’Reilly Automotive (NASDAQ:ORLY) is an auto parts and accessories retailer that sells everything from fuel pumps to car air fresheners to mufflers.

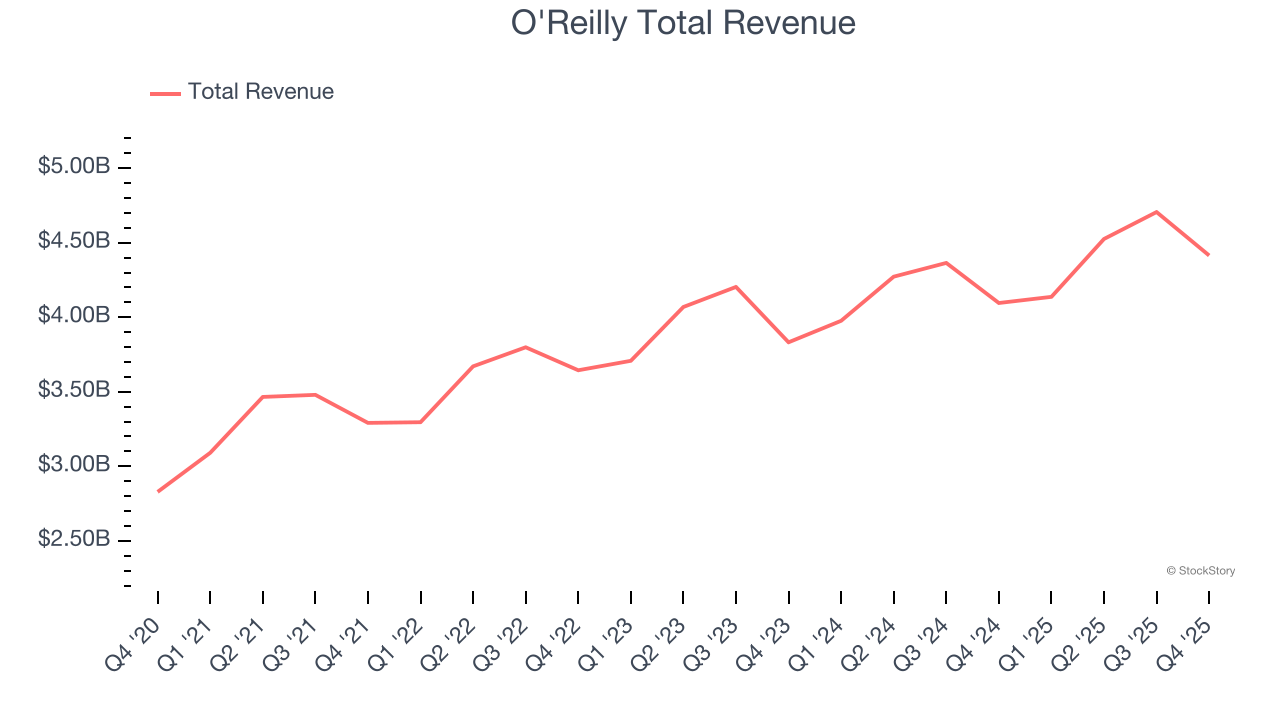

O'Reilly reported revenues of $4.41 billion, up 7.8% year on year. This print was in line with analysts’ expectations, but overall, it was a slower quarter for the company with full-year EPS guidance missing analysts’ expectations and full-year revenue guidance slightly missing analysts’ expectations.

Brad Beckham, O’Reilly’s CEO, commented, “I would like to thank our over 93,000 Team Members for their tremendous hard work and commitment while delivering a strong finish to 2025. Our Team continues to drive share gains on both sides of our business through excellent customer service and industry-leading parts availability, resulting in our fourth quarter comparable store sales growth of 5.6%. Our top-line results, coupled with strong gross margin performance, drove a 12% increase in operating profit dollars and a 13% increase in diluted earnings per share for the fourth quarter. We are pleased with our Team’s ability to capitalize on the investments we are making in our business and manage operating costs to provide exceptional customer service and capture market share; however, SG&A expenses again exceeded our expectations in the fourth quarter due to pressure from heightened inflation in team member health care and casualty claim costs. We remain intensely focused on managing expenses and mitigating these cost pressures but will always prioritize delivering the service levels and parts availability in our stores that are critical to winning share and driving industry-leading results.”

O'Reilly delivered the weakest full-year guidance update of the whole group. Unsurprisingly, the stock is down 2.2% since reporting and currently trades at $94.58.

Is now the time to buy O'Reilly? Access our full analysis of the earnings results here, it’s free.

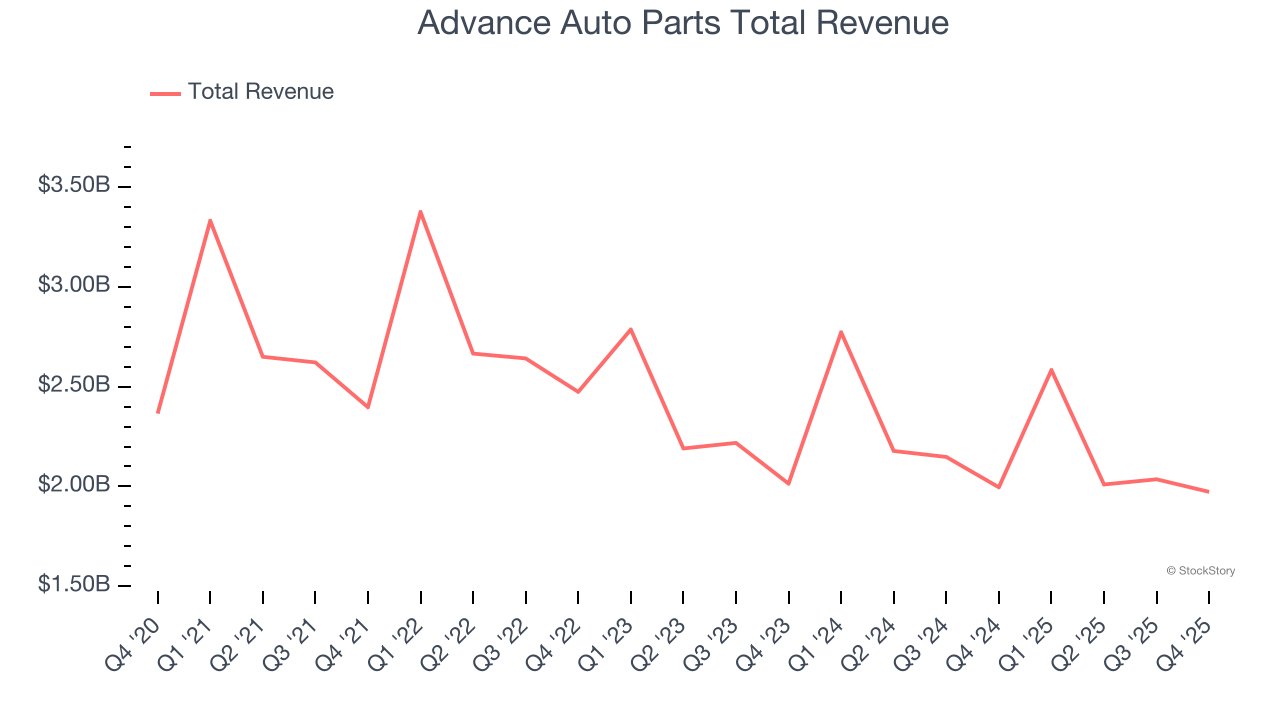

Founded in Virginia in 1932, Advance Auto Parts (NYSE:AAP) is an auto parts and accessories retailer that sells everything from carburetors to motor oil to car floor mats.

Advance Auto Parts reported revenues of $1.97 billion, down 1.2% year on year, outperforming analysts’ expectations by 1%. The business had a strong quarter with a beat of analysts’ EPS estimates and full-year EPS guidance exceeding analysts’ expectations.

Advance Auto Parts scored the biggest analyst estimates beat and highest full-year guidance raise among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 6.9% since reporting. It currently trades at $54.20.

Is now the time to buy Advance Auto Parts? Access our full analysis of the earnings results here, it’s free.

Aiming to be a one-stop shop for the DIY customer, AutoZone (NYSE:AZO) is an auto parts and accessories retailer that sells everything from car batteries to windshield wiper fluid to brake pads.

AutoZone reported revenues of $4.63 billion, up 8.2% year on year, in line with analysts’ expectations. It was a slower quarter as it posted a miss of analysts’ EBITDA estimates and a significant miss of analysts’ EPS estimates.

The stock is flat since the results and currently trades at $3,792.

Read our full analysis of AutoZone’s results here.

Started as a single location in Rochester, New York, Monro (NASDAQ:MNRO) provides common auto services such as brake repairs, tire replacements, and oil changes.

Monro reported revenues of $293.4 million, down 4% year on year. This result missed analysts’ expectations by 0.6%. In spite of that, it was a strong quarter as it put up a beat of analysts’ EPS estimates and a decent beat of analysts’ EBITDA estimates.

Monro had the slowest revenue growth among its peers. The stock is up 11.1% since reporting and currently trades at $22.25.

Read our full, actionable report on Monro here, it’s free.

Largely targeting the professional customer, Genuine Parts (NYSE:GPC) sells auto and industrial parts such as batteries, belts, bearings, and machine fluids.

Genuine Parts reported revenues of $6.01 billion, up 4.1% year on year. This number lagged analysts' expectations by 0.8%. It was a softer quarter as it also logged full-year EPS guidance missing analysts’ expectations significantly and a significant miss of analysts’ EBITDA estimates.

Genuine Parts had the weakest performance against analyst estimates among its peers. The stock is down 18.6% since reporting and currently trades at $119.78.

Read our full, actionable report on Genuine Parts here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.

| Aug-06 | |

| Aug-04 | |

| Aug-03 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-27 | |

| Jul-13 | |

| Jul-10 | |

| Jul-07 | |

| Jul-06 | |

| Jul-06 | |

| Jul-03 | |

| Jul-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite