|

|

|

|

|||||

|

|

|

New Elite Feature: Compare relative returns, fundamentals, and sector rankings head-to-head.

What a fantastic six months it’s been for Moderna. Shares of the company have skyrocketed 99.8%, hitting $50.65. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy Moderna, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Despite the momentum, we're cautious about Moderna. Here are three reasons why MRNA doesn't excite us and a stock we'd rather own.

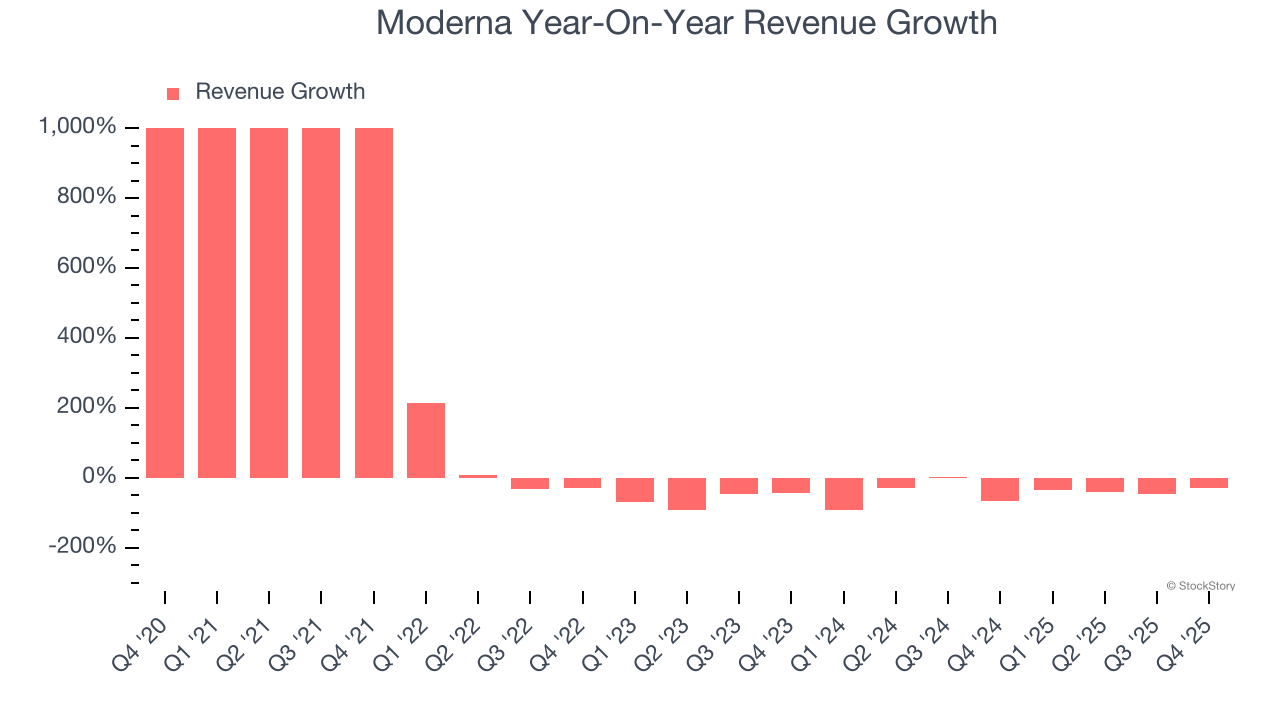

We at StockStory place the most emphasis on long-term growth, but within healthcare, a stretched historical view may miss recent innovations or disruptive industry trends. Moderna’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 46.7% over the last two years.

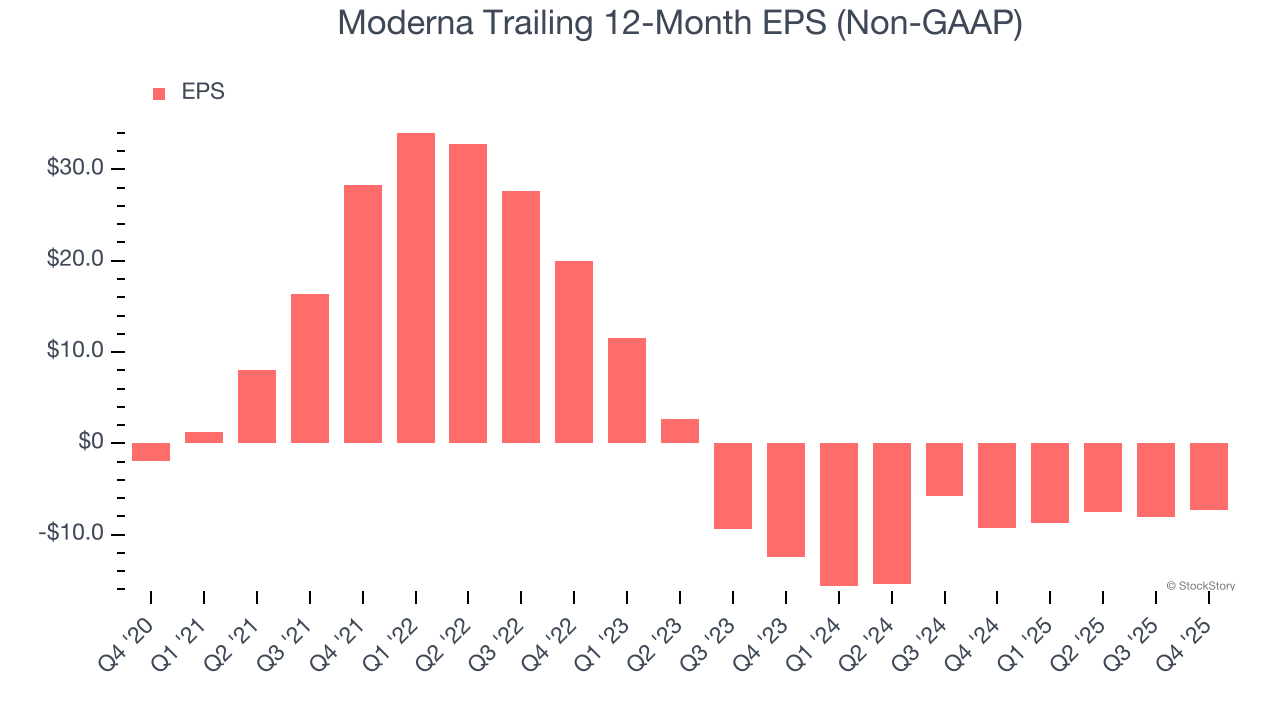

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Moderna’s earnings losses deepened over the last five years as its EPS dropped 30.2% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Moderna’s low margin of safety could leave its stock price susceptible to large downswings.

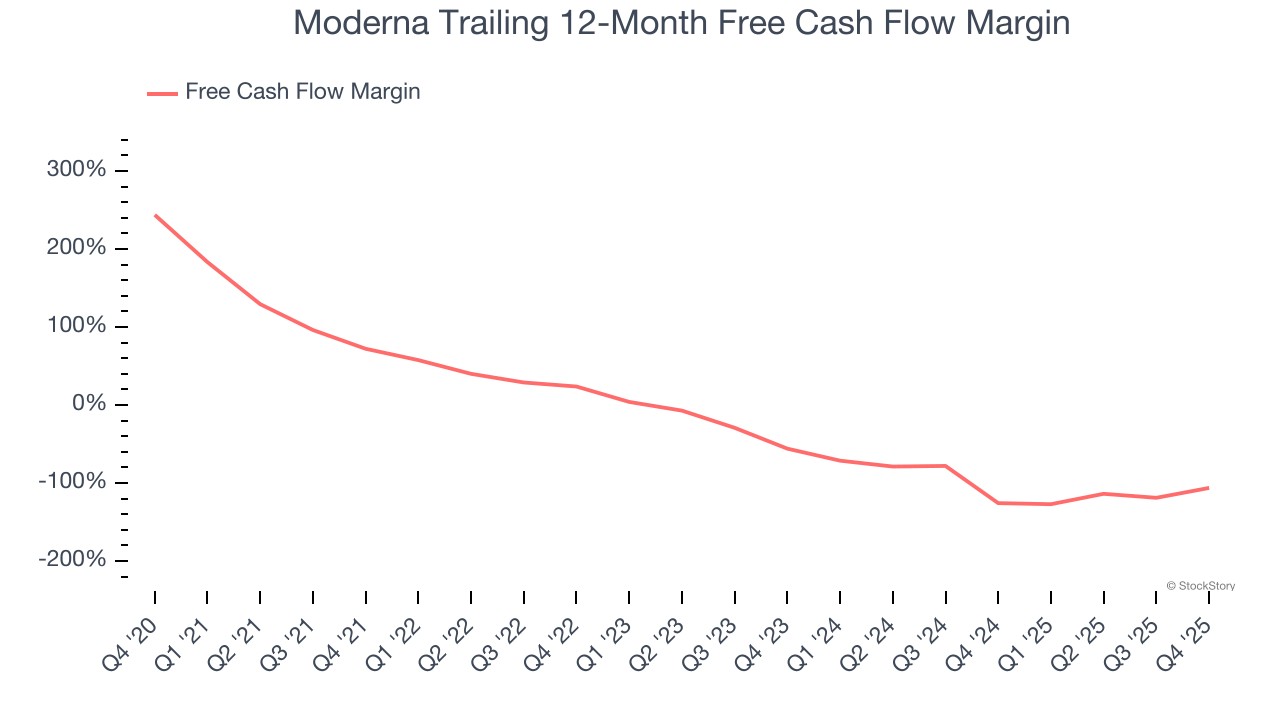

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Moderna’s margin dropped meaningfully over the last five years. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal it is in the middle of an investment cycle. Moderna’s free cash flow margin for the trailing 12 months was negative 106%.

We see the value of companies making people healthier, but in the case of Moderna, we’re out. After the recent rally, the stock trades at $50.65 per share (or a forward price-to-sales ratio of 9.8×). The market typically values companies like Moderna based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy. We’d suggest looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Jun-02 | |

| Jun-01 | |

| Jun-01 | |

| Jun-01 | |

| Jun-01 | |

| May-28 | |

| May-27 | |

| May-26 | |

| May-21 | |

| May-20 | |

| May-20 | |

| May-20 | |

| May-20 | |

| May-19 | |

| May-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite