|

|

|

|

|||||

|

|

|

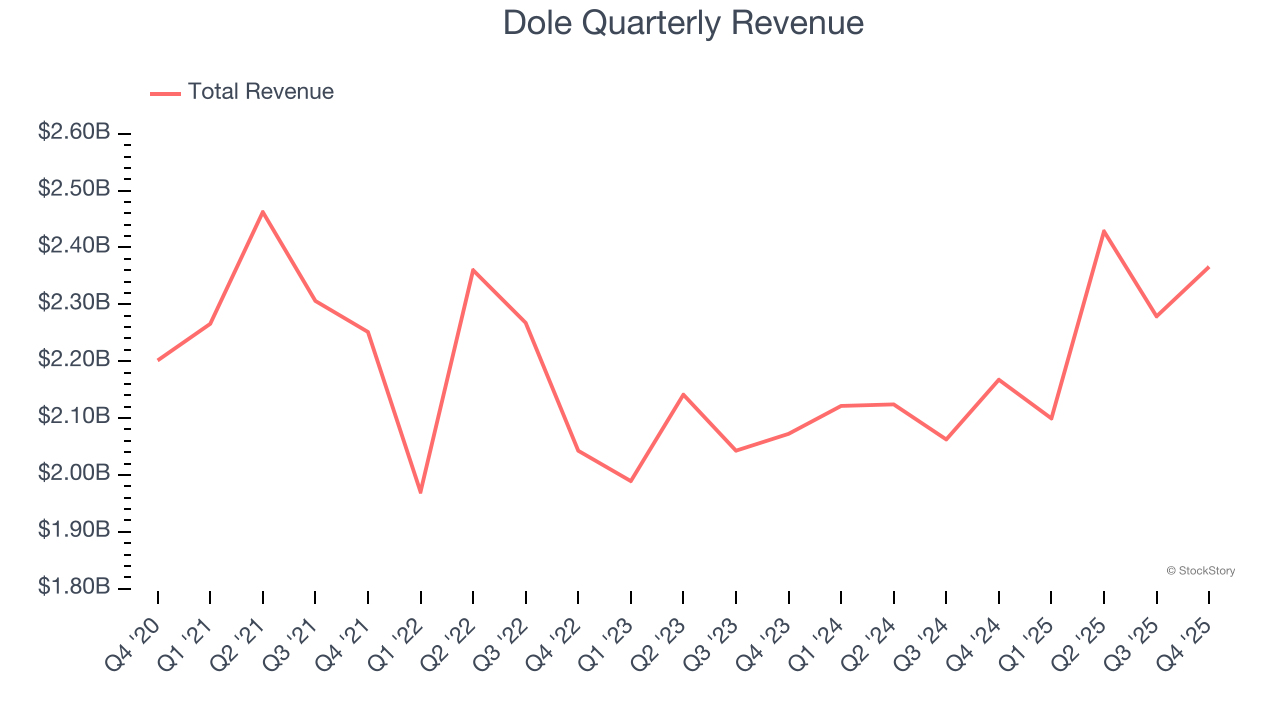

Fresh produce company Dole (NYSE:DOLE) announced better-than-expected revenue in Q4 CY2025, with sales up 9.2% year on year to $2.37 billion. Its non-GAAP profit of $0.14 per share was in line with analysts’ consensus estimates.

Is now the time to buy Dole? Find out by accessing our full research report, it’s free.

Known for its delicious pineapples and Hawaiian roots, Dole (NYSE:DOLE) is a global agricultural company specializing in fresh fruits and vegetables.

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $9.17 billion in revenue over the past 12 months, Dole is one of the larger consumer staples companies and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because there are only a finite number of major retail partners, placing a ceiling on its growth. To expand meaningfully, Dole likely needs to tweak its prices, innovate with new products, or enter new markets.

As you can see below, Dole’s 2% annualized revenue growth over the last three years was sluggish. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

This quarter, Dole reported year-on-year revenue growth of 9.2%, and its $2.37 billion of revenue exceeded Wall Street’s estimates by 2.3%.

Looking ahead, sell-side analysts expect revenue to grow 1.3% over the next 12 months, similar to its three-year rate. This projection is underwhelming and indicates its newer products will not catalyze better top-line performance yet.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

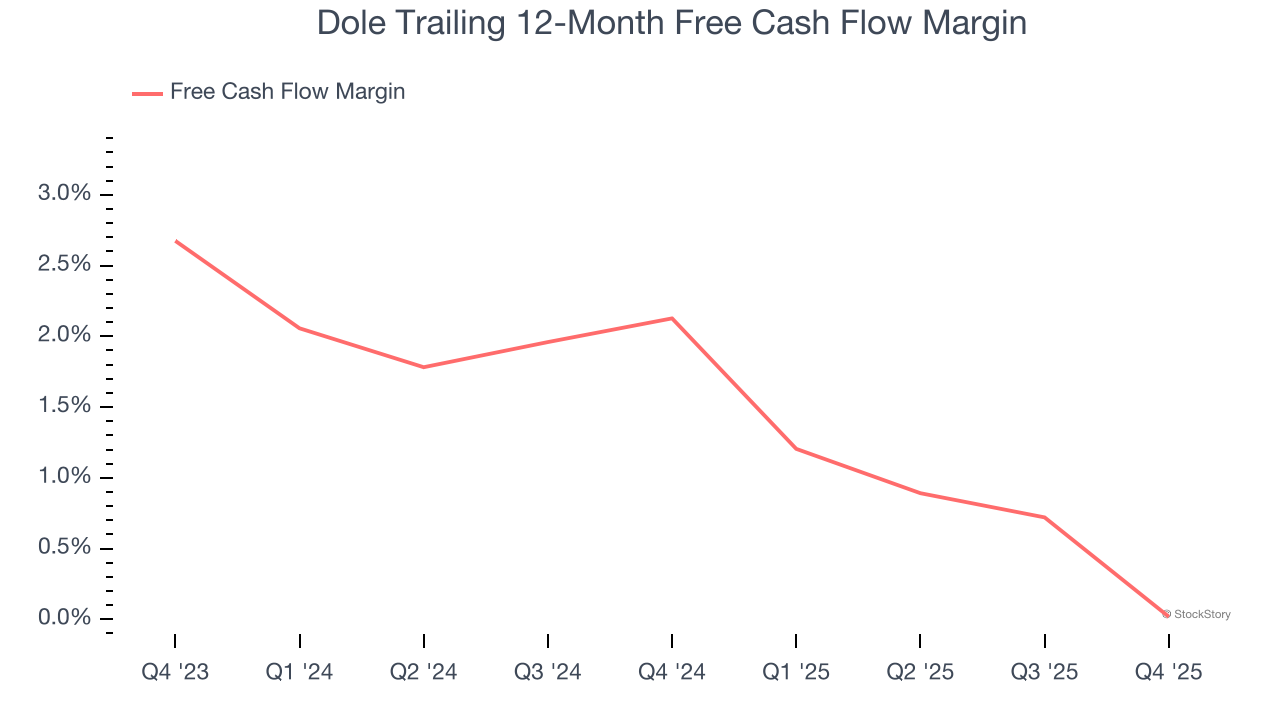

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Dole has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 1%, subpar for a consumer staples business.

Taking a step back, we can see that Dole’s margin dropped by 2.1 percentage points over the last year. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the trend continues, it could signal it’s becoming a more capital-intensive business.

Dole’s free cash flow clocked in at $67.87 million in Q4, equivalent to a 2.9% margin. The company’s cash profitability regressed as it was 3.2 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t put too much weight on this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends carry greater meaning.

We enjoyed seeing Dole beat analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its gross margin missed and its EPS was in line with Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $15.91 immediately after reporting.

Is Dole an attractive investment opportunity at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-20 | |

| Jul-02 | |

| Jul-01 | |

| Jun-25 | |

| Jun-23 | |

| May-14 | |

| May-12 | |

| May-11 | |

| May-11 | |

| May-11 | |

| Apr-27 | |

| Apr-20 | |

| Apr-07 | |

| Mar-10 | |

| Mar-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite