|

|

|

|

|||||

|

|

|

Escalating global tensions, particularly in parts of Europe and the Middle East, have heightened national security risks and prompted many governments to increase their defense budgets. As a result, the United States and its allies are increasing military expenditures to enhance preparedness, upgrade aging systems, and accelerate the development of advanced defense capabilities.

In January 2026, U.S. President Donald Trump proposed a significant increase in U.S. defense spending, targeting annual military outlays of about $1.5 trillion by 2027, up from the roughly $901 billion defense budget approved for fiscal 2026. This surge in spending supports leading contractors like Lockheed Martin LMT and Kratos Defense & Security Solutions KTOS, driving higher revenues through expanded procurement orders and long-term modernization initiatives.

Both companies benefit from rising Pentagon spending on advanced aerospace and defense technologies. Lockheed Martin is a large, established defense prime that innovates through massive, long-term programs like fighter jets, missile systems, and space defense platforms, emphasizing scale, integration and reliability. Kratos Defense, on the other hand, is a smaller, more agile company focused on emerging technologies, such as unmanned systems, drones, and hypersonic testing, aiming to deliver faster and lower-cost solutions.

Let's compare the stocks' fundamentals to determine which one is a better investment option at present.

Lockheed Martin is one of the largest U.S. defense contractors with a platform-centric focus that guarantees a steady inflow of follow-on orders from its leveraged presence in the Army, Air Force, Navy and IT programs. The F-35 program remains a key growth driver for the company’s Aeronautics segment, accounting for nearly 27% of LMT’s total consolidated net sales in 2025. The company has delivered 1,293 F-35 airplanes since the program's inception, with 368 jets in the backlog as of Dec. 31, 2025. This surely boosts expectation for the Aeronautics business segment’s sales, which improved 6.4% year over year in the fourth quarter of 2025.

The increase in the budget proposal suggests a stronger long-term funding outlook for defense programs, including missile defense, advanced weapons and space-related initiatives. Given Lockheed Martin’s leading position in these areas, higher and sustained defense spending could improve order visibility and support steady revenue growth for the company over time.

Kratos Defense is the primary provider of unmanned aerial target drone systems to the U.S. Air Force, Navy, Army and several allied defense agencies, leading to multiple recent contracts and partnerships that are expanding its presence in the global UAS market. During the fourth quarter of 2025, its Unmanned Systems segment generated $68.5 million of revenues compared with $61.1 million in the year-ago quarter.

The company significantly benefits from Pentagon demand. The U.S. Department of Defense is shifting toward modern, autonomous, and relatively low-cost technologies to upgrade its military, rather than relying only on traditional, expensive platforms. Kratos Defense benefits from this shift because it specializes in innovative and affordable systems. Key wins, including the Valkyrie drone moving into production and major hypersonic testing contracts, are drawing substantial government funding and supporting strong revenue growth.

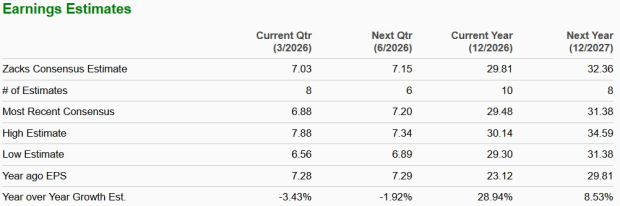

The Zacks Consensus Estimate for Lockheed Martin’s 2026 and 2027 earnings per share (EPS) indicates an increase of 28.94% and 8.53%, respectively, year over year.

The Zacks Consensus Estimate for Kratos Defense’s 2026 and 2027 EPS indicates an increase of 32.73% and 47.52%, respectively, year over year.

Lockheed Martin’s shares trade at a forward 12-month Price/Sales (P/S F12M) of 1.94X compared with Kratos Defense’s 9.35X.

Currently, total debt to capital for Kratos Defense is nil, while that for Lockheed Martin is 76.35%.

The time-to-interest earned ratio for Kratos Defense and Lockheed Martin is 11.8 and 6.3, respectively. The ratio, being greater than one, reflects the company’s ability to meet future interest obligations without difficulties.

In the past year, shares of Lockheed Martin and Kratos Defense have risen 50.5% and 263.3%, respectively.

Lockheed Martin benefits from its strong platform presence across U.S. military programs and a solid backlog supporting Aeronautics growth. Rising defense budget proposals further strengthen long-term funding prospects for missile defense, advanced weapons and space programs, supporting steady revenue visibility and future growth. Kratos Defense is expanding its global unmanned systems presence. Strong Pentagon demand for affordable, autonomous technologies is driving funding momentum and supporting continued revenue growth.

However, our choice at the moment is Kratos Defense, given its better earnings growth, better debt management and price performance than Lockheed Martin. KTOS has a Zacks Rank #2 (Buy) and LMT carries a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-25 | |

| Jul-25 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite