|

|

|

|

|||||

|

|

|

JPMorgan JPM continues to frame technology as a core, multi-year competitive investment rather than a discretionary cost lever. Management expects approximately $19.8 billion of technology spend in 2026, up 10% year over year. This will be driven by business growth and demand for new products/capabilities, with key cost pressures, including inflation and higher hardware costs amid AI-related chip/memory shortages, plus higher infrastructure (including public cloud) and software costs tied to volume/feature demand.

Incremental funding for major projects alongside identified efficiencies (including AI-related efficiencies) that help “self-fund” additional investment remain key tech spending reason. While JPM is “past peak modernization” in infrastructure, modernization continues, shifting from data-center/infrastructure modernization toward modernizing application code and data, explicitly to be positioned to benefit from AI and other innovations.

JPM’s 2026 Tech Spending

On AI specifically, JPMorgan is generating tangible benefits. Traditional ML/analytical AI has long improved outcomes in areas like marketing and fraud detection, while generative AI is a fast-growing share of activity. In 2025, the company doubled AI use cases in production, focusing on high-impact domains such as customer service (call-center efficiency), personalized client insights and developer productivity for software engineers. By adopting its internal GenAI tooling (“LLM suite”), its employees have moved from experimentation to secure API-based integration of GenAI into business applications and workflows.

Additionally, JPMorgan is leveraging a modernized tech foundation. The company is positioning AI benefits to accrue to customers through better experiences, new value propositions and streamlined middle/back-office processes, supported by an extensive data estate.

Beyond AI, JPM’s ongoing platform build-outs and innovation in areas like blockchain and tokenization (e.g., tokenized deposits and related digital-ledger capabilities) are part of the broader technology agenda to support payments, custody and client solutions over time.

Net Interest Income (NII) Trajectory: Following a decent 2025 NII performance, JPMorgan expects the momentum to continue this year. In 2025, the Federal Reserve lowered interest rates by 75 basis points (bps), following a 50-bp cut in 2024. Despite this, the bank reported a 3% rise in 2025 NII, driven by 11% loan growth and lower funding costs.

Building on this, JPMorgan now expects NII for 2026 to be approximately $104.5 billion, or up 9% year over year. It assumes two rate cuts, interest on reserve balance (IORB) falling about 83 bps year over year and deposit margin compression as headwinds. To counter that, the company points to modest improvement in Consumer and Wholesale deposit balances. Higher-yielding revolving card balances are expected to help cushion NII as benchmark rates drift lower, particularly if funding costs stay contained.

Part of the lift is likely to come from Markets NII. JPM has pegged 2026 NII, excluding Markets, at roughly $95 billion, implying Markets NII of around $9.5 billion (up from $3.3 billion in 2025).

2026 NII Expectation

Bank of America BAC expects 2026 NII to rise 5-7% year over year, following 7% increase in 2025. The company continues to benefit from a supportive rate backdrop, productivity gains from technology investments and the earnings resilience of a diversified franchise. Also, Citigroup C guides 5-6% NII growth for 2026, after delivering 11% year-over-year growth in 2025. The bank’s outlook is underpinned by a steadier rate environment and constructive balance sheet trends.

Coming back to JPMorgan, on Jan. 7, it signed an agreement to become the new issuer of the Apple Card, which has approximately $20 billion in receivables. While the deal will strengthen the bank’s position in the credit card operation, the phased transition (expected to be over in two years and subject to regulatory approvals) is unlikely to impact the company’s NII this year to a great extent.

Moreover, with Markets expected to contribute meaningfully to drive NII in 2026, the path will hinge on interest rates, deposit competition and trading-related balance sheet dynamics.

Fee Income to Witness More Upside From Lower Rates: Easier monetary policy will lift client activity, deal flow and asset values, supporting a broad rebound in JPMorgan’s non-interest income. Lower borrowing costs are expected to encourage corporate financing, including debt issuance, M&A and equity offerings, extending the recovery in capital markets after a subdued 2022-2023. JPMorgan’s leading investment banking franchise (ranked #1 globally with an estimated 8.4% wallet share in 2025) positions it to capture a larger share of advisory and underwriting fees as conditions become more supportive, though macroeconomic and geopolitical uncertainty remains a key risk.

Rate transitions have heightened volatility in fixed income, currencies and commodities, thus boosting client hedging and trading activity. With a top-tier trading platform, JPMorgan is positioned to benefit from stronger FICC and equities volumes as investors reposition for a lower-rate environment, even as trading activity normalizes over time.

In wealth and asset management, declining yields often shift investor preferences toward equities and alternatives, helping drive market appreciation, inflows and higher fees. Improved sentiment should support growth in assets under management and fee revenues across JPMorgan’s private banking and wealth platforms. As such, the company expects a broad-based improvement in fee income in the quarters ahead.

Branch Openings & Opportunistic Acquisitions: With 5,083 branches as of Dec. 31, 2025, more than any other U.S. bank and a presence in all 48 contiguous states, JPM continues to invest in brick-and-mortar to strengthen its competitive edge in relationship banking, despite the digital shift. JPMorgan plans to add 500 more by 2027, and as part of this plan, in 2026, it will open more than 160 branches across 30 states and renovate nearly 600 locations. These efforts will deepen relationships and boost cross-selling across mortgages, loans, investments and credit cards.

JPMorgan isn’t alone in branch expansion. Bank of America is growing its financial center network, with plans to open 150 more centers by 2027, despite most interactions being digital.

Additionally, JPMorgan has expanded through strategic acquisitions, including a larger stake in Brazil’s C6 Bank, partnerships with Cleareye.ai and Aumni, and the 2023 purchase of First Republic Bank. These moves boosted profits and supported its strategy to diversify revenues and grow digital and fee-based offerings.

Fortress Balance Sheet and Solid Liquidity: As of Dec. 31, 2025, JPM had a total debt of $500 billion (the majority of this is long-term in nature). The company's cash and due from banks and deposits with banks were $343.3 billion on the same date. The company maintains long-term issuer ratings A-/AA-/A1 from Standard and Poor’s, Fitch Ratings and Moody’s Investors Service, respectively.

Hence, JPMorgan continues to reward shareholders handsomely. It cleared the 2025 stress test impressively and announced an increase in its quarterly dividend by 7% to $1.50 per share, as well as authorized a new share repurchase program worth $50 billion. As of Dec. 31, 2025, almost $33.8 billion in authorization remained available.

This was the second time that JPMorgan hiked its quarterly dividends in 2025. In March 2025, it raised its quarterly dividend by 12% to $1.40 per share. In the last five years, it hiked dividends six times, with an annualized growth rate of 10.05%.

Similar to JPM, Bank of America and Citigroup cleared the 2025 stress test. Following this, Bank of America raised its quarterly dividend 8% to 28 cents per share and authorized a new $40 billion share repurchase program. Citigroup also announced a dividend hike of 7% to 60 cents per share. It is continuing with the previously announced buyback plan, which had $6.8 billion worth of authorization remaining as of Dec. 31, 2025.

Asset Quality: Lower rates will likely support JPMorgan's asset quality, as declining rates will ease debt-service burdens and improve borrower solvency. The overall effect is expected to be moderate and vary by loan segment and macro conditions. Variable-rate consumer and leveraged corporate portfolios might see the most direct benefit, reflecting the lower risk of near-term credit losses as rates fall.

JPMorgan expects that lower rates will help stabilize or even modestly improve overall credit performance, especially in consumer and corporate loan books, as long as the U.S. economy remains resilient. Hence, JPMorgan expects the card service NCO rate to be roughly 3.4% “on favorable delinquency trends driven by the continued resilience of the consumer.”

In the past year, shares of JPMorgan have gained 14.9% compared with a 17.6% rise for the S&P 500 Index. Bank of America and Citigroup have gained 14.7% and 38.5%, respectively, in the same time frame.

One-Year Price Performance

JPMorgan stock currently trades at a premium to the industry. It is currently trading at a price-to-book (P/B) of 2.36X, slightly above the industry’s 2.32X. However, the company’s P/B ratio is lower than its high over the past five years, reflecting some level of undervalued trading compared with historical norms.

JPM’s P/B

If we compare JPMorgan’s current valuation with that of Bank of America and Citigroup, it appears expensive. At present, Bank of America has a P/B of 1.33X, while Citigroup is trading at a P/B of 1.01X.

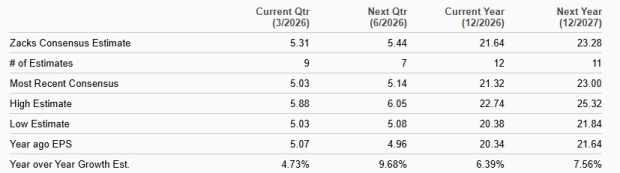

Analysts are bullish on JPMorgan’s prospects, with earnings estimates for 2026 and 2027 revised upward over the past week. The Zacks Consensus Estimate for JPM’s 2026 and 2027 earnings implies a 5.5% and 7.6% year-over-year increase, respectively.

Earnings Estimates

JPMorgan continues to project non-interest expenses of $105 billion this year, up more than 9% from 2025. Apart from 10% increase in tech spending, primary reasons for higher expenses include an increase in growth and volume-related spending (like compensation costs, costs for branching/expansion and costs related to credit card business growth), structural inflation-related costs and general operating overhead expenses.

Nonetheless, JPMorgan remains well-placed for growth backed by its robust capital markets business, dominant IB position, solid NII growth expectations and continued expansion through branch openings and strategic plans. The company’s size, diversification, track record and recent performance make it a reasonable core holding for a multi-year horizon.

However, you must keep an eye on interest-rate moves, developments across AI-usage in the banking sector, macroeconomic headwinds and the banking sector broadly because these could sway valuations and price movement more than the company’s individual performance. If you own this Zacks Rank #3 (Hold) stock, retain it, while others may wait for a better entry point. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 5 hours | |

| 9 hours | |

| 13 hours | |

| 19 hours | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite