|

|

|

|

|||||

|

|

|

Beam Therapeutics BEAM incurred a loss of 10 cents per share in the fourth quarter of 2025 (excluding gain on sale of equity method investment), narrower than the Zacks Consensus Estimate of a loss of $1.13. The company had reported a loss of $1.09 per share in the year-ago quarter.

Revenues totaled $114.1 million, beating the Zacks Consensus Estimate of $15 million. The company had recorded revenues of $30.1 million in the year-ago quarter. The top line primarily comprises license and collaboration revenues.

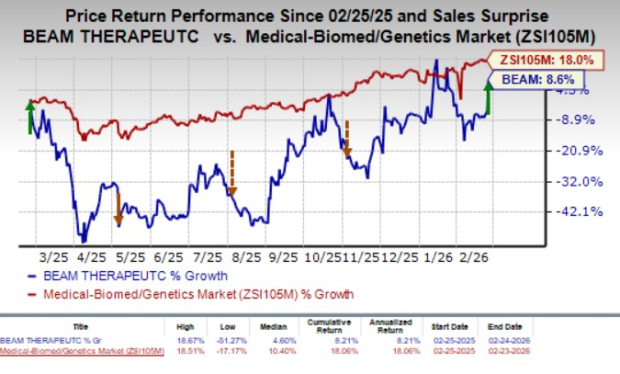

Over the past year, shares of Beam Therapeutics have gained 8.6% compared with the industry’s 18% rise.

Research and development expenses were $99.3 million in the fourth quarter, down 2.1% from the year-ago quarter.

General and administrative expenses surged 12.6% year over year to $32.3 million.

As of Dec. 31, 2025, Beam Therapeutics had cash, cash equivalents and marketable securities worth $1.25 billion compared with $1.1 billion as of Sept. 30, 2025.

In a separate press release, BEAM announced that it has secured a $500 million non-dilutive senior credit facility from Sixth Street to fund the potential launch of ristoglogene autogetemcel (risto-cel) in sickle cell disease (SCD). The deal includes $100 million upfront payment, up to $300 million tied to clinical, regulatory and commercial milestones and an optional $100 million tranche over a seven-year term. The financing extends BEAM’s cash runway into mid-2029.

For 2025, Beam Therapeutics reported total revenues of $139.7 million, representing a sharp increase of 120% year over year.

Beam Therapeutics is developing its leading ex-vivo genome-editing candidate, risto-cel, in the phase I/II BEACON study for the treatment of patients with SCD, an inherited blood disorder.

The company presented updated data from the BEACON study in December 2025, which continued to show evidence of risto-cel’s differentiated treatment profile in SCD patients. BEAM plans to submit a biologics licensing application (BLA) for risto-cel by the end of 2026.

Beam Therapeutics is also expanding its genetic disease pipeline by developing BEAM-301 and BEAM-302 for the treatment of glycogen storage disease type 1a (GSD1a) and alpha-1 antitrypsin deficiency (AATD), respectively.

Dosing has been completed in the first cohort of the phase I/II study, evaluating BEAM-301 as a potential treatment for patients with GSDIa in the United States. Enrollment is now underway in the second cohort. Initial data from the study are expected in 2026.

The company is developing BEAM-302 in a phase I/II dose-escalation study for treating AATD. BEAM has aligned with the FDA on a potential accelerated approval pathway based on 12-month AAT biomarker data and plans to enroll about 50 additional patients at the selected optimal dose to support a future BLA submission.

Dosing in the ongoing phase I healthy volunteer study, evaluating BEAM-103, an anti-CD117 monoclonal antibody for treating SCD, is expected to be completed in the first half of 2026.

The company expanded its liver-targeted genetic disease franchise with BEAM-304 for the treatment of phenylketonuria (PKU) and plans to file an investigational new drug application with the FDA in 2026. PKU is a rare, inherited metabolic disorder that results in the toxic accumulation of phenylalanine, which can lead to serious neurologic and neurocognitive impairments.

Beam Therapeutics Inc. price-consensus-eps-surprise-chart | Beam Therapeutics Inc. Quote

Beam Therapeutics currently carries a Zacks Rank #4 (Sell).

Some better-ranked stocks in the biotech sector are Harmony Biosciences HRMY, Assertio Holdings ASRT and Castle Biosciences CSTL, each currently sporting a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Over the past 60 days, estimates for Harmony Biosciences’ 2026 earnings per share have risen from $3.72 to $4.00. HRMY shares have lost 23.7% over the past year.

Harmony Biosciences’ earnings beat estimates in two of the trailing four quarters but missed in the remaining two, with the average surprise being 7.20%.

Over the past 60 days, estimates for Assertio’s 2026 loss per share have narrowed from 30 cents to 28 cents. ASRT shares have gained 1.6% over the past year.

Assertio’s earnings beat estimates in one of the trailing four quarters and missed in the remaining three, with the average negative surprise being 35.21%.

Over the past 60 days, estimates for Castle Biosciences’ 2026 loss per share have narrowed from $1.06 to 96 cents. CSTL shares have risen 19.5% over the past year.

Castle Biosciences’ earnings beat estimates in three of the trailing four quarters and missed in the remaining one, with the average surprise being 66.11%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-06 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-27 | |

| Jul-23 | |

| Jul-22 | |

| Jul-21 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite