|

|

|

|

|||||

|

|

|

Shares of Bank of Hawaii Corporation BOH have gained 15.7% in the past three months, outperforming the industry’s 6.2% growth and the S&P 500 Index’s 0.2% rise.

Further, the bank’s price performance has been better than that of its peers, Heritage Commerce Corp HTBK and Columbia Banking System, Inc. COLB. Shares of Heritage Commerce and Columbia Banking have gained 15.3% and 5.3%, respectively, in the same time frame.

Over the past 30 days, the company’s Zacks Consensus Estimate for 2026 and 2027 earnings has been revised upward.

The Zacks Consensus Estimate for BOH’s 2026 and 2027 earnings indicates a 27.4% and 9.8% rise, respectively. This suggests that analysts are more optimistic about the company’s future earnings.

Despite recent price strength and a strong earnings outlook, investors may wonder if Bank of Hawaii has more upside. Let’s examine its fundamentals and growth prospects to assess its investment appeal.

Strong Balance Sheet Position: Bank of Hawaii maintains a solid and well-managed balance sheet, supported by a stable deposit base and prudent loan portfolio. Over the seven years ended 2025, deposits recorded a compound annual growth rate (CAGR) of 5%, while net loans and leases grew at a CAGR of 4.4%.

The company’s diversified, long-duration deposit base, along with lower-risk loan assets, positions it to remain stable even amid changing interest-rate environments. A balanced asset mix and ongoing fixed-asset repricing further enhance resilience, with 2025 rate-sensitive assets of $7 billion and rate-sensitive interest-bearing liabilities of $10.4 billion. Looking ahead, loans are expected to grow in the mid-single-digit range in 2026, supporting continued asset expansion without compromising financial strength.

Overall, BOH’s strong balance sheet and prudent asset-liability management are likely to sustain stability and support future growth in net loans and deposits.

Low Funding Cost to Aid NII: Bank of Hawaii’s net interest income (NII) has shown steady growth, reflecting prudent balance sheet management and disciplined asset-liability strategies. Over the seven years ended 2025, the company’s NII recorded a CAGR of 1.3%. Notably, both NII and net interest margin (NIM) have expanded for the seventh consecutive quarter.

Looking ahead, both metrics are expected to rise in 2026, supported by ongoing asset cash-flow repricing and an improving deposit mix. Following 175 basis points of Federal Open Market Committee rate cuts from September 2024 through December 2025, interest-bearing liabilities have continued to decline, easing funding cost and supporting NII growth. Management expects NII momentum to strengthen further over the next one to two quarters as these factors take effect.

Thus, the bank is well-positioned to sustain NII growth, with balance sheet initiatives and favorable funding conditions driving continued improvement in net interest margins.

Fee Income Growth: BOH is well-positioned to benefit from steady growth in fee-based businesses. Over the seven years ended 2025, non-interest income recorded a CAGR of nearly 1%, reflecting consistent contributions from its diversified fee sources.

Going forward, the metric is expected to rise further, supported by ongoing strength in trust services, merchant services, and other transaction-related revenues. The steady expansion in these areas, combined with broadening client activity, is likely to provide additional support to the company’s overall revenue growth. The bank’s diversified offerings and stable transaction volumes will continue to drive fee income momentum.

Strategic Partnerships & Digital Expansion: The bank has been strengthening its wealth management and digital capabilities through key partnerships and technology investments.

In March 2025, the bank partnered with Cetera Financial Institutions to expand its $2.5 billion investment services program. Under the agreement, its investment services and insurance provider, Bankoh Investment Services, Inc. (“BISI”) was rebranded as Bankoh Advisors, offering clients a modernized experience with enhanced technology and additional resources while continuing to deliver personalized financial advice locally in Hawaii.

Earlier, in 2021, BOH selected FIS Digital One to modernize its digital and mobile banking platforms. This initiative enables more personalized online and mobile experiences, faster integration with fintech solutions, and supports the bank’s long-term goal of delivering seamless, client-focused digital services.

Solid Liquidity Position to Support Capital Distribution: The company maintains a healthy liquidity position. As of Dec. 31, 2025, total liquidity amounted to $946.5 million, comfortably exceeding total debt of $608.2 million, which includes securities sold under agreements to repurchase and other borrowings. This strong liquidity provides the bank with the flexibility to meet obligations even under challenging economic conditions.

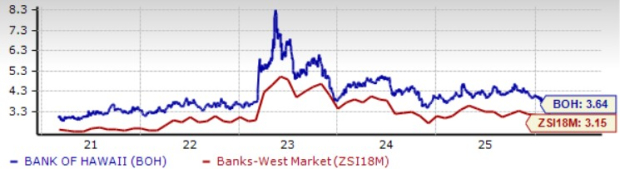

Bank of Hawaii continues to enhance shareholder value through dividends and share repurchases. In July 2021, it increased its quarterly dividend by 4.5% to 70 cents per share and has maintained it since. Over the past five years, the company has raised its dividend once, delivering an annualized dividend growth rate of 0.48%. Its current dividend yield stands at an attractive 3.64%, above the industry average of 3.15%. Meanwhile, the dividend yield of its peers, Columbia Banking and Heritage Commerce, are 4.96% and 4.10%, respectively.

Beyond dividends, BOH also maintains an active share repurchase program. In January 2023, the board approved a $100 million common stock buyback plan with no expiration, replacing the original 2001 authorization. As of Dec. 31, 2025, $121 million remained available under the program. The bank’s solid capital base and consistent income generation support ongoing capital distribution initiatives, positioning it well to return value to shareholders.

Elevated Expense Base: Over the last seven years (2018–2025), the bank’s non-interest expenses grew at a CAGR of 2.6%. The rise has been primarily driven by investments in technology and innovation, as well as higher incentive-related and other variable expenses. Management expects the bank’s core expenses to remain elevated, with an anticipated increase of 3–3.5% in 2026.

Geographic Loan Concentration Risk: A significant portion of BOH’s loan portfolio is concentrated in the Hawaii region. As of Dec. 31, 2025, 93% of total loans were in Hawaii, while the remaining 4% and 3% were in the Western Pacific and Mainland, respectively.

This high regional concentration makes the bank vulnerable to potential economic or political slowdowns in Hawaii. Any prolonged downturn in the local economy could weigh on loan performance and financial results, highlighting the risks associated with limited geographic diversification.

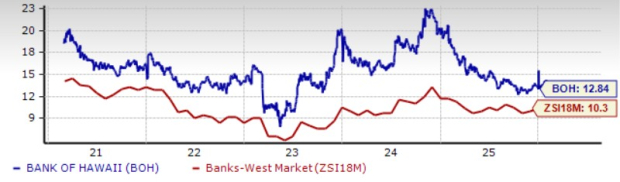

In terms of valuation, BOH stock appears expensive relative to the industry. The company is currently trading at a 12-month trailing price-to-earnings (P/E) ratio of 12.84X, which is higher than the industry’s 10.30X.

Meanwhile, Columbia Banking holds a P/E ratio of 9.65X, while Heritage Commerce’s P/E ratio stands at 12.73X.

While elevated operating expenses, geographic loan concentration and a premium valuation warrant some caution in the near term, these risks appear manageable given Bank of Hawaii’s resilient balance sheet and strong earnings outlook.

The consistent loan and deposit growth, expanding NII, and upward revisions of 2026 and 2027 earnings estimates reflect that the bank is benefiting from a favorable and easing interest-rate environment. Strategic partnerships in wealth management and digital banking, along with disciplined capital returns through dividends and share repurchases, further strengthen BOH’s long-term growth narrative.

Overall, Bank of Hawaii stands out as a compelling choice for investors seeking exposure to a well-run, growth-oriented regional bank with improving fundamentals and shareholder-friendly policies.

BOH currently carries a Zacks Rank #2 (Buy). You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-15 | |

| Jul-06 | |

| Jul-02 | |

| Jun-30 | |

| Jun-25 | |

| May-15 | |

| Apr-30 | |

| Apr-24 | |

| Apr-24 | |

| Apr-23 | |

| Apr-23 | |

| Apr-22 | |

| Apr-21 | |

| Apr-20 | |

| Apr-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite