|

|

|

|

|||||

|

|

|

The end of the earnings season is always a good time to take a step back and see who shined (and who not so much). Let’s take a look at how data & business process services stocks fared in Q4, starting with Equifax (NYSE:EFX).

A combination of increasing reliance on data and analytics across various industries and the desire for cost efficiency through outsourcing could mean that companies in this space gain. As functions such as payroll, HR, and credit risk assessment rely on more digitization, key players in the data & business process services industry could be increased demand. On the other hand, the sector faces headwinds from growing regulatory scrutiny on data privacy and security, with laws like GDPR and evolving U.S. regulations potentially limiting data collection and monetization strategies. Additionally, rising cyber threats pose risks to firms handling sensitive personal and financial information, creating outsized headline risk when things go wrong in this area.

The 9 data & business process services stocks we track reported a satisfactory Q4. As a group, revenues beat analysts’ consensus estimates by 2.1% while next quarter’s revenue guidance was in line.

While some data & business process services stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 2.7% since the latest earnings results.

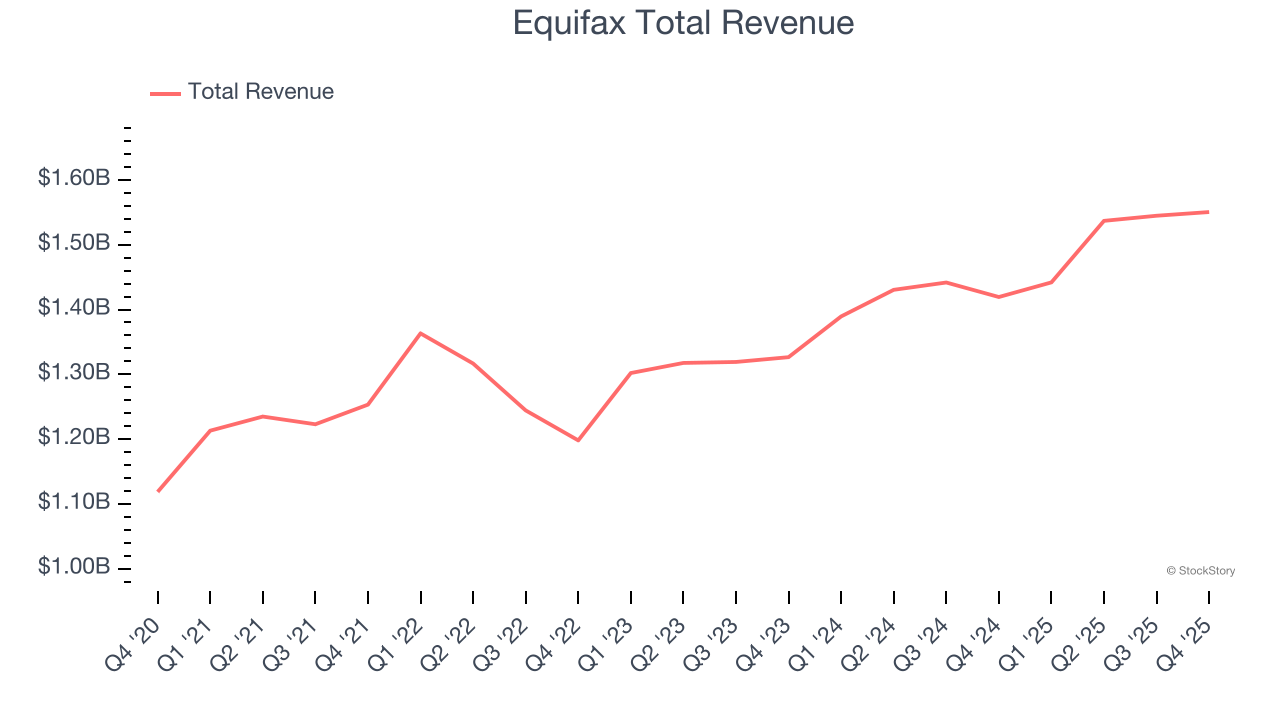

Holding detailed financial records on over 800 million consumers worldwide and dating back to 1899, Equifax (NYSE:EFX) is a global data analytics company that collects, analyzes, and sells consumer and business credit information to lenders, employers, and other businesses.

Equifax reported revenues of $1.55 billion, up 9.2% year on year. This print exceeded analysts’ expectations by 1.4%. Despite the top-line beat, it was still a mixed quarter for the company with revenue guidance for next quarter exceeding analysts’ expectations but a significant miss of analysts’ EPS guidance for next quarter estimates.

"Equifax delivered strong fourth quarter revenue of $1.551 billion, up 9% on both a reported and local currency basis, that was $30 million above the midpoint of our October guidance. This was led by strong 20% U.S. Mortgage revenue growth, strong Workforce Solutions Government revenue growth, and continued momentum in New Product Innovation with a Vitality Index of 17% despite headwinds from the U.S. Mortgage and Hiring markets. Workforce Solutions delivered 9% revenue growth, driven by Verification Services revenue growth of 10% led by Diversified Markets revenue growth of 11% from strong low double digit growth in Government and mid double digit growth in Consumer Lending businesses. USIS delivered strong revenue growth of 12%, well above their 6 to 8% Long Term Financial Framework. USIS revenue growth was led by very strong 33% Mortgage revenue growth and Diversified Markets revenue growth of 5%. International delivered 5% local currency revenue growth led by Latin America. We were pleased with the strong Equifax results in a challenging market environment and momentum into 2026 from our fourth quarter results," said Mark W. Begor, Equifax Chief Executive Officer.

Interestingly, the stock is up 12.3% since reporting and currently trades at $196.59.

Is now the time to buy Equifax? Access our full analysis of the earnings results here, it’s free.

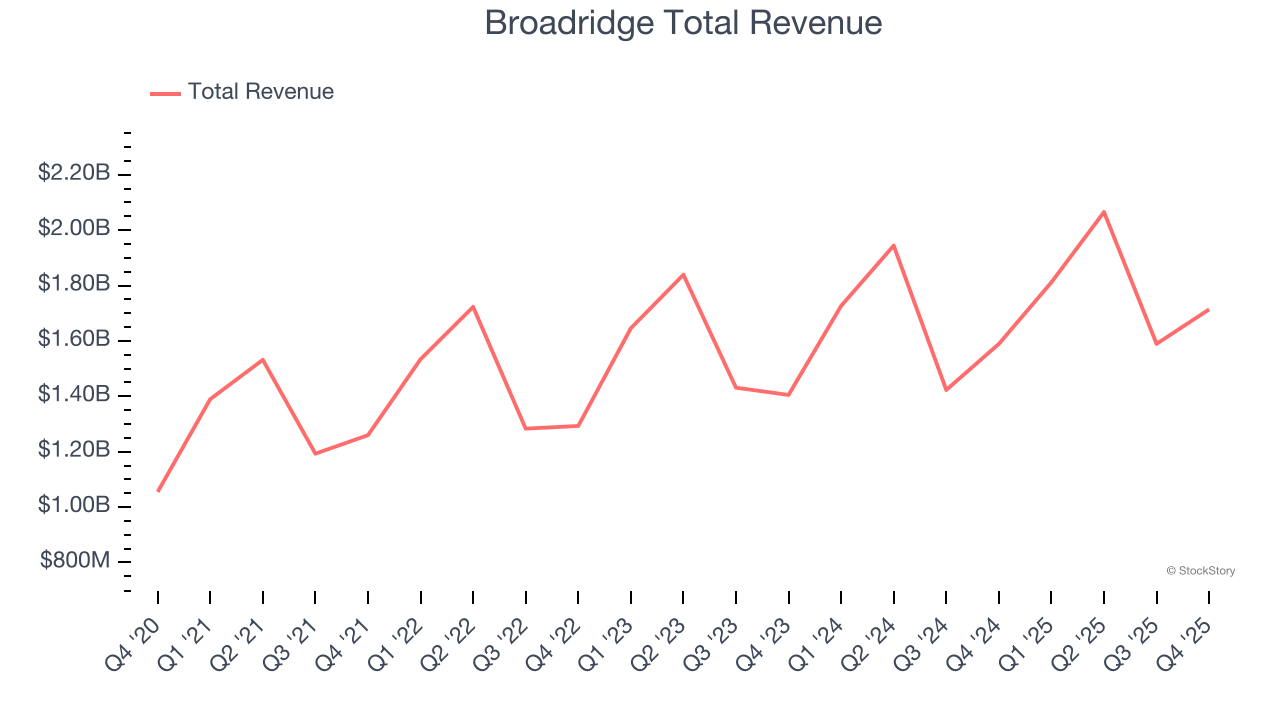

Processing over $10 trillion in equity and fixed income trades daily and managing proxy voting for over 800 million equity positions, Broadridge Financial Solutions (NYSE:BR) provides technology-driven solutions that power investing, governance, and communications for banks, broker-dealers, asset managers, and public companies.

Broadridge reported revenues of $1.71 billion, up 7.8% year on year, outperforming analysts’ expectations by 6.5%. The business had an incredible quarter with a beat of analysts’ EPS estimates and a solid beat of analysts’ revenue estimates.

Broadridge scored the biggest analyst estimates beat among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 10.1% since reporting. It currently trades at $178.30.

Is now the time to buy Broadridge? Access our full analysis of the earnings results here, it’s free.

Processing over 2.8 billion insurance transaction records annually through one of the world's largest private databases, Verisk Analytics (NASDAQ:VRSK) provides data, analytics, and technology solutions that help insurance companies assess risk, detect fraud, and make better business decisions.

Verisk reported revenues of $778.8 million, up 5.9% year on year, exceeding analysts’ expectations by 0.7%. Still, it was a mixed quarter as it posted full-year revenue guidance missing analysts’ expectations.

Verisk delivered the slowest revenue growth in the group. Interestingly, the stock is up 10.5% since the results and currently trades at $195.84.

Read our full analysis of Verisk’s results here.

Founded in 1986 as a bridge between technology and financial services, SS&C Technologies (NASDAQ:SSNC) provides software and software-enabled services that help financial firms and healthcare organizations automate complex business processes.

SS&C reported revenues of $1.65 billion, up 8.1% year on year. This result beat analysts’ expectations by 1.9%. It was a very strong quarter as it also put up an impressive beat of analysts’ full-year EPS guidance estimates and full-year revenue guidance topping analysts’ expectations.

SS&C achieved the highest full-year guidance raise among its peers. The stock is down 1.9% since reporting and currently trades at $73.57.

Read our full, actionable report on SS&C here, it’s free.

With a research department that makes over 10,000 property updates daily to its 35-year-old database, CoStar Group (NASDAQ:CSGP) provides comprehensive real estate data, analytics, and online marketplaces for commercial and residential properties in the U.S. and U.K.

CoStar reported revenues of $900 million, up 26.9% year on year. This number topped analysts’ expectations by 0.9%. However, it was a slower quarter as it logged a significant miss of analysts’ full-year EPS guidance estimates and a significant miss of analysts’ EPS guidance for next quarter estimates.

CoStar scored the fastest revenue growth among its peers. The stock is down 9.3% since reporting and currently trades at $44.59.

Read our full, actionable report on CoStar here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.

| Jul-30 |

Equifax 'duplicate collection account' class-action settlement: Who qualifies

EFX -5.84%

Yahoo Personal Finance

|

| Jul-30 | |

| Jul-29 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-09 | |

| Jul-08 | |

| Jul-07 | |

| Jul-07 | |

| Jul-06 | |

| Jul-01 | |

| Jun-30 | |

| Jun-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite