|

|

|

|

|||||

|

|

|

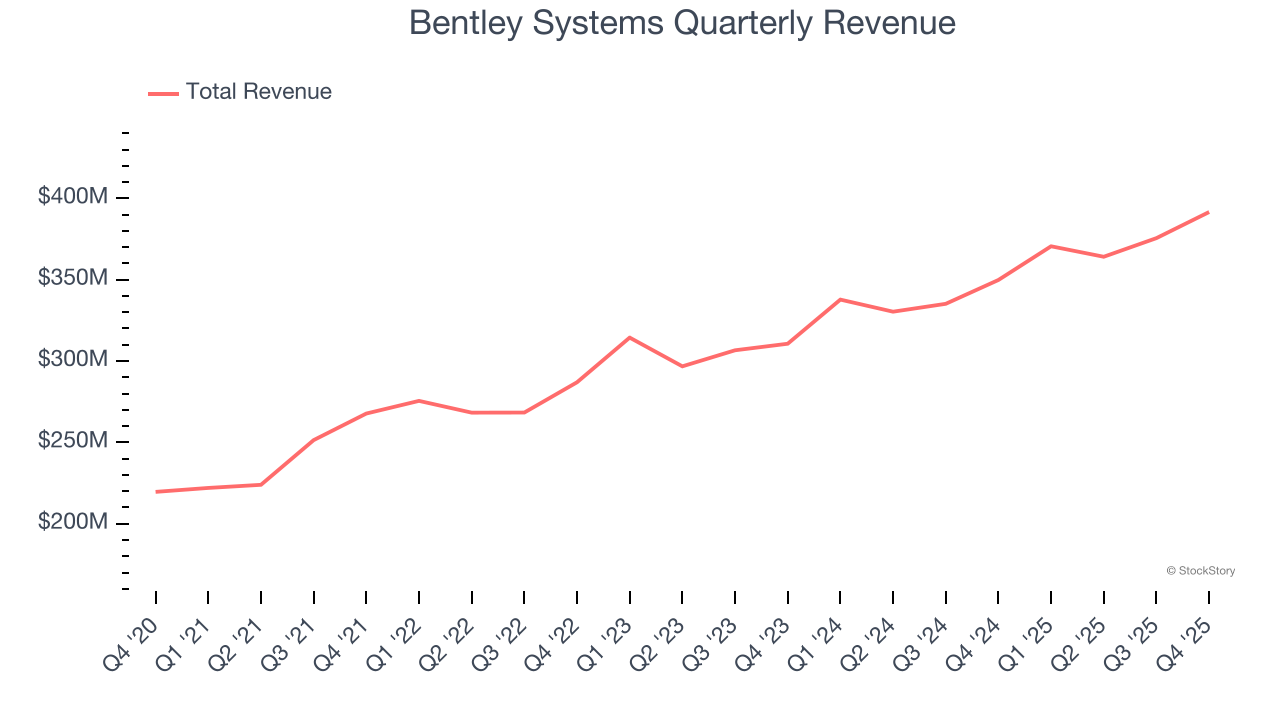

Infrastructure engineering software company Bentley Systems (NASDAQ:BSY) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 11.9% year on year to $391.6 million. The company’s full-year revenue guidance of $1.7 billion at the midpoint came in 3.2% above analysts’ estimates. Its non-GAAP profit of $0.27 per share was in line with analysts’ consensus estimates.

Is now the time to buy Bentley Systems? Find out by accessing our full research report, it’s free.

CEO Nicholas Cumins said, “We delivered a strong finish to the year, giving us great momentum for our 2026 outlook, and I want to thank our colleagues for their outstanding dedication and our users for their continued partnership. The standout growth of our Seequent business continues to successfully expand our addressable market into critical resources. In parallel, we are building momentum in AI, from the growing commercial traction of Bentley Asset Analytics in operations, to our strategic push in the foundational area of AI in design—where we see enormous potential and are building the market to secure long-term leadership.”

Pioneering the concept of "digital twins" for infrastructure projects long before it became an industry buzzword, Bentley Systems (NASDAQ:BSY) provides software solutions that help engineers design, build, and operate infrastructure projects across sectors including roads, bridges, utilities, mining, and industrial facilities.

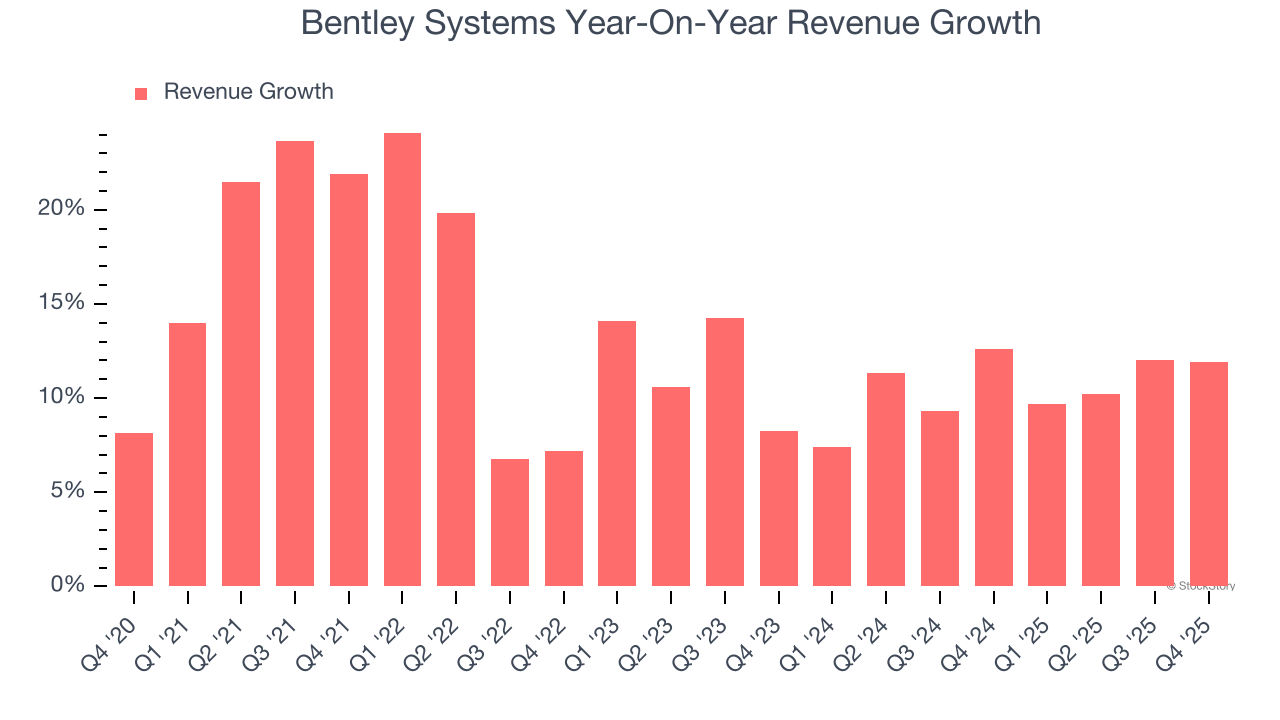

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Bentley Systems grew its sales at a 13.4% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the software sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Bentley Systems’s recent performance shows its demand has slowed as its annualized revenue growth of 10.6% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Bentley Systems reported year-on-year revenue growth of 11.9%, and its $391.6 million of revenue exceeded Wall Street’s estimates by 2.7%.

Looking ahead, sell-side analysts expect revenue to grow 9.6% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and suggests its products and services will face some demand challenges.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

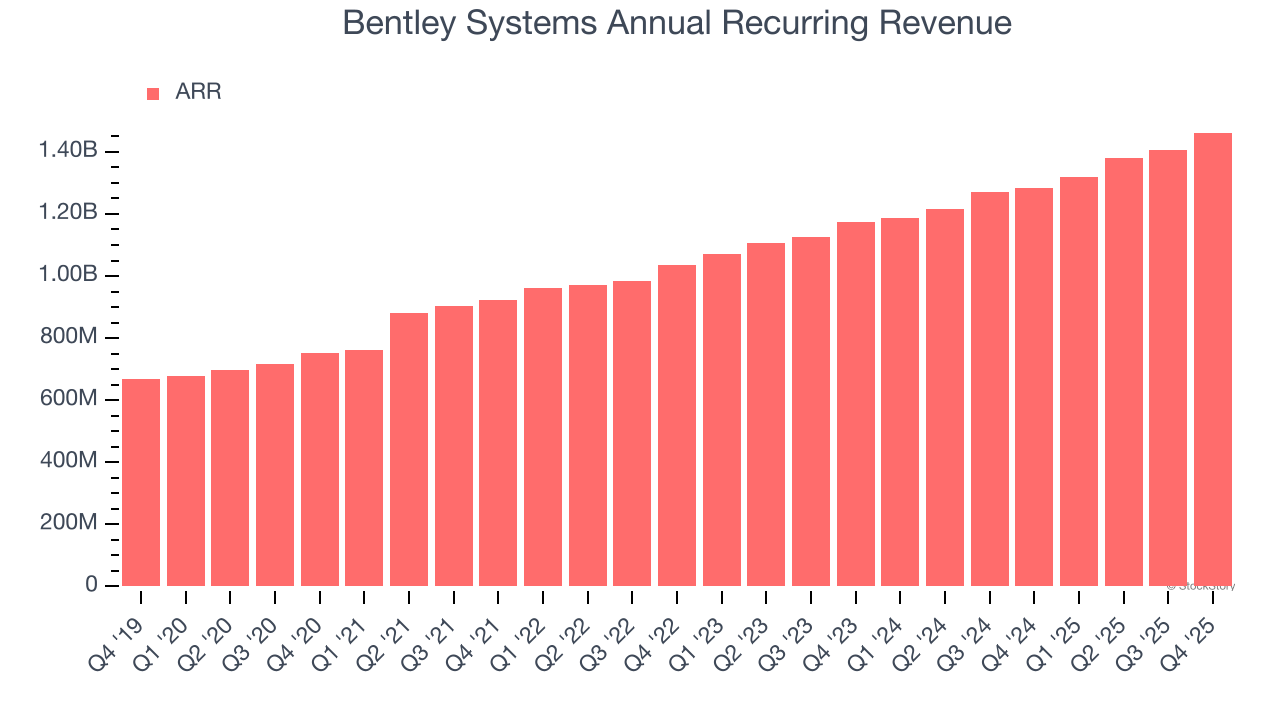

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Bentley Systems’s ARR came in at $1.46 billion in Q4, and over the last four quarters, its growth was underwhelming as it averaged 12.3% year-on-year increases. This performance mirrored its total sales and suggests that increasing competition is causing challenges in securing longer-term commitments.

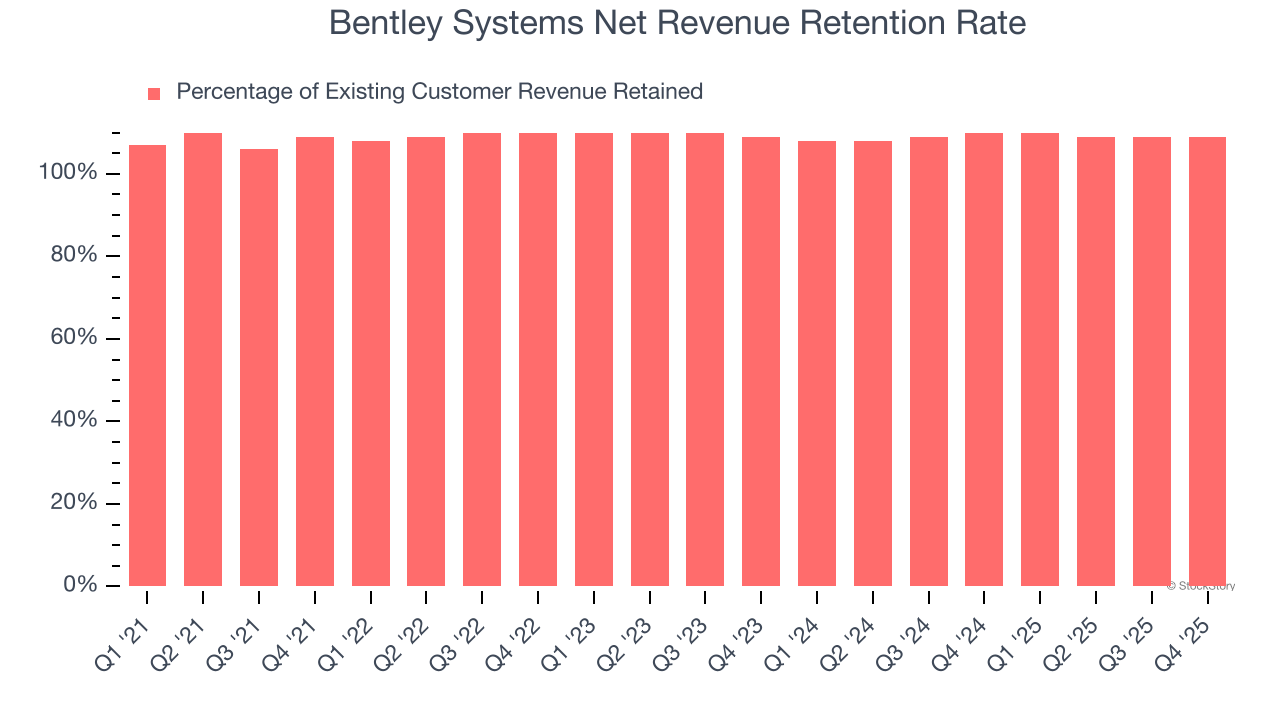

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Bentley Systems’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 109% in Q4. This means Bentley Systems would’ve grown its revenue by 9.3% even if it didn’t win any new customers over the last 12 months.

Bentley Systems has a decent net retention rate, showing us that its customers not only tend to stick around but also get increasing value from its software over time.

We were impressed by how significantly Bentley Systems blew past analysts’ billings expectations this quarter. We were also glad next year’s revenue guidance was robust. On the other hand, its adjusted operating income missed. Overall, we think this was still a decent quarter with some key metrics above expectations. The stock traded up 5.7% to $34.34 immediately following the results.

Bentley Systems may have had a good quarter, but does that mean you should invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-24 | |

| Jul-23 | |

| Jul-16 | |

| Jul-08 | |

| May-26 | |

| May-22 | |

| May-07 | |

| May-07 | |

| Apr-29 | |

| Apr-01 | |

| Mar-09 | |

| Mar-05 | |

| Mar-04 | |

| Mar-02 | |

| Mar-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite