|

|

|

|

|||||

|

|

|

Semiconductor companies are at the core of the AI revolution, as they offer solutions that enable improved processing power and efficiency to execute cloud and AI workloads.

Both Credo Technology Group Holding Ltd CRDO and Texas Instruments TXN operate in the semiconductor industry, but in different areas. They vary widely in terms of scale and maturity.

Texas Instruments is a manufacturer of analog and embedded processing chips, while Credo specializes in high-speed connectivity solutions, which are essential for cloud computing, hyperscale networks and AI.

Both companies bring unique strengths to the table, which makes this an intriguing comparison for investors.

So, the question now arises: Which stock is a better investment pick at present? Let us dive into the fundamentals, valuations, growth outlook and risks for each company.

CRDO’s focus on high-performance, energy-efficient connectivity solutions gives it strategic relevance as hyperscalers and cloud service providers overhaul their network architectures amid AI-driven data center expansion. As AI clusters scale into the hundreds of thousands of GPUs and push toward million-GPU configurations, reliability, signal integrity, latency and power efficiency, total cost of ownership has become “mission-critical”. Credo’s architecture (purpose-built SerDes technology, sound IC design and a system-level development approach) is tailored to meet these demands.

CRDO recently reported preliminary results for the third quarter of fiscal 2026. The company now expects to report revenues between $404 million and $408 million, far exceeding its previously issued guidance of $335 million to $345 million. CRDO expects sequential revenue growth in the mid-single digits heading into fiscal 2027. Credo now anticipates more than 200% year-over-year revenue growth for fiscal 2026 (up from prior 170% view). The company will report fiscal third-quarter results on March 2, 2026.

CRDO’s Active Electrical Cables (AECs) business sits at the core of its growth narrative, playing an increasingly critical role in AI-driven networking deployments. It is now focusing on the IC portfolio, which includes retimers and optical DSPs, and has continued to show a healthy performance. On the last earnings call, management noted that the PCIe retimer program remains on track for design wins in fiscal 2026 and revenue contributions in the next fiscal year.

Credo Technology Group Holding Ltd. price-consensus-eps-surprise-chart | Credo Technology Group Holding Ltd. Quote

The introduction of three additional pillars, each representing a multi-billion-dollar opportunity, bodes well. These include Zero-Flap optics, active LED cables and OmniConnect gearboxes (Weaver). These three, along with AECs and IC solutions (retimers and optical DSPs), collectively present a market opportunity likely to surpass $10 billion, more than tripling Credo’s market reach just 18 months ago, as management highlighted on the fiscal second quarter earnings call.

CRDO remains “well capitalized” to continue to fuel the next leg of growth, while maintaining a considerable cash buffer. At the end of the last reported quarter, it had a fortified balance sheet, boasting a cash position of $813.6 million. The company generated cash flow from operating activities of $61.7 million, up $7.5 million sequentially, while free cash flow totaled $38.5 million.

This cash strength is strategically valuable as Credo deepens its role in the hyperscale ecosystem. Increasing funds offer Credo meaningful internal funding capacity to invest in system-level platform expansion and new product initiatives. The cash balance also boosts CRDO’s M&A efforts. Last year, CRDO acquired Hyperlume, which is a developer of miniature light-emitting diode (microLED) technology-based optical interconnects for chip-to-chip communication.

Texas Instruments is one of the leading names in the semiconductor domain. It reported sales of 17.7 billion in 2025, up 13%, driven by increasing demand, especially in the Analog segment. Texas Instruments operates under three business divisions: Analog, Embedded Processing and Other.

Strength in the Analog segment is one of the key catalysts for TXN, with revenues from the segment surging 15% to $14 billion in 2025. Analog chips are required in almost any electronic device. As analog devices are used in a wide range of industries like industrial, automotive, data center, personal electronics and communications equipment, this diversification insulates TXN from overreliance on any single end market.

Explosive growth in the newly classified data center end market has emerged as a compelling development. In the fourth quarter of 2025, revenues from this end market surged 70% year over year. Data center contributed 9% to total revenues in 2025, or $1.5 billion, up 64% year over year. The company started to report data center as a separate market starting in the fourth quarter. By breaking out data center as a separate market, including compute, networking, rack power and thermal management, the company underscores the solid business opportunities tied to AI.

Texas Instruments Incorporated price-consensus-eps-surprise-chart | Texas Instruments Incorporated Quote

Texas Instruments continues to strengthen its dominance in the industrial and automotive sectors. Industrial and automotive each contributed $5.8 billion in 2025 revenues, both representing 33% of total revenues. Management highlighted “secular content growth,” meaning more analog and embedded chips per application over time, to drive growth in these end markets. Combined with the data center market, these three markets now account for 75% of total revenues in 2025, up dramatically from 43% in 2013.

Investors would find strong capital allocation plans also appealing. In 2025, the company generated approximately $7.15 billion of operating cash flow and distributed approximately $6.48 billion through dividend payments and share buybacks.

Although TXN is nearing the end of its six-year elevated capex cycle, 2025 capital expenditures surged to $4.6 billion. Texas Instruments invested heavily in 300-millimeter wafer fabrication facilities to expand cost-efficient manufacturing capacity at scale in the past six years. Massive debt load limits flexibility. Total debt stands at $14 billion compared with $4.9 billion in cash and short-term investments. Weaknesses in end markets like Personal Electronics and Communications Equipment remain concerning. Moreover, the semiconductor landscape remains fraught with intense competition.

In the past month, CRDO has lost 3.2%, while TXN has gained 8.6%.

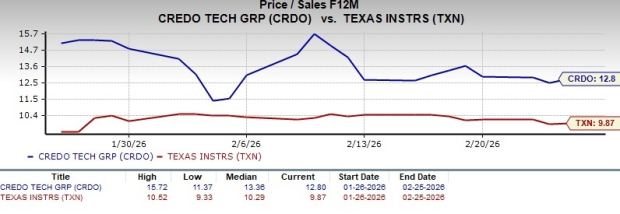

In terms of the forward 12-month price/sales ratio, Credo is trading at 12.8X, higher than TXN’s 9.87X.

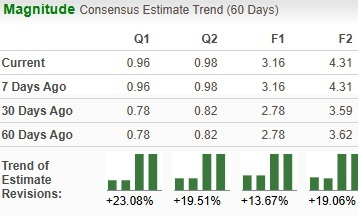

Analysts have revised earnings estimates upwards by 13.7% for CRDO for the current fiscal year in the past 60 days.

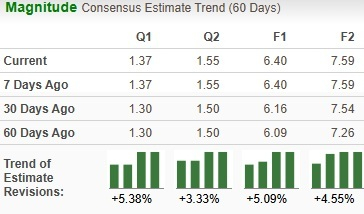

Estimates have been revised 5.1% upwards for TXN’s bottom line.

CRDO currently flaunts a Zacks Rank #1 (Strong Buy) and TXN carries a Zacks Rank #3 (Hold).

In terms of the Zacks Rank, CRDO appears to be a better pick at the moment.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 50 min | |

| 2 hours | |

| Jul-19 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-14 | |

| Jul-14 | |

| Jul-13 | |

| Jul-10 | |

| Jul-10 | |

| Jul-09 | |

| Jul-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite