|

|

|

|

|||||

|

|

|

Coeur Mining, Inc. CDE and Ero Copper Corp. ERO) are operating in a supportive macro environment marked by elevated gold prices, driven by safe-haven demand, central bank buying and resilient investment inflows, which strengthen pricing and cash flow visibility.

Coeur Mining remains more directly leveraged to gold price movements and operational execution across its precious metals portfolio. Ero Copper, primarily exposed to structurally strong copper demand from electrification and infrastructure trends, benefits from gold by-product credits that provide additional upside amid firm precious metals demand.

Let’s dive deep and closely compare the fundamentals of these two miners to determine which one is a better investment now.

Coeur produced approximately 112,429 ounces of gold and 4.7 million ounces of silver in the fourth quarter of 2025, up from about 87,149 ounces and 3.2 million ounces, respectively, in the year-ago quarter, reflecting stronger execution and portfolio contributions.

Las Chispas in Mexico delivered about 14,719 ounces of gold and 1.4 million ounces of silver on steady high-grade throughput, while Palmarejo produced roughly 25,662 ounces of gold and 1.6 million ounces of silver on higher milling volumes.

Rochester in Nevada contributed nearly 17,000 ounces of gold and 1.7 million ounces of silver, driven by expanded crushing capacity and stronger ore placement. Kensington in Alaska added close to 30,000 ounces of gold on improved grades, and Wharf in South Dakota produced around 25,000 ounces of gold despite minor operational disruptions.

Rochester’s three-stage crushing circuit raised capacity to about 88,000 tons per day, enhancing its silver and gold production outlook. Las Chispas is maintaining a high-grade throughput of more than 400 g/t silver equivalent, with continued drilling supporting resource growth. Palmarejo has strengthened its reserve base through ongoing near-mine exploration, while Kensington’s underground advancements have improved access to higher-grade areas, sustaining quarterly production of around 30,000 ounces of gold. At Wharf, recent reserve additions have extended the mine’s life to roughly 12 years.

At the end of December 2025, CDE’s cash and cash equivalents were $554 million, a significant increase of $55 million from a year ago. Total debt was reduced to roughly $341 million from about $590 million a year earlier. Free cash flow in the fourth quarter was about $313 million. The higher output amid favorable metal prices is expected to enhance revenue visibility, support margin expansion and boost cash flows.

Ero Copper delivered record consolidated copper production of 19,706 tons, up significantly from 12,883 tons in the fourth quarter of 2024, reflecting a strong year-over-year increase driven by improved mill throughput and operational stability at Caraíba, along with the continued ramp-up of the Tucuma operation.

Gold production totaled 28,836 ounces, also rising meaningfully from the year-ago quarter on stronger by-product output and processing performance. The higher volumes enhanced revenue leverage amid firm copper and gold prices, positioning ERO for sustained growth as its newer assets continue to optimize performance.

It recently strengthened its growth trajectory through record operating performance and the advancement of key expansion projects in Brazil. In 2025, the company produced a record 64,307 tons of copper and 52,290 ounces of gold, as Tucumã ramps up and optimization efforts continue at Caraíba.

A major growth catalyst is the inaugural PEA for the Furnas copper-gold project in the Carajás Mineral Province, outlining a 24-year initial mine life, average annual production of roughly 108,000 tons of copper equivalent over the first 15 years. ERO is advancing the new shaft at the Pilar Mine, undertaking plant debottlenecking initiatives, and executing extensive exploration programs to expand resources and support long-term production growth toward a targeted 80,000–90,000 tons of copper annually.

At the end of September 2025, ERO’s cash and cash equivalents were $66 million. Long-term debt was $571 million. Free cash flow in the third quarter was about $34 million.

Heading into the fourth quarter with solid free cash flow generation gave Ero Copper a stronger liquidity cushion to manage working capital requirements, fund the Tucumã ramp-up and cover sustaining capital at Caraíba. Stronger fourth-quarter production and sales will likely support a sequential build in cash and a gradual improvement in net debt levels, enhancing overall financial flexibility. While continued capital expenditures may limit the speed of deleveraging, solid operating results should continue to sustain liquidity and reinforce the company’s balance sheet position.

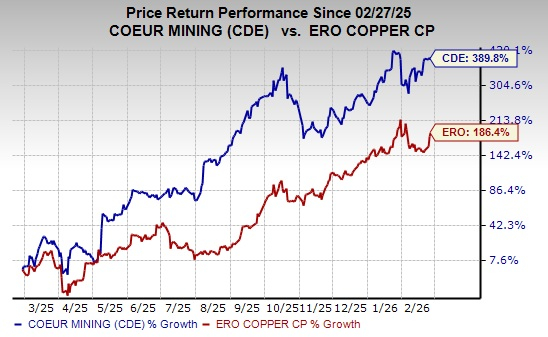

CDE stock has surged 389.8% in the past year, and ERO is up 186.4%.

CDE is currently trading at a forward 12-month earnings multiple of 12.17X, while ERO is currently trading at a forward 12-month earnings multiple of 7.92X.

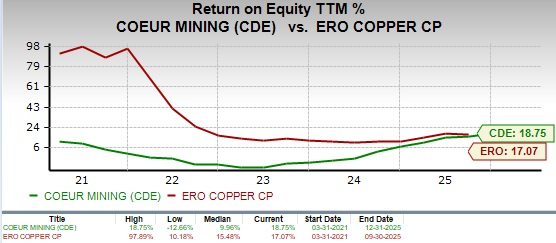

CDE is currently trading at a trailing 12-month Return on Equity of 18.75% and ERO is trading at a 17.07%

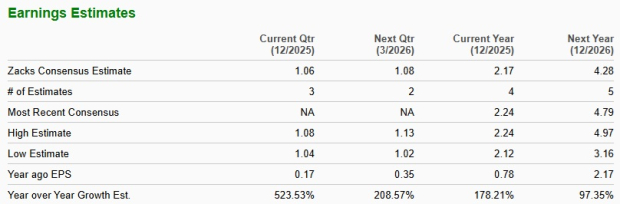

The Zacks Consensus Estimate for CDE’s 2026 sales implies year-over-year growth of 120%. The same for EPS suggests a 144% year-over-year rise.

EPS estimates for CDE for fiscal 2026 have been trending higher over the past 60 days.

The consensus estimate for ERO’s 2026 sales and EPS implies a year-over-year rise of 46% and 98%, respectively.

EPS estimates for 2026 have been trending northward over the past 60 days.

Coeur Mining and Ero Copper both present compelling cases to hold in a portfolio. CDE offers stable, cash-generative growth with a strong balance sheet, low debt and diversified exposure to gold and silver, supported by operational improvements across multiple mines and extended mine life at key assets. In contrast, ERO delivers higher growth potential, driven by record copper and gold production, the ramp-up of Tucumã and long-term projects like the Furnas copper-gold development, though it carries higher leverage and smaller cash reserves.

ERO has a slight edge on the valuation basis because of its low multiple compared to CDE. Holding both allows investors to balance stability and predictable cash flow from CDE with the upside and copper exposure offered by ERO, providing a diversified approach to precious and base metals investments.

Both CDE and ERO carry a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 (Strong Buy) Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-21 | |

| Jul-16 | |

| Jul-09 | |

| Jul-08 | |

| Jul-02 | |

| Jun-29 | |

| Jun-25 | |

| Jun-18 | |

| Jun-10 | |

| Jun-10 | |

| Jun-08 | |

| Jun-08 | |

| Jun-05 | |

| Jun-04 | |

| May-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite