|

|

|

|

|||||

|

|

|

Bank of America BAC and Wells Fargo WFC are two of the four largest U.S. banks and are classified as systemically important financial institutions. Both institutions derive significant net interest income (NII) and maintain substantial exposure to consumer banking, leaving them highly responsive to shifts in interest rates and overall economic conditions.

Although they operate under similar macroeconomic influences, their strategic positioning differs. Wells Fargo has regained greater operational flexibility following the removal of its asset cap, while Bank of America continues to benefit from solid momentum in its investment banking division.

With these factors in mind, a closer examination of their long-term growth outlooks can help determine which bank currently offers the more compelling investment opportunity.

Bank of America, one of the most rate-sensitive banks in the country, is prioritizing organic, domestic growth through the expansion of its physical and digital presence. This is part of a broader strategy to solidify customer relationships and tap into new markets, driving NII growth over time. By 2027, the company plans to expand its financial center network and open more than 150 centers.

Despite the Federal Reserve’s three interest rate cuts in 2025, Bank of America is expected to witness continued improvement in NII and net interest yield in the near term, supported by loan growth and stabilizing funding costs. Management expects NII (FTE) to grow 5-7% year over year in 2026.

Coupled with the growing adoption of digital tools, such as the Zelle money transfer system and the AI-powered assistant Erica, these initiatives support BAC's ability to enhance digital engagement and cross-sell a range of products, including mortgages, auto loans and credit cards.

BAC’s investment banking (IB) business is well-positioned to expand as deal-making activities have regained momentum. As the market for global mergers and acquisitions has been improving, the company will continue to witness solid growth in IB fees, driven by a healthy IB pipeline. In 2025, IB fees increased 8.4% on a year-over-year basis.

Over the next three to five years, BAC aims to deliver 12% of earnings growth and a return on tangible common equity (ROTCE) between 16% and 18%.

Wells Fargo is moving to expand across multiple business lines now that the Fed has lifted the asset cap that limited its growth since 2018. With this, the company can now boost deposits, grow its loan portfolio and broaden its securities holdings. This will lead to an increase in NII, going forward. WFC intends to expand fee-generating businesses like payment services, asset management and mortgage origination. These fee income-generating opportunities will bolster its top-line mix.

Wells Fargo is adopting a more balanced approach to its operations. While the bank is reducing headcount and streamlining processes, it is investing in its branch network and digital upgrades. This allows the bank to maintain a focus on cost management.

Wells Fargo is taking a strategic approach to its branch network, reducing its total branches by 2.1% year over year to 4,090 in 2025. At the same time, it continues to invest and optimize its branch network to reduce costs. In 2025, the company refurbished approximately 700 branches, with more than half of its branch network now upgraded and the remaining branches expected to be completed over the next few years.

Wells Fargo has signaled that interest rate cuts will help stabilize funding costs, making deposit growth a central pillar of its balance sheet strategy. With lower rates and asset cap removal, the bank aims to aggressively grow consumer and corporate loan assets. Average loans are expected to increase in the mid-single-digit rate in 2026. WFC expects NII to be $50 billion in 2026, supported by balance-sheet growth, a favorable loan and deposit mix, and continued fixed-asset repricing.

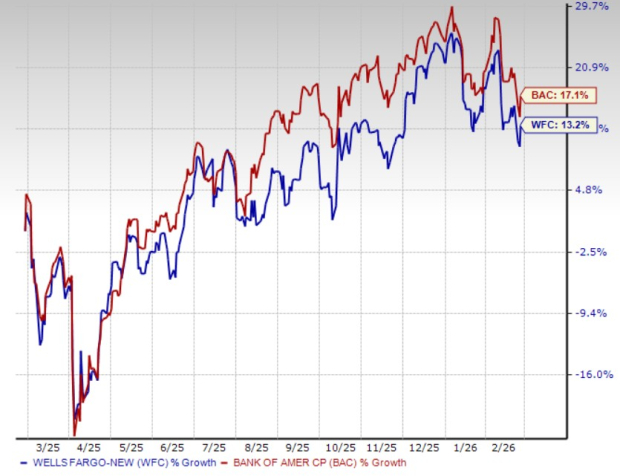

In the past year, shares of Bank of America and Wells Fargo have gained 17.1% and 13.2%, respectively.

Price Performance

In terms of investor sentiments, BAC clearly has the edge.

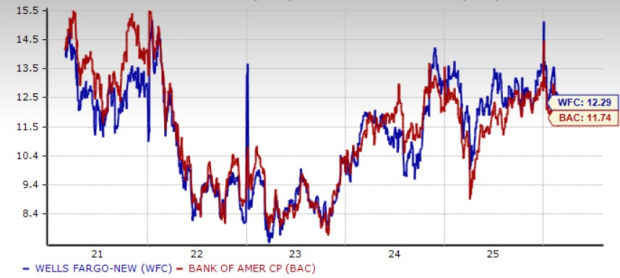

In terms of valuation, BAC is currently trading at a 12-month forward price-to-earnings (P/E) of 11.74 X, while the WFC stock is trading at a 12-month forward P/E of 12.29X.

Price-to-Earnings F12M

Both are trading at a discount compared with the industry average of 13.60X. So, Bank of America is inexpensive compared with WFC.

BAC’s dividend yield of 2.17% is more than Wells Fargo’s dividend yield of 2.08%. Nonetheless, both are higher than the S&P 500 average dividend yield of 1.08%.

Dividend Yield

The Zacks Consensus Estimate for BAC’s 2026 and 2027 revenues implies year-over-year growth of 7.1% and 4.8%, respectively. The consensus estimate for earnings indicates 12.9% and 14.6% rallies for 2026 and 2027, respectively.

Earnings Estimate

On the contrary, the Zacks Consensus Estimate for WFC’s 2026 and 2027 revenues implies year-over-year growth of 5.4% and 4.9%, respectively. The consensus estimate for earnings indicates 10.2% and 12.9% rallies for 2026 and 2027, respectively.

Earnings Estimate

While both Bank of America and Wells Fargo are well-positioned to benefit from loan growth, stabilizing funding costs, and improving economic conditions, Bank of America currently offers the more compelling long-term upside.

BAC combines solid NII growth with a powerful and expanding investment banking franchise, giving it a diversified earnings engine. Its continued investment in digital capabilities, branch expansion and cross-selling initiatives further strengthens its competitive positioning. Importantly, consensus estimates point to stronger revenue and earnings growth for BAC, yet the stock trades at a slightly lower forward valuation multiple than WFC.

While Wells Fargo’s asset cap removal provides meaningful flexibility and growth opportunities, its projected growth rates remain modestly below BAC’s, and its transformation efforts are still ongoing.

Considering superior projected earnings growth, diversified revenue streams, attractive valuation and strong operational momentum, Bank of America offers a stronger blend of stability and growth.

Currently, BAC and WFC carry a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 47 min | |

| 1 hour | |

| 2 hours | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-19 | |

| Jul-19 | |

| Jul-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite