|

|

|

|

|||||

|

|

|

Oddity Tech Ltd. ODD delivered fourth-quarter 2025 results, with both the top and bottom lines surpassing the Zacks Consensus Estimate. Revenues saw year-over-year growth, while the earnings remained flat compared to the previous-year period.

Management disclosed a severe spike in customer acquisition costs driven by algorithm changes at its largest advertising partner, which pushed CPAs to more than double normal levels and made first-time orders unprofitable. The company warned of a meaningful revenue decline in the first half of 2026 and withdrew full-year guidance due to limited visibility on when advertising efficiency will normalize.

Given ODD’s heavy reliance on paid digital acquisition to fuel growth, the disruption raised concerns about margin pressure, earnings uncertainty and platform dependency risk. As a result of these forward-looking headwinds, the stock plunged 49.2% yesterday.

ODD reported quarterly earnings of 20 cents per share, beating the Zacks Consensus Estimate of 14 cents per share. The reported figure was higher than the guided range of 11 to 13 cents.

ODDITY Tech Ltd. price-consensus-eps-surprise-chart | ODDITY Tech Ltd. Quote

Net revenues of the company were $152.7 million, rising 23.5% year over year from $123.6 million and beat the Zacks Consensus Estimate of $151 million. The reported figure came higher than the expected range of $149 million to $152 million. The revenue growth was mainly driven by the rise in the number of orders.

Gross profit increased 20% year over year to $108 million from $90 million in the previous-year period, while the gross margin reached to 70.5%, declining by 220 basis points year over year from 72.7%. Despite this margin contraction, it came higher than the expected adjusted gross margin of 69%. This outperformance was partly driven by the product mix.

Selling, general and administrative expenses totaled $106 million in the fourth quarter, representing a 23.4% increase year over year compared with $85.8 million in the prior-year period.

Adjusted EBITDA declined 17.4% year over year to $12.5 million. Despite this decline, the adjusted EBITDA came higher than the expected range of $10 million to $12 million.

The adjusted EBITDA margin was 8.2% compared with 12.3%, declining significantly by 410 basis points year over year. Contraction was primarily due to planned investments to support future growth. These investments include the launch of the METHODIQ brand, the development of ODDITY LABS and Brand 4, as well as increased media spending to drive brand awareness and expansion initiatives.

The company exited 2025 in a strong liquidity position, with $776 million in cash, cash equivalents and investments on the balance sheet. The increase in reserves during 2025 was driven by a successful exchangeable note offering and free cash generation of $84 million for the year. Fourth-quarter free cash flow was negatively impacted by approximately $19 million in higher inventory levels, reflecting new inventory investments in METHODIQ in addition to the seasonal build ahead of the first-quarter selling period.

In January 2026, the company amended its credit facilities to expand borrowing capacity to $350 million. These facilities remain undrawn.

Oddity believes repurchasing its stock is attractive at recent share prices and intends to opportunistically return cash to shareholders through share buybacks. A total of $103 million remains under its previously announced $150 million repurchase authorization, which expires on June 30, 2027.

For the first quarter of 2026, the company expects sales to decline approximately 30% year over year due to reduced new user acquisition caused by abnormally high customer acquisition costs. The company stated that acquisition costs in some cases are running at more than two times normal levels, and at current CPAs, the company is not profitable on first orders, which will materially pressure near-term EBITDA.

For the second quarter of 2026, the company indicated that sales are also likely to decline, although the company is not yet able to quantify the magnitude. The uncertainty relates to the timing of normalization in customer acquisition costs. The company emphasized that the first and second quarters are historically the largest user acquisition periods, and weaker acquisition in those quarters will reduce repeat revenue later in the year, even if acquisition costs normalize in the second half.

The company is not issuing full-year 2026 guidance at this time due to limited visibility on when acquisition costs will return to normalized levels. The company expects the most significant financial impact to occur in the first half of 2026 and expressed hope for meaningful progress in the second quarter and normalization in the third or fourth quarters.

On margins, the company stated that costs are being actively managed to offset EBITDA pressure, while continuing to invest in growth initiatives, including ODDITY LABS, new product development, METHODIQ, Brand 4, and technology infrastructure. The company also reiterated long-term financial algorithm targets of 20% sustained top-line growth and approximately 20% adjusted EBITDA margins once conditions normalize.

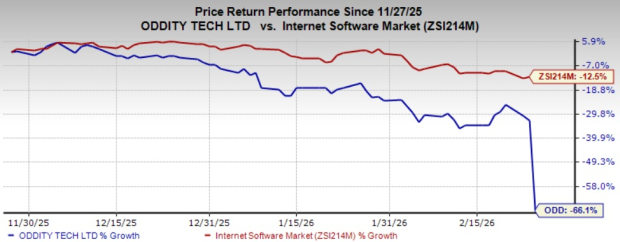

ODD currently carries a Zacks Rank #3 (Hold). Its shares have plummeted 66.1% in the past three months compared with the industry’s 12.5% decline.

Some better-ranked stocks have been discussed below:

Hubspot, Inc. HUBS provides inbound marketing and sales applications over the cloud. HUBS currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for HUBS' current fiscal-year sales and earnings implies growth of 17.9% and 26.7% from the year-ago actuals. HUBS delivered a trailing four-quarter negative earnings surprise of 3%, on average.

Getty Images Holdings, Inc. GETY is a preeminent global visual content creator and marketplace which offers a full range of content solutions. GETY currently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for GETY’s current fiscal-year sales indicates growth of 0.8%, and the same for earnings indicates a decline of 412.5% from the year-ago reported figures. GETY delivered a trailing four-quarter earnings surprise of 258.3%, on average.

A10 Networks, Inc. ATEN provides software based application networking solutions. ATEN currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for ATEN’s current fiscal-year sales and earnings indicates growth of 10.7% and 13.3%, respectively, from the year-ago reported figures. ATEN delivered a trailing four-quarter earnings surprise of 4.9%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 7 hours | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-18 | |

| Jul-17 | |

| Jul-16 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 | |

| Jul-10 | |

| Jul-09 | |

| Jul-08 | |

| Jul-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite