|

|

|

|

|||||

|

|

|

PayPal Holdings PYPL released fourth-quarter 2025 results on Feb. 3, with earnings per share (EPS) and revenues missing the Zacks Consensus Estimates. The company issued weaker-than-expected 2026 guidance, and with this, shares slipped 9.6% since the earnings announcement through yesterday’s closing session.

Given the estimate miss and weaker guidance, we intentionally waited before publishing our review to gauge whether price movements may reveal deeper sentiment trends. Let’s delve deeper and find out.

On paper, PayPal reported moderate growth in the fourth quarter of 2025. The company’s net revenues came in at $8.68 billion, rising 3.7% year over year. Adjusted EPS stood at $1.23, reflecting a 3.4% increase year over year. Non-GAAP operating income rose 3%. Total Payment Volume (“TPV”) climbed 8.8% to $475.14 billion. Transaction margin dollars (“TM$”) increased 2.5% to $4.03 billion from the year-ago quarter. Total active accounts increased 1.2% year over year to 439 million.

However, the company issued full-year 2026 guidance, where TM$ is expected to decline slightly alongside an adjusted EPS range of a low single-digit decline to a slightly positive gain, signaling caution about its strategic path ahead. Management expects to generate more than $6 billion of adjusted free cash flow, and projects share repurchases to be $6 billion in 2026. With lower 2026 guidance, the sustainability of the drivers was questioned.

PayPal’s online branded checkout TPV grew only 1% on a currency-neutral basis, down from 5% in the previous quarter. The company highlighted U.S. retail weakness (K-shaped economy impact on middle-income consumers), international headwinds (e.g., Germany macro softness and competition) and slowdown in high-growth verticals like travel, ticketing, crypto and gaming as factors leading to this de-growth. In the fourth quarter of 2025, engagement per user slipped, with payment transactions per active account on a trailing 12-month basis declining 4.8% year over year.

Management admitted its execution in the quarter has not met expectations, with slow speed and insufficient focus. This prompted a CEO change and appointment of Enrique Lores to bring greater discipline and accelerate execution. Moreover, PayPal operates in a highly competitive global payments industry, and its nature of business makes it vulnerable to foreign exchange fluctuations.

Venmo is positioned as the preferred money movement platform for the young, affluent, digitally native consumers. Venmo’s user base is large and growing, with more than 100 million total active accounts. In the fourth quarter of 2025, Venmo’s TPV rose 13%, marking its fifth consecutive quarter of double-digit growth.

More importantly, revenue composition has shifted as more consumers are using Venmo for everyday commerce. In 2025, Venmo revenue grew approximately 20% to $1.7 billion, excluding interest income. Over the past two years, Pay with Venmo and Venmo debit card revenue have doubled. This mix shift is important to its overall transformation and positions Venmo for stronger profitability as it continues to grow.

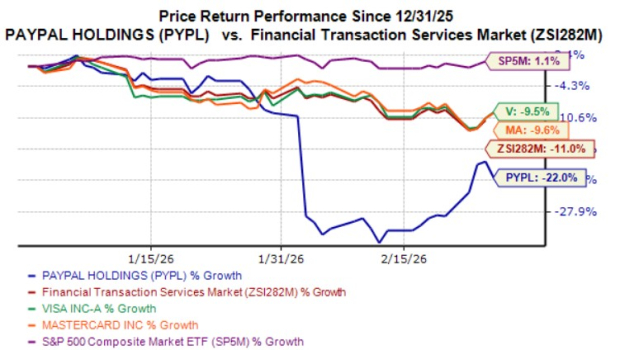

PYPL shares have dropped 22% year to date, largely due to intensifying competition in the fintech sector. Rivals like Visa Inc. V and Mastercard Incorporated MA continue to expand their offerings, challenging PayPal’s dominance in digital payments. Broader macroeconomic pressures and uncertainty surrounding the tariff policy have also dampened investor sentiment. While PYPL has struggled more, Visa and Mastercard shares have declined 9.5% and 9.6%, respectively, over the same timeframe.

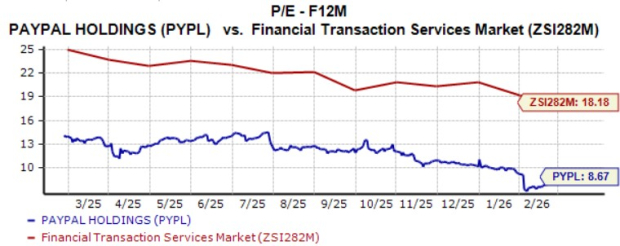

However, with the decline, PayPal shares are trading cheap, as suggested by the Value Score of A. In terms of forward 12-month P/E, PYPL stock is trading at 8.67X compared with the Zacks Financial Transaction Services industry’s 18.18X.

The stock is also cheaper than competitors, including Visa and Mastercard. Shares of Visa and Mastercard are currently trading at P/E of 23.12X and 25.66X, respectively.

PayPal’s estimate revisions reflect a negative trend for full-year 2026. The Zacks Consensus Estimate for 2026 earnings of $5.38 per share has been revised downward over the past week.

Although PayPal reported moderate growth in net revenues, adjusted EPS, TPV and TM$, its lower growth in online branded checkout TPV and weaker 2026 guidance made investors adopt a cautious stance post fourth-quarter earnings. Reflecting on this, the stock has underperformed the broader industry in the year-to-date period. Estimate revisions trends for 2026 earnings have also shifted downward. Intensifying competition, alongside macroeconomic pressures, adds further uncertainty. Amid this environment, it is better to focus on other stable opportunities.

PayPal currently has a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 32 min | |

| 6 hours | |

| 7 hours | |

| 8 hours | |

| 9 hours | |

| 13 hours | |

| 14 hours | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite